Watch as Eric D. Nelson, CFA, of Servo Wealth Management demolishes the bubble meme in a new post at his blog this week…

Probably the best method of “bubble detection”, to the extent such a thing is even possible, is to simply observe an investment’s recent past performance history to measure how far in excess of the long-term average it has been. For example, Gold experienced a ten-year run starting in 1971 where it returned almost 32% per year. US small cap stocks earned 27% per year for the decade ending in 1984. And Japanese stocks produced over 28% per year returns in the 1980s. All of these results were well above long-term expectations and unsustainable, as each market eventually “reverted to the mean.” Have we reached this point again?

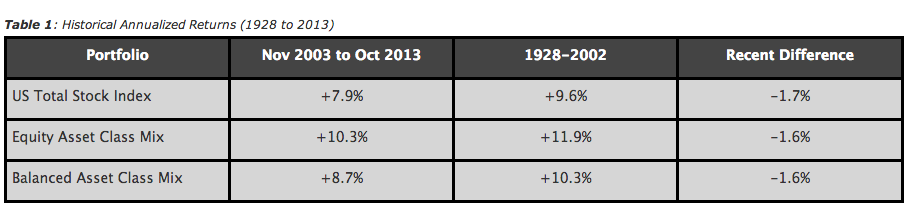

Table 1 looks at three different investment portfolios: a traditional US total stock index, followed by two more diversified asset class mixes—an all-stock allocation (“Equity”) and a balanced stock and bond combination (“Balanced”).

For the recent ten-year period, investment returns have been healthy despite the debilitating setback in 2008. The US Total Stock Index earned almost 8% per year. But this is far from an alarming rise in prices, as the average over the previous 75 years was 1.7% higher, at +9.6% per year. So far, so good. If lower-than-average returns have created a market bubble, that would certainly be the first time.

Josh here – Stocks are supposed to go up over 10-year periods and they almost always do – 88% of rolling 10-year periods over the last 89 years have shown a positive return for the US market. Looking at the last ten years, even with the inclusion two mega rallies and a massive bear market, we’re just now getting back to historical return averages.

Shall we pause here and reverse or shoot all the way through to a real bubble? That’s the more important question.

I’m a New York City-based financial advisor at Ritholtz Wealth Management LLC. I help people invest and manage portfolios for them. For disclosure information please see here.

Subscribe & Reform

Get a Full Investor Curriculum: Join The Book List

Every month you'll receive 3-4 book suggestions--chosen by hand from more than 1,000 books. You'll also receive an extensive curriculum (books, articles, papers, videos) in PDF form right away.

… [Trackback]

[…] Find More here on that Topic: thereformedbroker.com/2013/11/29/not-a-bubble-just-the-old-normal/ […]

… [Trackback]

[…] Information on that Topic: thereformedbroker.com/2013/11/29/not-a-bubble-just-the-old-normal/ […]

… [Trackback]

[…] Find More here on that Topic: thereformedbroker.com/2013/11/29/not-a-bubble-just-the-old-normal/ […]

… [Trackback]

[…] Read More on on that Topic: thereformedbroker.com/2013/11/29/not-a-bubble-just-the-old-normal/ […]

… [Trackback]

[…] Info to that Topic: thereformedbroker.com/2013/11/29/not-a-bubble-just-the-old-normal/ […]

… [Trackback]

[…] Read More Info here on that Topic: thereformedbroker.com/2013/11/29/not-a-bubble-just-the-old-normal/ […]

… [Trackback]

[…] Read More to that Topic: thereformedbroker.com/2013/11/29/not-a-bubble-just-the-old-normal/ […]

… [Trackback]

[…] Find More Information here on that Topic: thereformedbroker.com/2013/11/29/not-a-bubble-just-the-old-normal/ […]

… [Trackback]

[…] Find More Info here on that Topic: thereformedbroker.com/2013/11/29/not-a-bubble-just-the-old-normal/ […]

… [Trackback]

[…] Info to that Topic: thereformedbroker.com/2013/11/29/not-a-bubble-just-the-old-normal/ […]

… [Trackback]

[…] Read More to that Topic: thereformedbroker.com/2013/11/29/not-a-bubble-just-the-old-normal/ […]