Yesterday I had the great pleasure of attending the 32nd Tiburon CEO Summit at the Ritz-Carlton Battery Park City. Chip Roame and Co filled the day with incredible speakers on every important topic for the wealth management industry.

(Jack Bogle talks with Tiburon’s Chip Roame)

Some quick insights I came away with.

Chip’s opening keynote is always a panoramic look around the industry and it never disappoints. He notes that there are 326.5 million people (consumers) in the United States today, comprising 125.6 million households. Collectively, they hold $42 trillion and change in investable assets and another $22 trillion in retirement plan assets. In other words, some $65 trillion in liquid assets to be managed by the investment industry.

This is on top of $11 trillion in small business value and another $29 trillion in personal assets and homes that they live in. Added together, US households have $107.9 trillion in total assets, with $15.1 trillion in total liabilities, or total household net worth of $92.8 trillion.

There are 1,826 billionaires in the United States and another 142,000 people with net worths exceeding $25 million.

This is a staggering amount of wealth.

Who is going to manage it?

The conclusion reached by both the audience taking a poll as well as by Chip, who is a leading consultant to the industry for 20 years, is that the only categories with meaningful growth in the space will be the RIA channel, the online brokerage channel and the digital advice channel. Everyone else is losing share and these trends should persist. It’s important to note that assets are triple-counted in this industry – in Chip’s example, if he buys a mutual fund from an RIA – the RIA counts the money as AUM, so does the mutual fund company and so does the RIA’s custodian.

There was a lot of talk about fee compression, both at the fund level and the advisory level. Advisors aren’t giving up their margins, so they’re turning to product companies that have lower fees to keep a lid on the all-in costs they’re showing to clients. As a general rule, “Whoever is the closest to the customer almost always eventually wins.” Put another way, the advisor who owns the relationships (distribution) will survive the downward pressure on fees better than the fund companies will. This is regardless of the “active-passive debate” or anything else.

On the whole fuss over millennials, Chip notes that, for the time being, they’re irrelevant to the wealth management industry. “93% of the assets in 401(k) plans are held by Boomers. For the next five years at least, that’s the market.”

On the breakaway broker trend of wirehouse advisors going to or starting RIAs, Chip says this is dramatically overstated and tiny relative to the amount of attention it receives. He calculates that only 500 successful wirehouse brokers make the move each year. “A guy who gets fired by UBS is not a breakaway broker.”

One of the few areas within asset management that is expected to see explosive growth (other than indexing) is socially responsible investing, which we call ESG at Ritholtz Wealth Management. Chip shows how globally, 60% + of all SRI assets are from Europe and the US is just getting started.

There’s $8.7 trillion managed according to some sort of socially responsible mandate in the US, but it is almost entirely institutional. “This is more than the entire hedge fund industry and the entire ETF industry – combined.” SRI is not yet a retail concept – the socially responsible mutual fund business, for example, is tiny. He thinks this is going to be the fat pitch for advisors over the coming decade as more and more people seek to align their values with their portfolios. It’s an area where advisors can differentiate themselves. (We agree, and would also point out that clients who believe in their portfolios are less apt to capriciously abandon them during market corrections.)

The consensus of the audience – all wealth management CEOs – is that hedge fund use will continue to decline and that the wirehouse channel will continue to lose relevance. The Department of Labor ruling on fiduciary standard of care being altered or pushed back or killed won’t change the death of commissions. He thinks there’s a chance that Merrill Lynch drops all transactional business and becomes the largest RIA in America at some point in the next few years.

Speaking of RIAs, he doesn’t think a majority of them are growing. Most of the growth is happening at the largest firms at this point, both organically and via acquisition. Smaller firms are already beginning to be left behind. It will be harder for them to compete as technology, compliance and other costs rise and practices become more sophisticated. This will drive continued consolidation.

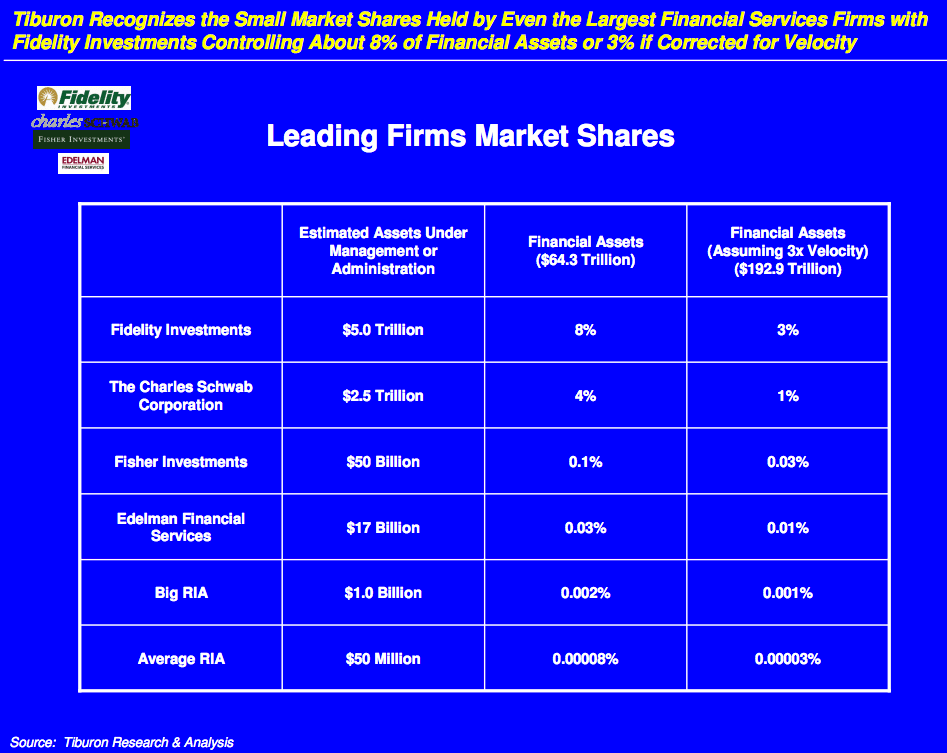

Perhaps the most interesting insight is that we truly have one of the most dynamic and fragmented industries in America. No one – no one – has anything even approaching true scale. Take a look:

That last column – with the 3x velocity – illustrates the thing I mention above about assets being triple-counted.

When you think about the wealth industry that way, you really get a sense of how much opportunity there is for everyone in the game who has the ability to grow and thrive. Many financial advisors will be wiped out of the business in the coming years as they fail to keep up with technology and marketing challenges. Those who get over the hump will be the consolidators and the beneficiaries.

I just want to thank Tiburon for having me there again this year. It was one of the best industry events I’ve ever attended. Where else do you get the opportunity to hear from Morningstar’s Don Phillips, Ric Edelman, Tom Dorsey, Shirl Penney and Jack Bogle (!) live and in person, in a single day? Sick event.

[…] Josh Brown: The State of Wealth Management in 2017 […]

[…] Josh Brown: The State of Wealth Management in 2017 […]

[…] The State of Wealth Management in 2017 […]

[…] got to meet Jack on stage at the Battery Park Ritz-Carlton in the spring of 2017 when he came to give the keynote address at Chip Roame’s Tiburon CEO […]

… [Trackback]

[…] Info on that Topic: thereformedbroker.com/2017/04/05/the-state-of-wealth-management-in-2017/ […]

… [Trackback]

[…] Find More to that Topic: thereformedbroker.com/2017/04/05/the-state-of-wealth-management-in-2017/ […]

… [Trackback]

[…] There you can find 51824 more Information on that Topic: thereformedbroker.com/2017/04/05/the-state-of-wealth-management-in-2017/ […]

… [Trackback]

[…] Here you will find 55404 additional Info to that Topic: thereformedbroker.com/2017/04/05/the-state-of-wealth-management-in-2017/ […]

… [Trackback]

[…] Here you can find 98495 more Information to that Topic: thereformedbroker.com/2017/04/05/the-state-of-wealth-management-in-2017/ […]

… [Trackback]

[…] Find More to that Topic: thereformedbroker.com/2017/04/05/the-state-of-wealth-management-in-2017/ […]

… [Trackback]

[…] Find More on that Topic: thereformedbroker.com/2017/04/05/the-state-of-wealth-management-in-2017/ […]