Under normal circumstances, a waterfall-like collapse in commodity prices would not be seen as “good news” for the economy’s near-term prospects. But these are not normal circumstances.

A few weeks back I called the top in wage-related inflation pressures. I still think I will be right as we get data reflecting hiring / firing into the summer months. There will be acute shortages of labor in various (important) pockets of the economy, like commercial airline pilots and truckers and even lifeguards(!) but overall things are easing.

I also called the top in housing-related inflation pressures. I might be early on that one – new and existing home sales are now dropping and prices are being cut at a fast clip, but rents are still too damn high.

I will add commodity price-related inflation to the list of things that are getting better. The price of everything is dropping precipitously. The Wall Street Journal cites a fall in some commodity markets that puts prices back to where they were in March…

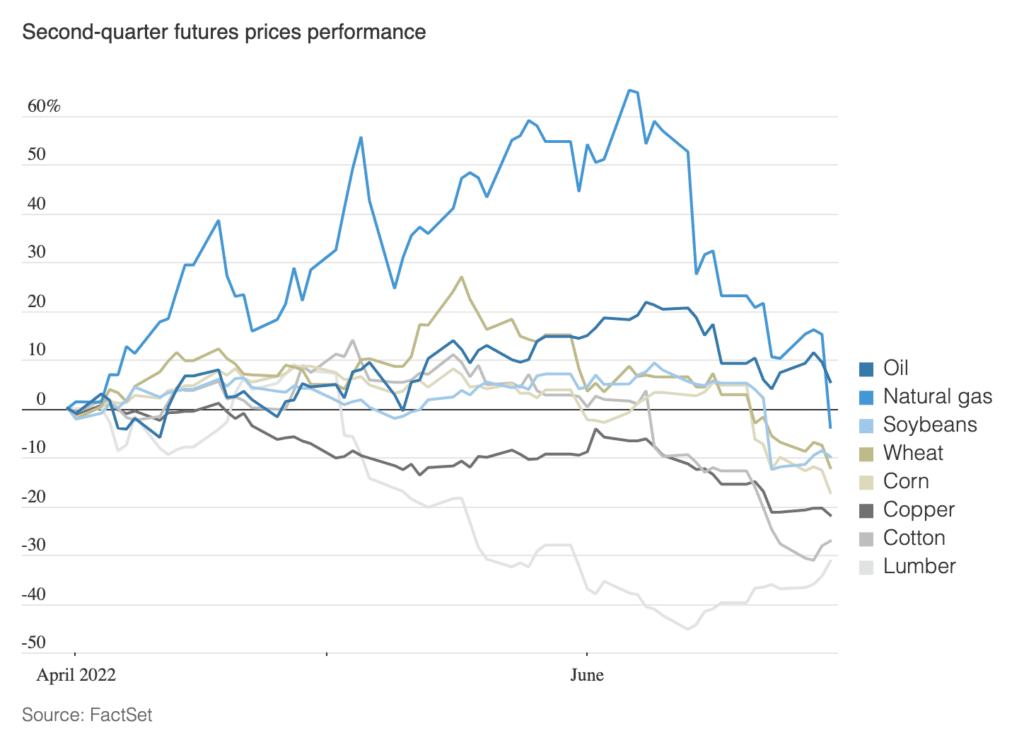

Natural-gas prices shot up more than 60% before falling back to close the quarter 3.9% lower. U.S. crude slipped from highs above $120 a barrel to end around $106. Wheat, corn and soybeans all wound up cheaper than they were at the end of March. Cotton unraveled, losing more than a third of its price since early May. Benchmark prices for building materials copper and lumber dropped 22% and 31%, respectively, while a basket of industrial metals that trade in London had its worst quarter since the 2008 financial crisis.

This is good news, I suppose. I’m not sure how much of this drop is coming from whatever the Fed is doing to destroy demand and how much is just the natural way of things running their course. As has been pointed out here and elsewhere, the best cure for high commodity prices is high commodity prices. Supply will always, eventually, arrive to meet a surfeit of demand. And supply will also always overshoot because producers want to sell things to consumers for money. That’s kind of the whole point.

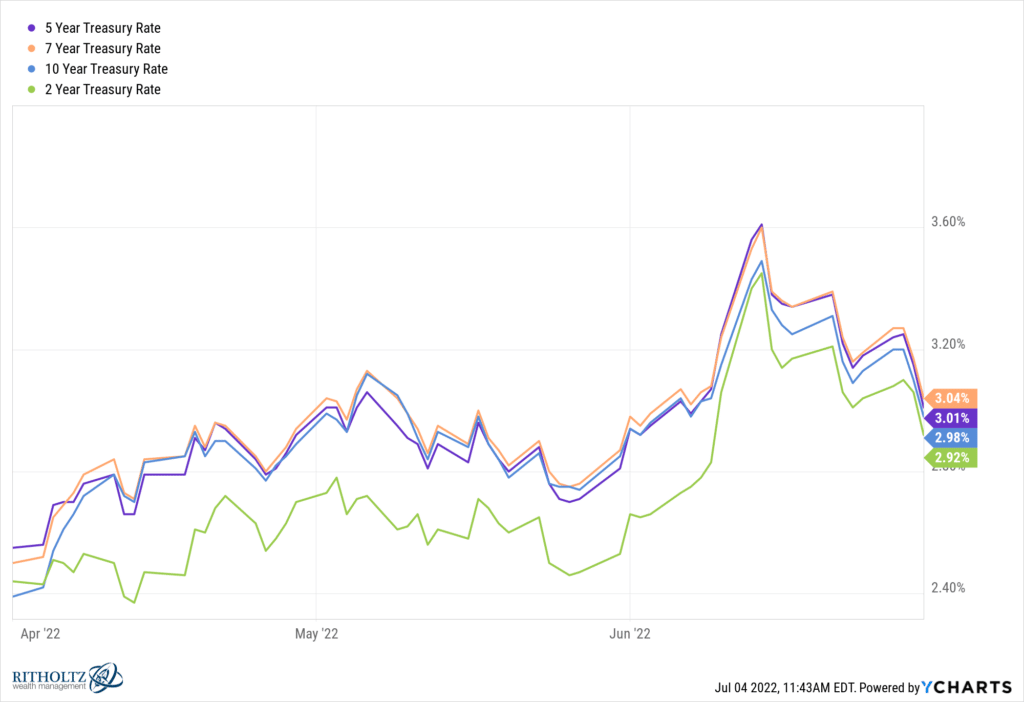

I don’t know how and when this all translates into CPI or PCE inflation stats in the coming months, I just know that it will. Which gives the Federal Reserve a little more breathing room, perhaps. More optionality, something it hasn’t had in six months. The bond market is not waiting for the Fed. It’s already been reacting. Here are the 2, 5, 7 and 10 year Treasury rates peaking out (at least in the short-term) as the economic data softens, recession talk fills the air and the market anticipates a drop in the inflation threat:

Now you might be asking “How does the Fed impact commodity prices? I thought that was solely the province of supply and demand in the real economy…?” Not quite. There are other factors at play. One of those factors is what tighter money can do to the demand side. We’re seeing that slowly play out. The other factor is the amount of money placing bullish bets and driving prices up in the financial markets – a factor that the Fed can influence a great deal by making money cost more and / or reducing the overall liquidity picture in general. After a huge rally in the futures market, the flows are now going the other way.

Back to WSJ:

Traders and analysts say that some of the decline in commodity prices can be traced to the retreat of investors who piled into markets for fuel, metals and crops to hedge against inflation. JPMorgan Chase & Co. commodity strategist Tracey Allen said about $15 billion moved out of commodity futures markets during the week ended June 24. It was the fourth straight week of outflows and brought to about $125 billion the total that has been pulled from commodities this year, a seasonal record that tops even the exodus in 2020 as economies closed.

It’s not magic. It’s monetary policy. Interest rates are to the financial markets as gravity is to the physical world, and nothing is immune to gravity.

None of this will save Biden’s party in the midterms. It’s going to be a slaughterhouse for the Dems, as the midterms often are for the incumbent party – especially when voters despise their current economic conditions as they do today. I don’t think the reaction to SCOTUS’s overturn of Roe v Wade is going to do enough for turnout to counter the negative economic sentiment out there right now. It’s bad and shows no sign of improvement. In 1982 there was talk within the GOP that maybe Reagan ought to stand down from reelection in ’84, just as there is talk today of whom the Democrats should run in Biden’s place in two years. High inflation and a persistently hawkish Fed are a nearly insurmountable challenge for whomever is “responsible” in the eyes of the public.

But a slowing economy accompanied by falling inflation is preferable to pretty much anything else we could hope for right now.

So, good news. For now.

Source:

Falling Commodity Prices Raise Hopes That Inflation Has Peaked (WSJ)

Read Also: