A fun chart I whipped up looking at Treasury bond yields by maturity, just for a frame of reference now that everyone’s carrying on about rising rates.

The truth is, rates have already been rising, for quite some time.

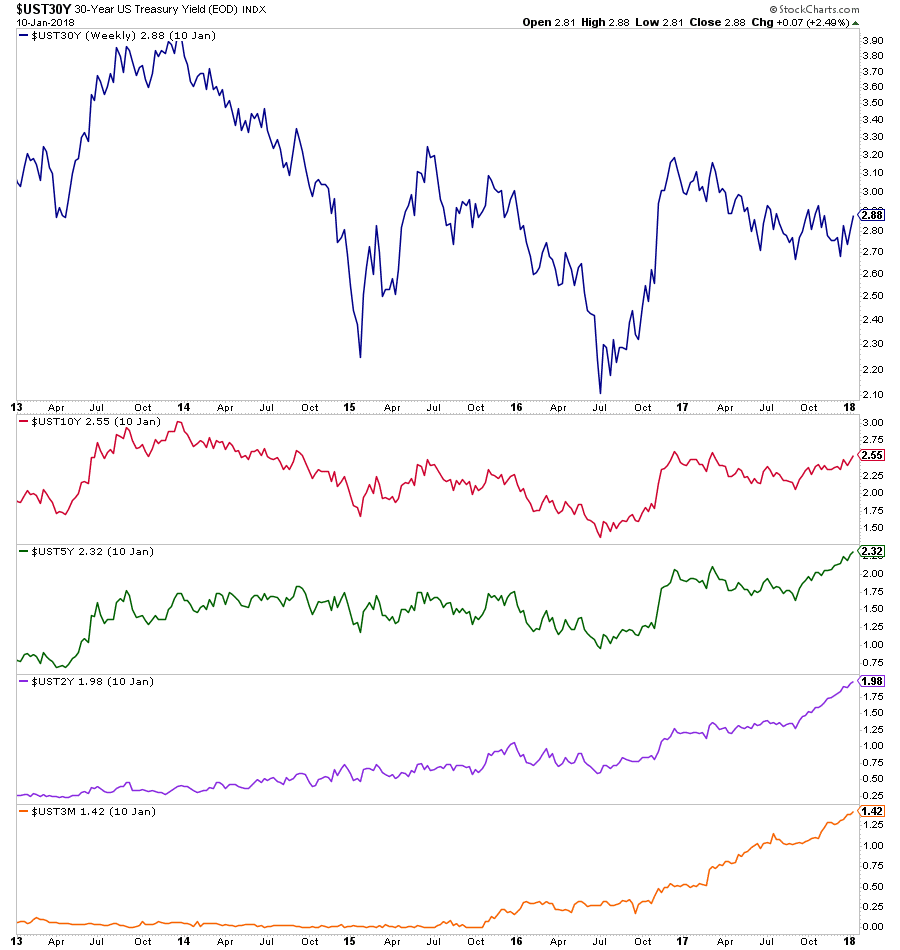

The long bond in the top pane finally found a real bottom in the summer of 2016 as the economic data around the world began to materially improve all at once. Global yields had dragged it down, so normalizing global yields were the only elixir. The Brexit non-event turned out to have been the signal. Who knew? Maybe this was the big, bad thing that investors were waiting to see us get past before raising their own expectations.

The 10-year Treasury played along, bottoming at pretty much the same time.

But the 5-year had already put in its lows years earlier after the Taper Tantrum in the summer of 2013. It had not revisited them in the summer of 2016 as longer-dated maturities made their ultimate lows.

Same for the 2-year and for 3-month paper. Bumping along the bottom and then a noticeable lift as the Fed began to raise overnight rates very slowly, deliberately and transparently.

We’ve been hearing about a bond catastrophe in the making for quite a while now. Meanwhile, rates have risen very gradually and the central bank has never been more open about their moves, telegraphing their actions in a way that watchers of the Greenspan era could only have dreamed of.

No such crisis has taken place yet as the Fed first began buying less during QE, then buying none, then began to talk about slowly winding down its portfolio. Overall, fixed income market participants have been extraordinarily well-behaved. Liquidity has not been a problem.

Bears will now screech at me that it’s because Bank of Japan and the ECB have picked up the slack and covered the Fed’s exit. Okay, so what? Was that some sort of shocking development that no one could have foresaw?

There’s a new guy running the Fed. His boss (let’s not kid ourselves about independence) is a President who loves to borrow money and makes it a point to reference the soaring stock market every time he finds his mouth in front of an open microphone. There’s no reason to think the pace of gradual hikes and constant market communication is going to change much through 2018.

I’m a New York City-based financial advisor at Ritholtz Wealth Management LLC. I help people invest and manage portfolios for them. For disclosure information please see here.

Get a Full Investor Curriculum: Join The Book List

Every month you'll receive 3-4 book suggestions--chosen by hand from more than 1,000 books. You'll also receive an extensive curriculum (books, articles, papers, videos) in PDF form right away.

… [Trackback]

[…] Read More here to that Topic: thereformedbroker.com/2018/01/11/when-did-rates-bottom/ […]