Throughout the summer, various cartoon characters throughout the financial media have been relentlessly pointing out some divergences in the stock market between internals and price.

The S&P 500’s price has been doing just fine, hanging around just below all-time highs hit during the winter and then finally bursting through, accompanied by a new record high for the Dow Jones yesterday.

But beneath the surface, some stocks had been doing better than most of the other stocks. To which poorly-trained or ill-informed commentators attached a ton of importance, despite the obvious fact that every single bull market throughout history has had leadership stocks that separated themselves from the pack and that this represents a totally normal Pareto–esque condition.

“But this sector isn’t doing as well as that sector!” they’d tweet, as though this observation had any profundity or carried with it even the hint of an implication for the future course of market prices. “But not every stock is making a new high with the index!” they’d warn, as though the alternative – a lockstep march higher of all index components – is something that we should ever expect to see.

The thing about divergences is that there are two ways for a divergence to resolve. One possibility is that the divergence is a signal that the market is about to change direction to match whatever is happening to the internals, good or bad. In which case, the person pointing the divergence out will be lauded for having seen it coming.

But then there’s what actually happens, most of the time: The primary trend that is already established reasserts itself, and the internal divergences are “resolved” back into agreement.

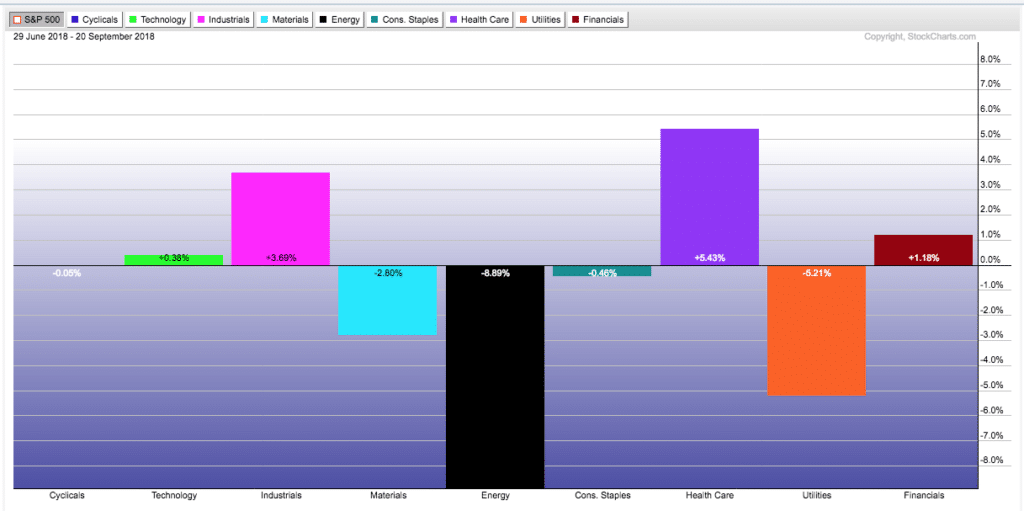

Here’s a look at how S&P 500 sector SPDRs have done since the start of the 3rd quarter we’re now getting to the end of. It’s not “all tech”. In fact, many sectors, especially health care and industrials, are doing substantially better. Tech, as a sector, is virtually flat.

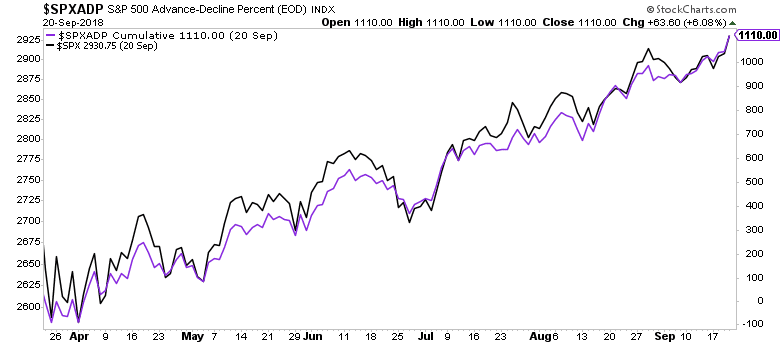

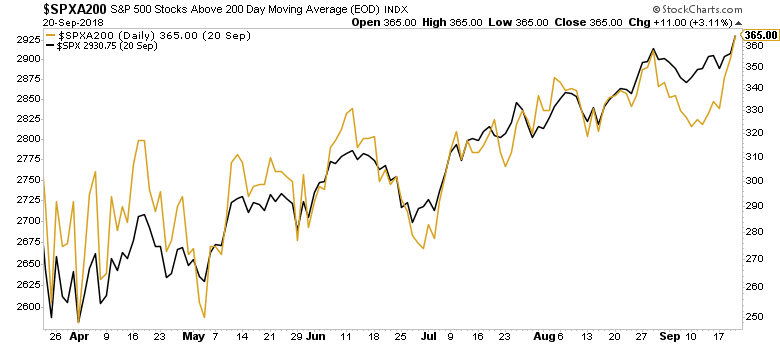

Have a look at the two charts below. You can see the divergences from the S&P 500 index, which eventually resolved to the upside as the index made new price highs.

Here’s that advance-decline line (shown cumulatively, purple) for S&P 500 stocks vs the index itself (black). You can see that moment of separation at the end of August. This was a divergence that was much remarked upon at the time.

Now that’s it has resolved to the upside, the people who did the remarking will not come back out and mention it again. They’re on to the next nonsensical bullshit they can cook up and serve to the crowd. It pays the bills.

Below is the S&P 500, again in black, versus the percentage of S&P 500 stocks that are currently above their own 200-day moving averages. Once again, you see a gap or divergence between the index and the internal metric in late August / early September and, yes, once again you see this divergence being resolved to the upside – the internals now matching the index’s direction as new highs are taken out.

Sometimes there are divergences worth noticing and even pointing out. I’m cool with this. Sometimes there are people who get their hands on a piece of information and are so uninformed and without context that they end up embarrassing themselves.

Sometimes it would be better to listen to others.

Sometimes it would be better not to see the conclusion you’ve already drawn reflected back to you in every new data point, and every new movement on a chart.

Sometimes it would be better to sit quietly and try to learn something new from people who know what they’re talking about. Even if it’s your job to have an opinion, saying that you don’t have a strong one or that you’re unsure of something is a perfectly valid stance.

Sometimes it would be better to just say nothing.

[…] ‘Sometimes it Would Be Better to Just Say Nothing’ – Josh Brown – The Reform… […]

[…] Throughout the summer, various cartoon characters throughout the financial media have been relentlessly pointing out some divergences in the stock market between internals and price. The S&P 500’s price has been doing just fine, hanging around just below all-time highs hit during the winter and then finally bursting through, accompanied by a new record high for the Dow Jones yesterday. But beneath the surface, s… Source: http://thereformedbroker.com/2018/09/21/sometimes-it-would-be-better-to-just-say-nothing/ […]

… [Trackback]

[…] Read More to that Topic: thereformedbroker.com/2018/09/21/sometimes-it-would-be-better-to-just-say-nothing/ […]

… [Trackback]

[…] Here you can find 54297 more Information to that Topic: thereformedbroker.com/2018/09/21/sometimes-it-would-be-better-to-just-say-nothing/ […]

… [Trackback]

[…] Read More here to that Topic: thereformedbroker.com/2018/09/21/sometimes-it-would-be-better-to-just-say-nothing/ […]

… [Trackback]

[…] Information to that Topic: thereformedbroker.com/2018/09/21/sometimes-it-would-be-better-to-just-say-nothing/ […]

… [Trackback]

[…] Find More on to that Topic: thereformedbroker.com/2018/09/21/sometimes-it-would-be-better-to-just-say-nothing/ […]

… [Trackback]

[…] Find More on that Topic: thereformedbroker.com/2018/09/21/sometimes-it-would-be-better-to-just-say-nothing/ […]

… [Trackback]

[…] Information on that Topic: thereformedbroker.com/2018/09/21/sometimes-it-would-be-better-to-just-say-nothing/ […]