An analysis of book value captures things like plants and equipment and facilities and hard-money, real assets that corporations have managed to accumulate over their lifetimes.

And when the cost of money is higher, these things are more highly valued by investors because they are expensive to replicate and costly to replace.

An analysis of book value doesn’t capture things like intellectual property and brand, intangible assets that corporations have accumulated or are currently accumulating.

And when the cost of money is lower (or, effectively zero) as it is today, these things become more highly valued by investors than physical assets are because they are weapons that corporations can use to nullify the moats and assets of the incumbent corporations that they are competing with for customers, revenue and market share.

This is why a AirBnB is currently more highly valued than all of the publicly traded hotel chains on the NYSE.

This is why Uber is worth more than all of the auto makers and taxi companies that own their own fleets of cars.

It’s why WeWork, which leases floors from building owners, is worth more than those building owners’ corporations.

This is how it’s possible that Beyond Meat, with its sizzling hot brand, could be worth exponentially more than the other publicly-traded food processing companies, with their century-old supply chains and manufacturing operations and union relationships and supermarket shelf space privileges and trucking contracts.

This is why the CEO of Goldman Sachs laments the fact that if his company’s Marcus online bank was a standalone “social finance” company backed by venture capitalists, it would be worth significantly more.

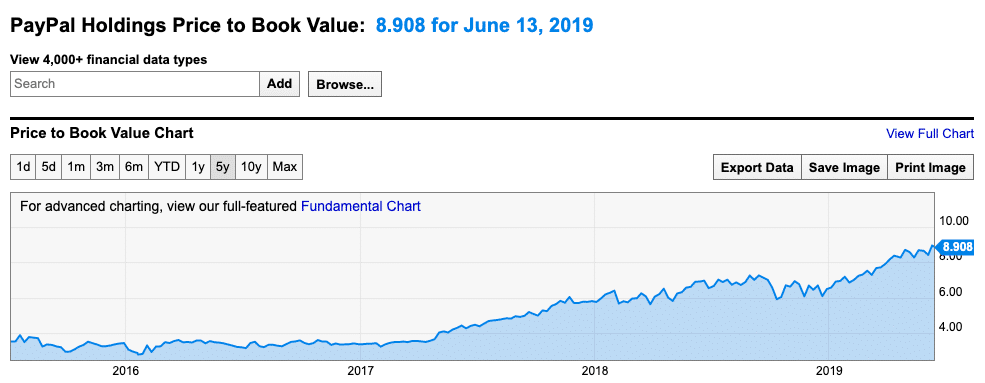

As he says this, note that the Goldman Sachs share price has just slipped below its tangible book value again. In the meantime, here’s PayPal’s price to book value – it has doubled over the last two years:

Nobody cares about PayPal’s book value because the truly valuable aspects of PayPal’s business – its brand, its ubiquity on the phones of millennials and its technological savvy – are not captured in the calculation of this metric. They lease office space, and they take market share. They don’t build factories or erect smokestacks off the side of the interstate highway.

And as a result of this popular preference for asset-light, recurring revenue model companies, factor (or smart beta) strategies that weight portfolios by the stocks’ price-to-book value have badly trailed the market.

Capital is Now Free, Have Fun

I had dinner with one of the foremost authors and thinkers in the history of the investment markets, William Bernstein, earlier this year. At the end of the dinner, Jason Zweig asked Bernstein “What’s the one thing that’s on your mind that no one else at this table is talking or thinking about right now?”

Bernstein said he’d been thinking about the question “What if the cost of capital never rises again?” The implications of a world in which equity capital is flowing while interest rates on credit never rise to the level of being a serious roadblock for innovation are fascinating to consider. What if every new idea that comes along, no matter how world-altering and disruptive, no matter how unproven or risky, can get overnight funding without much of a problem? Masayoshi Son’s Vision Fund has been investing based on this premise. Massive pools of capital from sovereign nations and university endowments and gigantic corporations like Google’s moonshot division are investing this way as well.

This question is being answered on Wall Street every day, even if the participants are not aware of it. Their actions and allocations have already decided what we think this world would look like. Value stocks have appreciated significantly less than growth stocks in the post-crisis period that’s been marked by a cost of capital that has approached zero. Value stocks have underperformed the overall stock market and their size within the indices has declined as a percentage of the weighting of these indices accordingly.

Lines

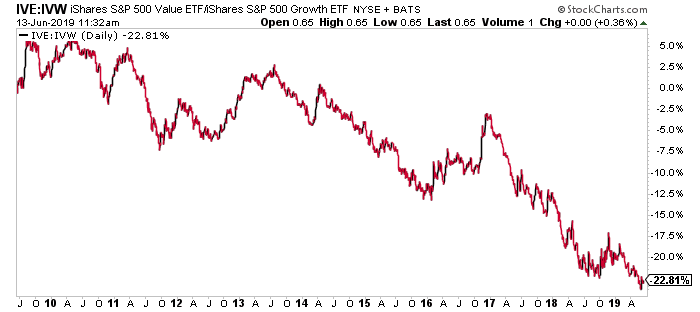

Below, a ratio chart of the incredible underperformance of value vs growth – the IVE is made up of US large value stocks. Here, it’s divided by the IVW ETF, which holds large cap growth stocks:

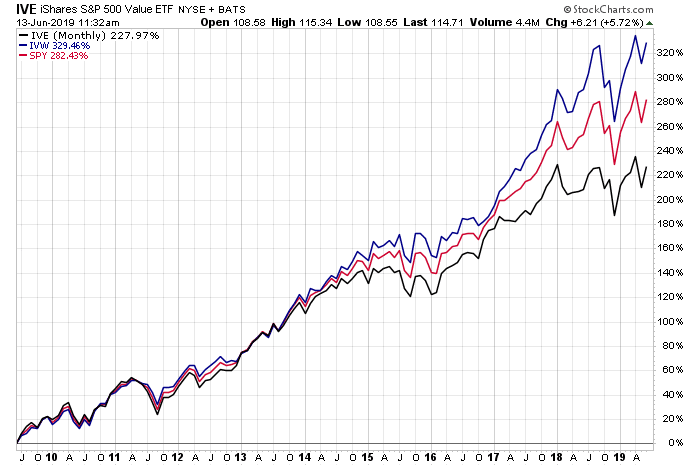

Seen another way, here’s the IVW (growth) in blue leading the S&P 500 in red, with the IVE (value) in black trailing substantially.

These are not just lines on a chart.

They are responsible for the shifting of trillions of dollars in market cap from one group of companies to another.

They are responsible for the collapse of some of the greatest reputations in the investing business, and for the numerous closings of their funds.

These lines have caused divorces and broken marriages among the hedge fund elite, as aging 90’s superstars, who could once reliably bet against highfliers while overweighting cheaper stocks, found they no longer had a viable investment strategy after a decade of free money funding moat-busting disruption and heretofore unfathomable business models. You don’t go home to Greenwich from your Park Avenue office in a good mood when the market makes it a point to remind you of how vestigial your skills have become, day after day after day.

Lines on charts become lines on people’s faces in this game. They become dividing lines separating things that used to work from things that may work in the future. While these lines are merely made of keystrokes and digital ink, the trends they are emblematic of in the real world cause layoffs and pivots and fire sales and bankruptcies on Wall Street.

Everyone Likes a Bargain (in theory)

There are no asset managers who represent their strategy to clients as “We buy the most expensive assets, and add to them as they rise in price and valuation.” That’s unfortunate, because this is the only strategy that could have possibly enabled an asset manager to outperform in the modern era. It’s one of those things you could never advertise, but had you done it, you’d have beaten everyone over the ten-year period since the market’s generational low.

But almost every investment professional says that they do the opposite of this. Even the explicitly growth-oriented managers use terms like “at a reasonable price,” to communicate their place on the spectrum of speculative chastity. There are no textbooks lauding an investment approach where it makes more sense to buy PayPal at 4 times book on its way to 9 times book while forsaking Goldman Sachs at less than 1 times book.

New initial public offerings for companies worth billions of dollars with little or no history of profit-making or tangible book value growth are arriving every month now. Public companies with long histories of profitability and substantial tangible assets are being routinely met with investor apathy, unless and until they make their digital transformations the paramount part of their story (a la Walmart and Disney and McDonalds).

Customers are now being referred to as users, and, as such, commanding more respect (and capital) from the investor class as a result of doing so. Customers is an unsexy term, with the connotation that they must continually be sold to and “reacquired.” Users, on the other hand, mustn’t be reacquired because they are always there. I get a customer, I keep a user. “What’s in a name? that which we call a rose. By any other name would smell as sweet.” Poor Romeo would be lost today. As inventive as he was, even William Shakespeare couldn’t have envisioned a society in which money was free. He died a century before the dawn of equity funding – in his day, it cost an average of 4 percent to borrow from either a British bank or a Medici money lender in the Italian nation states. In fact, the plot of The Merchant of Venice literally depends on the premise of capital having a cost attached to it. Shylock was ready to maim to collect the interest owed – his pound of flesh.

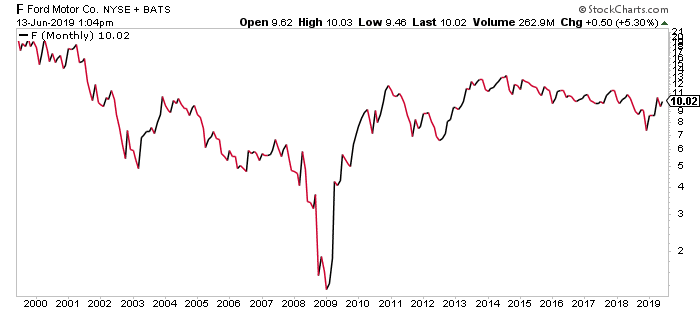

If Ford Motor were a savvier marketer of their stock, which has changed hands at more or less the same price for twenty years, they’d be calling buyers of their cars a user base and the cars themselves would be rechristened “physical mobility apps.” But they are dumb, and so Ford, with all of its heritage and legacy assets, is considered to be worth less than nothing by the modern marketplace for money and attention.

Bernstein’s Question

Bernstein’s question, left unanswered as all large and weighty contemporaneous questions about human civilization must be, introduces additional mysteries that we can only guess at.

Here are some additional questions I cannot answer:

Will “real” assets remain permanently undervalued relative to brand and intellectual capital forever?

Will the entire business of securities analysis institutionally restructure itself to account for this new reality, prizing other facets of a corporate issuer of securities more highly than projected cashflows and balance sheets?

What, if anything, could possibly come along to change the investor class’s attitudes about this?

Is it true that every time a purported “value investor” invents a justification for buying Amazon shares, an angel has its wings ripped off?

Do we simply need a recession for the old attributes of value stocks to shine through? What if that only makes it worse, given that in times of low cyclical growth, companies with high secular growth become even more sought after?

Would a sudden and long-term rise in the price of money and the cost of capital upend everything I’ve written here and completely reverse the lines on my chart, as a railroad worker throws the switch and sends itinerant trains onto completely different tracks?

Did I just call the top in the decade-long growth-versus-value massacre?

I don’t know the answers. You have opinions, but you can’t know for sure either. Maybe we need the last active pure-value manager on The Street to close up shop and retire as our signal. It’ll never happen. Even the buyers of stocks like Workday and ServiceNow and Zoom are convincing themselves that they’re playing a “relative” value game, and can always find things more obscene to point to in their quarterly virtue-signaling.

Paying Your Borrower

In 2016, I imagined the perfect startup business for this moment in time, not thinking back then that what I’d used as a parody would come closer to being a reality three years later:

Here’s the perfect business idea for this environment: Open a Hundred Dollar Bill Store™. You sell hundred dollar bills for ninety dollars each. You’ll lose ten dollars per transaction but you’ll do a trillion in revenues in year one. Maybe you show an ad to everyone who walks into the store and you break even. User growth with be on the order of 1000% per month. A billion users. You’ll be the biggest IPO of all time when Goldman’s underwriters get wind of that growth rate. Go public and let someone else worry about a competitor selling hundred dollar bills for eighty-five.

As ridiculous as that seemed at the time, it is today slightly less ridiculous, in a world where $20 trillion of the $55 trillion in global sovereign bonds currently yield zero percent or less. There is even a negative interest rate in same cases, with German citizens and other buyers paying the German government a quarter of one percent each year for the privilege of lending it money. What foul vision of unsurvivable torment, on earth or in hell, could the “investors” in these bonds possibly be running from when they consider the alternatives and decline?

Talk to a venture investor these days and they’ll tell you the single thing they don’t need more of is money. We have so much money in this new world we’re inventing new digital forms of currency just to have a place to stuff it all. Capitalists need ideas, talent, attention, audience, anything but more capital. Please don’t give me more. I can barely earn a lower-risk return on what I already have!

Which would you rather have?

Joking around with no one in particular, I asked which currently had more value – having a generic four-year degree from Anytown University, or an Instagram account with a million followers?

It was a Twitter survey and the results were what you’d have expected. Voters in the poll overwhelmingly chose the followers as having more value. Instagram doesn’t pay you a dollar for your follower count. It’s worth nothing on paper. But, as in most things in life, it can be an asset to you if you know how to use it. That right there is the intangible thing that everyone wants right now.

The following represents the power and reach of your brand. The college degree, in this analogy, is also an asset that you must make use of, but it is seen to be of substantially lower value given the ubiquity of young and middle-aged people in the labor force who also have one.

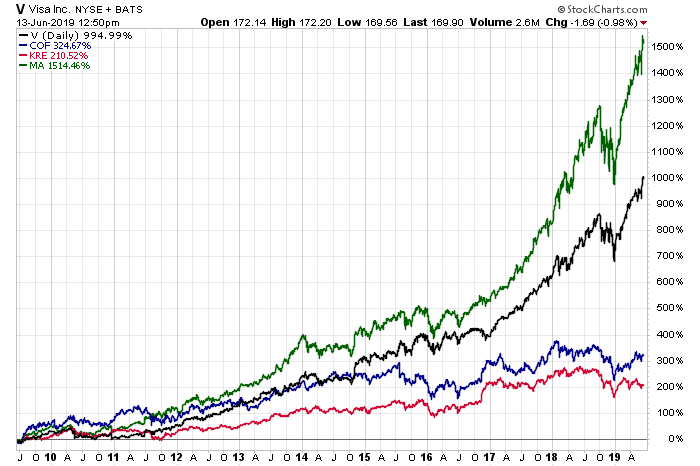

You’re a CEO in the financial sector. Which would you rather have as your corporation’s main asset, a chain of marble-floor main street bank branches or the payment network of Visa or Mastercard? We know what your potential shareholders would prefer you had. Here’s the regional bank stock ETF versus the interchange fee credit card giants, who collectively have zero bank branches despite being in the business of money changing hands and consumer borrowing:

Red is the regionals. Meh. Black and Green is Visa and Mastercard. The holy grail. And just for fun I snuck in Capital One Financial (in blue) – it’s in the credit card issuance game and the regional bank game, and still it’s done less than the S&P 500 since the crisis ten years ago.

In the battle for capital right now, the brands and intangibles and user bases and networks are winning by a landslide against the things that used to be important. And the companies that are rich in those old fashioned things, like Walmart, Disney and McDonalds, are spending all of their time and attention to transform themselves into the spitting image of their upstart competitors. Disney wants to look like Netflix, Walmart wants to retail like Amazon, McDonalds wants to be as habit-forming and celebrated for its freshness as its former protege Chipotle is. Goldman Sachs wants to grow up to be BlackRock. And in emulating these younger models, they hope, their multiples will soon be following suit.

And as for those stodgy old stalwarts of the 20th century that aren’t pursuing this transformation…it remains to be seen whether the rusty old assets they do possess will ever matter to investors ever again.

… [Trackback]

[…] Information to that Topic: thereformedbroker.com/2019/06/13/when-everything-that-counts-cant-be-counted/ […]

… [Trackback]

[…] Find More to that Topic: thereformedbroker.com/2019/06/13/when-everything-that-counts-cant-be-counted/ […]

… [Trackback]

[…] Find More on that Topic: thereformedbroker.com/2019/06/13/when-everything-that-counts-cant-be-counted/ […]

… [Trackback]

[…] Read More Info here on that Topic: thereformedbroker.com/2019/06/13/when-everything-that-counts-cant-be-counted/ […]

… [Trackback]

[…] Info on that Topic: thereformedbroker.com/2019/06/13/when-everything-that-counts-cant-be-counted/ […]

… [Trackback]

[…] Read More to that Topic: thereformedbroker.com/2019/06/13/when-everything-that-counts-cant-be-counted/ […]

… [Trackback]

[…] Read More to that Topic: thereformedbroker.com/2019/06/13/when-everything-that-counts-cant-be-counted/ […]

… [Trackback]

[…] Read More here on that Topic: thereformedbroker.com/2019/06/13/when-everything-that-counts-cant-be-counted/ […]