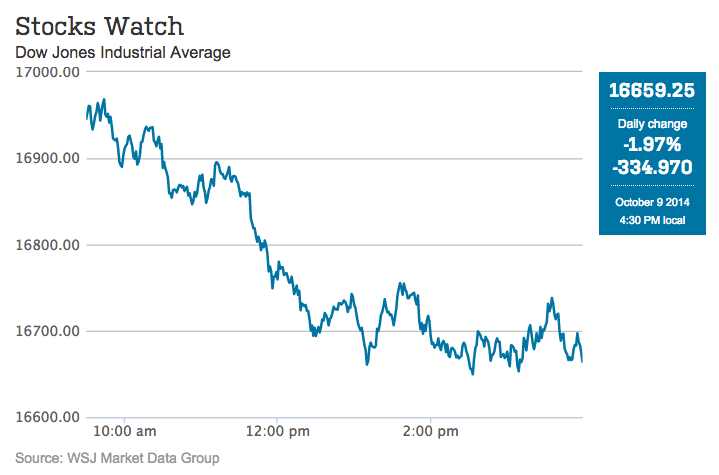

Why did the stock market plummet more than 330 points today?

I could give you any one of several answers but they won’t actually help you. Because this is the wrong question.

The right question is to ask why it went up an almost equivalent amount yesterday. And the answer to that is people are out of their f***ing minds.

They’re nostalgic for the sentiment-driven, Fed-fueled, multiple expansion market of 2013 and they haven’t yet accepted the fact it was a once (maybe twice) in a lifetime thing. The conditions that were in place to set up what happened in 2013 were the following:

1. Everyone was underinvested in stocks, overly invested in cash, gold and bonds.

2. The Fed was furiously pumping dollars directly into the investment markets, fueling all manner of buybacks, IPOs and raised dividends.

3. Sentiment was absurdly pessimistic, with Wall Street, institutional investment managers and retail players negative on equities.

4. US companies were consistently smashing expectations and raising guidance for the future.

5. The rest of the world began reporting improving economic fundamentals.

That was then. I documented the shit out of this phenomenon that entire year, until my fingers bled from blogging.

This year, many of those factors are non-existent or on the wane.

Consider:

1. Investors are no longer underinvested in stocks. According to the Federal Reserve’s Flow of Funds report, we’re back at all-time peaks (last seen in 2000, 2007) for household corporate equity (stocks, mutual funds, corporate bonds) participation.

2. The Fed is walking away. Later this month, the taper of stimulus will have been concluded. After shoveling a trillion dollars a year at the investment markets, they are retiring from the QE business and merely pledging a low Fed Funds rate in lieu of stimulus. Investor demand must now stand on its own and you better believe things are going to adjust. Buybacks are expected to slow markedly from their torrid pace. It already began in the most recent quarter. IPO volume (in transactions, not dollars) has already dropped.

3. Sentiment from week to week has been volatile but the big picture is that people are back in again. All you need to do is to look at the inflows to Vanguard’s passive stock index products and the record levels of 401(k) buying to know that. Never listen to a survey, watch what their hands are doing, not what their lips are saying.

4. US companies are not smashing anything. Their beats have become more modest. Their warnings have become more grave. There are many high profile blue chip companies that have already thrown in the towel on 2014, most notably Target and Ford. There’s plenty of good news on the earnings front (mostly in tech, select consumer discretionary), but there is less surprisingly good news overall. Expectations are everything. We’re already expecting a lot.

5. The rest of the world is not only not improving, it’s becoming a disaster. Europe is looking at a continent-wide triple-dip recession. An absolute absurdity, and yet here it is. Japan is going nowhere, China’s slow-mo unwind continues apace and the commodity collapse / dollar rally is killing off any hope of strength around the rest of the emerging world.

And so with the five factors that had driven the rally since 2012 no longer in our favor, we consolidate and thrash around a bit awaiting the next set of catalysts. Maybe a great holiday shopping season thanks to plunging energy costs. Perhaps – at long last – a meaningful uptick in wages for our now tighter labor market. Maybe European QE resets the board game there and sparks les esprits animaux. All of these things are possible – they’re just not happening yet.

And so volatility ticks up and the crowd second-guesses everything in their portfolios.

Welcome to the next phase. The old phase has been over for awhile, I’m sorry that nobody rang a bell or hung a sign.

Read Also:

Stocks Explode Higher on Fears of Renewed Economic Weakness (TRB)

RT @ReformedBroker: WHY DID THE STOCK MARKET PLUMMET TODAY? http://t.co/5m4BFxKZRC $SPY $DIA $QQQ $IWM

Why did the stock market plummet today? by @ReformedBroker http://t.co/8OQMcsqAOA

[…] M. Brown at The Reformed Broker gives some answers to what happened this week, mostly on the no-real-big-deal […]

Why did the stock market plummet today? http://t.co/uh5Nq9p37P

Great reality check from @ReformedBroker -> Why did the stock market plummet today? http://t.co/nD7FA3S4mD #investing #markets #stocks

RT @ReformedBroker: Why did the stock market plummet yesterday? Five key factors from the 2013 miracle are no longer in place… http://t.co/…

Why Did The Market Plummet Today? Wrong question folks ….@ReformedBroker with a wake up call. What to do now? http://t.co/HtQTx9njrO

All you need to know : Why did the stock market plummet today? by @ReformedBroker http://t.co/6LoSUYEluV #tellitbrother #notlikeoldtimes

Why did the stock market plummet today? by @ReformedBroker http://t.co/cX9I5m1RRN 미증시 급란이유를 잘 설명한 글

RT @sambonfante: What was behind yesterday’s stock market dive? http://t.co/n6K8LC2g7x

RT @ReformedBroker: WHY DID THE STOCK MARKET PLUMMET TODAY? http://t.co/WU2qxH7tV6 $SPY $DIA $QQQ $IWM

RT @sambonfante: What was behind yesterday’s stock market dive? http://t.co/n6K8LC2g7x

RT @sambonfante: What was behind yesterday’s stock market dive? http://t.co/n6K8LC2g7x

RT @paulwoll: RT @ReformedBroker: WHY DID THE STOCK MARKET PLUMMET TODAY? http://t.co/WU2qxH7tV6 $SPY $DIA $QQQ $IWM

RT @sambonfante: What was behind yesterday’s stock market dive? http://t.co/n6K8LC2g7x