Neil Irwin at the Upshot takes a look at a new study by McKinsey on the total indebtedness of the world. Intuitively, one would suspect that the aftermath of a global debt crisis would lead to significantly less debt being taken on by countries and businesses, stung by the bust. One would be wrong, in this case, as overall debt levels have soared virtually everywhere.

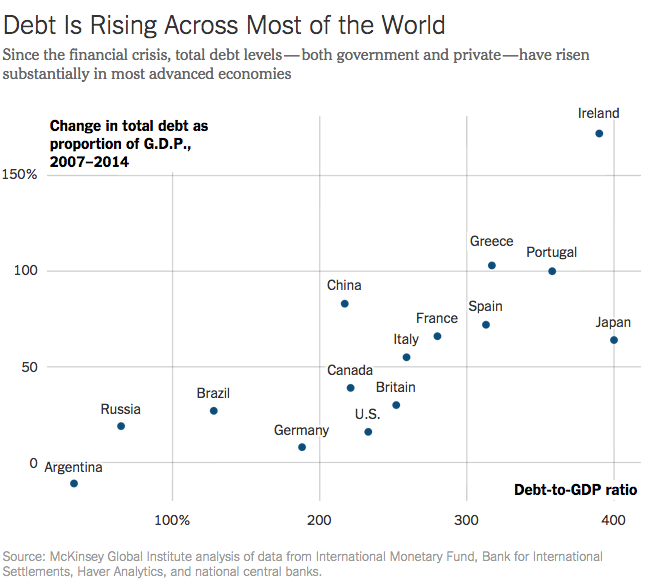

Below, you’re looking at the growth in overall debt by country, with the zero baseline on the X axis representing 2007…

Irwin says this either matters a great deal or not much at all…

Here are two things we know about how debt affects the economy.

First, in the abstract it doesn’t matter. For every debtor there is a creditor, and in theory an economy should be able to hum along just fine whether a country’s citizens have a great deal of debt or none. A company’s ability to produce things depends on the workers and machines it employs, not the composition of its balance sheet, and the same can be said of nations.

Second, in practice this is completely wrong, and debt plays an outsize role in creating boom-bust cycles across the world and through history. High debt increases the amplitude of economic swings. To think of it in terms of the corporate metaphor, high reliance on borrowed money may not affect a company’s level of output in theory, but makes it a great deal more vulnerable to bankruptcy.

Josh here – I’ll take the “in practice” explanation over the “in theory” version any day of the week. Head over to read the whole piece.

I’m a New York City-based financial advisor at Ritholtz Wealth Management LLC. I help people invest and manage portfolios for them. For disclosure information please see here.

Get a Full Investor Curriculum: Join The Book List

Every month you'll receive 3-4 book suggestions--chosen by hand from more than 1,000 books. You'll also receive an extensive curriculum (books, articles, papers, videos) in PDF form right away.

… [Trackback]

[…] Information on that Topic: thereformedbroker.com/2015/02/07/chart-o-the-day-global-debt-rises-by-57-trillion-in-7-years/ […]

… [Trackback]

[…] Read More Info here to that Topic: thereformedbroker.com/2015/02/07/chart-o-the-day-global-debt-rises-by-57-trillion-in-7-years/ […]