Why have stock-picking fund managers had it so tough over the last few years? A lot of people would say high correlation in the stock market, but that’s only part of the story. According to Goldman Sachs strategists, the real culprit is low dispersion. We’ve talked about this topic here before, but to rehash: Dispersion is a measurement of how stocks act in relation to each other, not just to the overall market.

A high-dispersion environment is where a large number of stocks are zigging and zagging drastically. This means that returns and risk factors are all over the map, which, in theory, would allow skilled stock-pickers to greatly differentiate themselves. In a low-dispersion environment, which is what Goldman expects to continue throughout 2015, it’s harder to select stocks that will move meaningfully based on individual company micro-drivers (fundamental changes, news, etc).

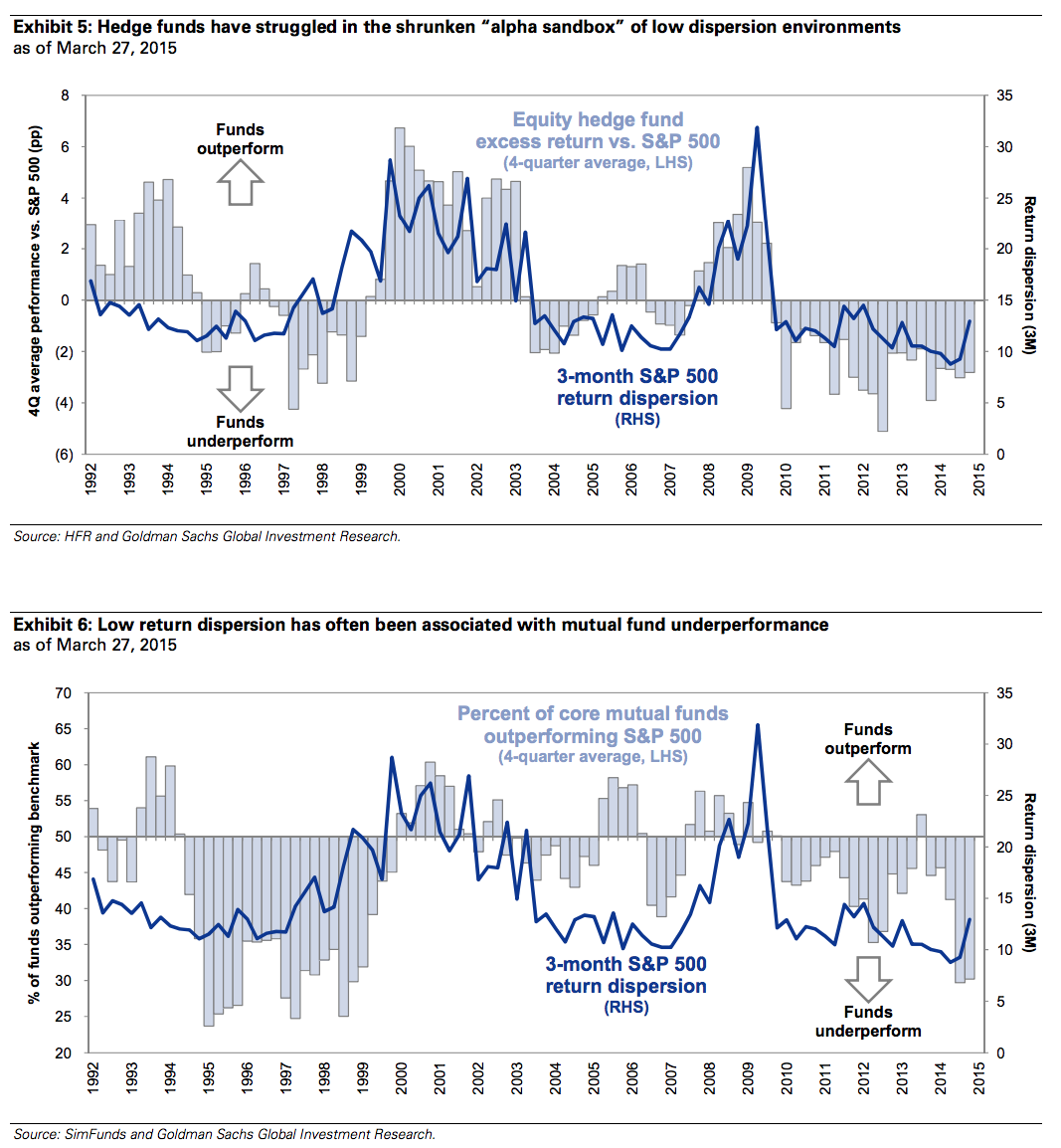

The two charts below show how the stock-pickers struggle when dispersion is low and alpha grows scarce:

You’ve also likely noticed that funds have trouble outperforming during bull markets generally, but we’ve been over that too (see: Why Active Management Fell Off a Cliff).

Strategist David Kostin & Co ran an analysis that measured the S&P 500 stocks for dispersion potential and the tendency to move independently.

They find that the stocks with the potential for high dispersion are most likely to fall into either the information technology or consumer discretionary sectors. This makes intuitive sense – consumer disc companies see radical changes in stock price as a result of the capricious preferences of shoppers while in technology, individual-company innovation is the big driver. Energy, materials and staples – with largely commoditized products to sell – tend to see the lowest amount of dispersion among their stocks.

GS emphasizes that picking stocks with high-dispersion tendencies will be the key to outperformance this year, long or short. The best hunting grounds are in the retailers, techs, biotechs and luxury brands.

Source:

Picking stocks in a low return dispersion market Goldman Sachs – March 30th 2015

[…] According to Goldman Sachs, increased dispersion almost always leads to a higher percentage of stockpickers outperforming, as their skills in deciding winners from losers become more useful: […]

[…] It is important to note that while we always root for a “stock picker’s market,” it does not follow that in such markets active managers will do well in aggregate. This study from S&P Dow Jones undermines the idea (at least for the recent past) that higher dispersion leads to better results for active management as a whole. I think this may have something to do with the fact that so many more managers are “closet indexers” in this sample of years than in the past, but the results are still interesting. Josh Brown has also explored this same topic. […]

I’m a New York City-based financial advisor at Ritholtz Wealth Management LLC. I help people invest and manage portfolios for them. For disclosure information please see here.

Subscribe & Reform

Get a Full Investor Curriculum: Join The Book List

Every month you'll receive 3-4 book suggestions--chosen by hand from more than 1,000 books. You'll also receive an extensive curriculum (books, articles, papers, videos) in PDF form right away.

RT @asibiza1: The trouble with a large number of stocks are zigging and zagging all over the place… @ReformedBroker http://t.co/HLuFZJUbo8

[…] Joshua M Brown Why have stock-picking fund managers had it so tough over the last few years? A lot of people would […]

RT @ReformedBroker: How Dispersion Stole the Alpha

http://t.co/OFBiyeNaFe http://t.co/7bviCUEowz

Chart o’ the Day: How Dispersion Stole the Alpha by @ReformedBroker http://t.co/sTjC7EN9yP

RT @MStarETFUS: Chart o’ the Day: How Dispersion Stole the Alpha by @ReformedBroker http://t.co/sTjC7EN9yP

Chart o’ the Day: How Dispersion Stole the Alpha by @ReformedBroker http://t.co/Yfx3WkPGWA

How hedge funds are still sucking, thanks to dispersion…excuses excuses.

http://t.co/j0GJH7KXLh #markets #feedly

Why have stockpickers had it so tough recently? Low dispersion according to @ReformedBroker

http://t.co/AxrNsgVZEj http://t.co/aMOpAug8CN

[…] Joshua Brown: Chart o’ the Day: How Dispersion Stole the Alpha […]

@michaelbatnick @millennial_inv Josh @ReformedBroker had a terrific post yesterday on this topic: http://t.co/aLsyInOGHS

RT @EnisTaner: @michaelbatnick @millennial_inv Josh @ReformedBroker had a terrific post yesterday on this topic: http://t.co/aLsyInOGHS

[…] According to Goldman Sachs, increased dispersion almost always leads to a higher percentage of stockpickers outperforming, as their skills in deciding winners from losers become more useful: […]

[…] It is important to note that while we always root for a “stock picker’s market,” it does not follow that in such markets active managers will do well in aggregate. This study from S&P Dow Jones undermines the idea (at least for the recent past) that higher dispersion leads to better results for active management as a whole. I think this may have something to do with the fact that so many more managers are “closet indexers” in this sample of years than in the past, but the results are still interesting. Josh Brown has also explored this same topic. […]

… [Trackback]

[…] Find More Information here to that Topic: thereformedbroker.com/2015/03/31/chart-o-the-day-how-dispersion-stole-the-alpha/ […]

… [Trackback]

[…] Here you can find 92536 more Info on that Topic: thereformedbroker.com/2015/03/31/chart-o-the-day-how-dispersion-stole-the-alpha/ […]