The Wall Street Journal is reporting this morning that household debt grew in 2016 by the most in almost a decade. The composition is different (more auto, less mortgage) but this is exactly what the Federal Reserve has been trying to produce all this time – velocity of money moving throughout the economy.

Total household debt climbed by $226 billion in the final three months of 2016, according to a report Thursday from the Federal Reserve Bank of New York. Total household debts are now just $99 billion shy of the all-time peak of $12.7 trillion set in the third quarter of 2008 just as the banking system began crashing down. The New York Fed estimates that debt is highly likely to set a new record in 2017.

But “a new record” should be looked at in the context of the overall economy, not nominally. We’re not nearly in the same place we were headed into the financial crisis when viewed correctly, as Josh Zumbrun points out:

The New York Fed doesn’t adjust its figures for inflation. When measured against the broader economy, total household borrowing today is 67% of nominal gross domestic product, compared with about 85% in 2008.

The bad news is that much of the growth in household indebtedness has come from student and auto loans. The Fed’s data on auto loan delinquencies this week is somewhat troubling. Here’s the New York Post:

Auto loan delinquencies in the fourth quarter hit their highest level since the financial crisis, a report out Thursday revealed.

About $23.27 billion in loans were 30 days or more late as of Dec. 31 — a whopping 14 percent increase from the year earlier and the most since the $23.46 billion in the third quarter of 2008, according to the New York Federal Reserve.

Delinquencies have moved up as the credit quality of the loans has deteriorated and the length of the auto loans has increased — sometimes to 84 months.

Sounds scary. But – when you look at the breakdown between subprime auto loans and regular auto loans, it’s not quite so dire:

It calculated that subprime borrowers accounted for about $280 billion in auto loans in the fourth quarter — not notably different from the $345 billion in auto loans attributed to the most creditworthy borrowers (those who had credit scores above 760).

Almost all borrowers with credit scores above the subprime cutoff of 620 are “performing very well,” it said.

As far as the student loans thing, yeah, it sucks that young people have to go deep into debt to secure a future for themselves. Student loans outstanding now total $1.3 trillion and there is no doubt that this has held back household formation – one of the primary drivers of any economic expansion.

But young people (and their families) are merely responding to a bigger truth – which is that the unemployment rate for college graduates is practically non-existent at this point and earnings for grads are significantly higher than for non-grads. College degrees are a de facto prerequisite for being able to survive in this country circa 2017. Viewed this way, $1.3 trillion in outstanding loans makes sense – it’s an economic incentive that people are responding to. We could argue about whether or not college should cost less or be more subsidized by government, but that’s a different discussion.

Here’s Forbes:

As of the January 2017 report which contains numbers for December 2016, the unemployment rate for college graduates was only 2.5 percent. That means that only one out of every 40 college graduates is unemployed. This is half the unemployment rate of those with high school degrees and one-third the unemployment rate of those with without a high school degree.

Economists refer to 2.5% as being “frictional” – meaning it’s perfectly normal and reflects people leaving one job for another on an ongoing basis. You don’t get lower than 2.5% in the real world.

Which leads me to a look at the banks themselves, who are making these loans. They’re doing just fine. Dodd Frank regulations have not been holding back borrowing or lending to a significant degree. Financial institutions have seen the business climate improving in-line with the broader improvement in the overall economy – slow, but steady.

With the exception of Citigroup, all of the Big Six are now selling above tangible book value on the stock market. They’ve had a big run since the election of Donald Trump, in anticipation of a dismantling of regulation. But they were also already running up beforehand – because rates were rising and the economy has been improving, way in advance of the election.

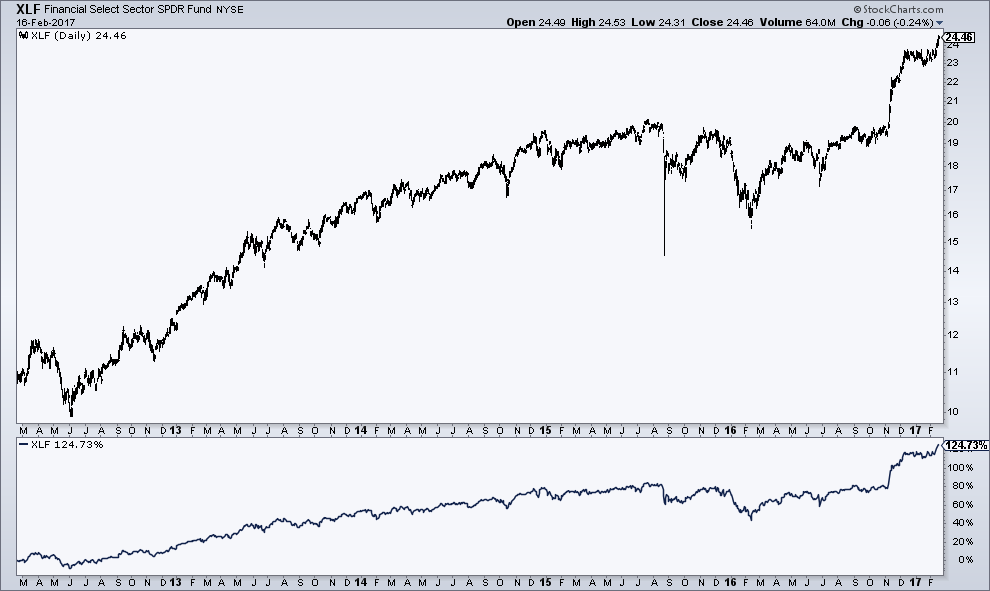

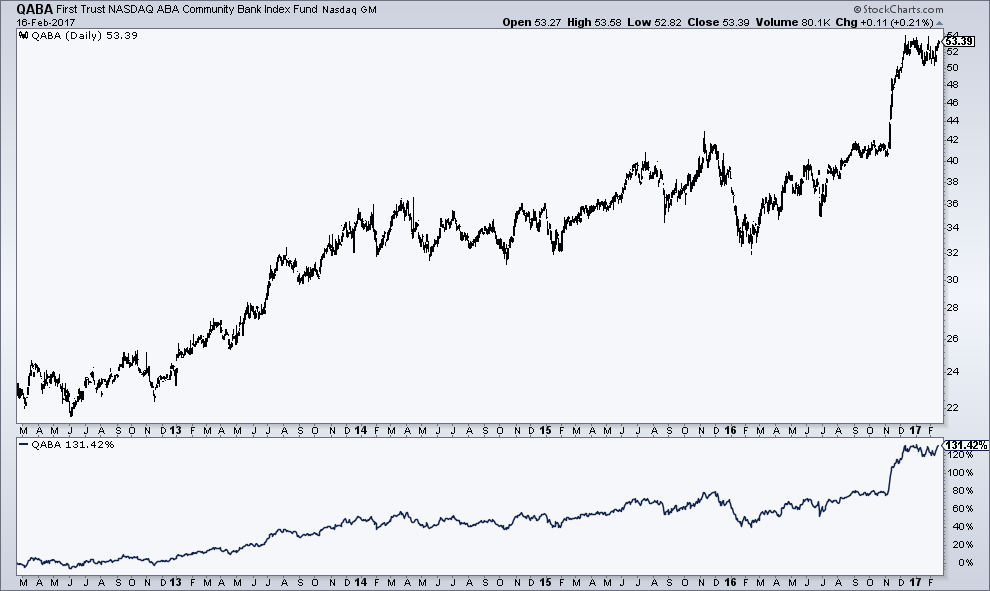

Here’s a look at three representative ETFs, in which you’ll see sentiment and valuations improving both before and after November…

First, the big financials over the last 5 years, as represented by the Financial Select Sector SPDR, XLF (price in the top pane, percentage performance in the below):

Next, the SPDR S&P Regional Banking ETF, also doing just fine before and after:

Finally, the allegedly beleaguered thrift and community banks, as represented by the First Trust NASDAQ ABA Community Bank Index Fund:

Again – a nice recent spike which merely punctuates a gradually improving environment since 2012. In fact, the QABA ETF is annualizing at almost 19% over the last five years.

Now, it is true that commercial real estate loan conditions are tightening a bit, so Trump’s anecdote about how he has a friend with a tremendous nice business who is having trouble borrowing is not totally false, but it’s a story, not a data point – and certainly not enough to take a chainsaw to the rulebooks again.

And of course, we’d like to see more C&I loans (commercial and industrial) to jumpstart business development, but that’s already underway. As James Saft at Reuters pointed out a week ago, “commercial and industrial (C&I) loans are now higher as a percentage of economic output than they’ve been since the 1980s, when the capital markets were far smaller and the economy more reliant on direct finance via banks.”

When bankers complain, the rhetoric is almost always a caricature of the reality. Today is no different. There’s probably room to streamline or clean up the crisis era regs, but to make the claim that “the banks can’t lend” flies in the face of the actual facts.

[…] Banks CAN lend. Everything else is just rhetoric. (thereformedbroker) […]

[…] or thankless cause, doing the real work to demonstrate the facts. This week’s award goes to Josh Brown for his thoughtful analysis of debt, and what it really means. The arguments about excessive debt, […]

[…] or thankless cause, doing the real work to demonstrate the facts. This week’s award goes to Josh Brown for his thoughtful analysis of debt, and what it really means. The arguments about excessive debt, […]

[…] or thankless cause, doing the real work to demonstrate the facts. This week’s award goes to Josh Brown for his thoughtful analysis of debt, and what it really means. The arguments about excessive debt, […]

[…] or thankless cause, doing the real work to demonstrate the facts. This week’s award goes to Josh Brown for his thoughtful analysis of debt, and what it really means. The arguments about excessive debt, […]

[…] or thankless cause, doing the real work to demonstrate the facts. This week’s award goes to Josh Brown for his thoughtful analysis of debt, and what it really means. The arguments about excessive debt, […]

… [Trackback]

[…] Read More on that Topic: thereformedbroker.com/2017/02/17/dodd-frankly-speaking/ […]

… [Trackback]

[…] Read More here on that Topic: thereformedbroker.com/2017/02/17/dodd-frankly-speaking/ […]

… [Trackback]

[…] Information on that Topic: thereformedbroker.com/2017/02/17/dodd-frankly-speaking/ […]

… [Trackback]

[…] Read More to that Topic: thereformedbroker.com/2017/02/17/dodd-frankly-speaking/ […]

… [Trackback]

[…] Read More here on that Topic: thereformedbroker.com/2017/02/17/dodd-frankly-speaking/ […]

… [Trackback]

[…] Find More here on that Topic: thereformedbroker.com/2017/02/17/dodd-frankly-speaking/ […]

… [Trackback]

[…] Read More to that Topic: thereformedbroker.com/2017/02/17/dodd-frankly-speaking/ […]

… [Trackback]

[…] Info on that Topic: thereformedbroker.com/2017/02/17/dodd-frankly-speaking/ […]

… [Trackback]

[…] Info to that Topic: thereformedbroker.com/2017/02/17/dodd-frankly-speaking/ […]