The image above is of the street-facing windows and facade at the New York Yacht Club, poured and molded concrete in the shape of a ship’s stern. It’s one of the many landmarks on 44th Street, a few doors down from my office, and the site of the DoubleLine Lunch with Jeffrey Gundlach for the third year running.

I took a bunch of notes from the lunch and have assembled them in a logical order below, just as I’ve done for you the past two years (see 2011 here and 2012 here for reference).

Without further ado, here’s what I took away from the event:

***

First off, no matter how many times you’re in this room, you never get over how incredible it is. You’re surrounded by carved wood and centuries-old ships’ prows, adornments and other artifacts of the city’s seafaring distant past. It’s truly magnificent, if you can ever find a reason to get in there I suggest you check it out.

Jeff and I chatted a bit before he took the podium, I think he’s sick of looking up and seeing me on the firm’s TV screens. He doesn’t watch much financial television and, as a contrarian, really only uses it to find out what the consensus is all hopped up about at any given time.

I should mention that he’s the most consistently well-dressed money manager I know (and I go to an awful lot of conferences). I’m not sure why this might be important to you, but the congruency of a Bond King looking the part is important to me. I think I might start doing some pocket squares and stuff myself later this year…

Anyway.

Jeff’s presentation was entitled “Why Own Any Bonds At All” and it speaks to the recent zeitgeist surrounding the concept that the Fed has made it so that stocks are the only game in town and bonds are useless.

Gundlach respectfully disagrees. The purpose of his talk today was to show that, while the bond market is not exactly the free lunch it became in 2009-2010, there’s still plenty of fruit hanging from the tree if you know which orchards to look in. Jeff demonstrates why the Fed’s policies literally cannot change any time soon and how investors can use this as an opportunity.

Most of the below is me paraphrasing, but where you see something in quote’s it’s Jeffrey. Let’s begin…

We’ve heard this question before

For starters, this isn’t the first time the investor class has questioned whether they should own bonds at all. The last era during which this was an open question was 1997 – but for different reasons.

In 1997, bonds and stocks were positively correlated. When bonds went down, stocks did too. But when bonds went up, stocks went up even more. And so why bother with the bonds at all, went the thinking. US bond yields in 1997 were 6%, so you can just imagine how much higher the expectations were for stock returns then!

Jeff loves the Japanese comparison and uses it here – in 1989, the year the Nikkei (Japan’s stocks) peaked, Japanese government bonds were also yielding 6% – obviously Japanese bonds were the (much) better buy then versus stocks.

No bond bubble

America does not “over-own” bonds.”Raise your hand if you own a Treasury mutual fund for yourself or your clients…” No hands go up in the entire room (maybe out of embarrassment or because the salads were served).

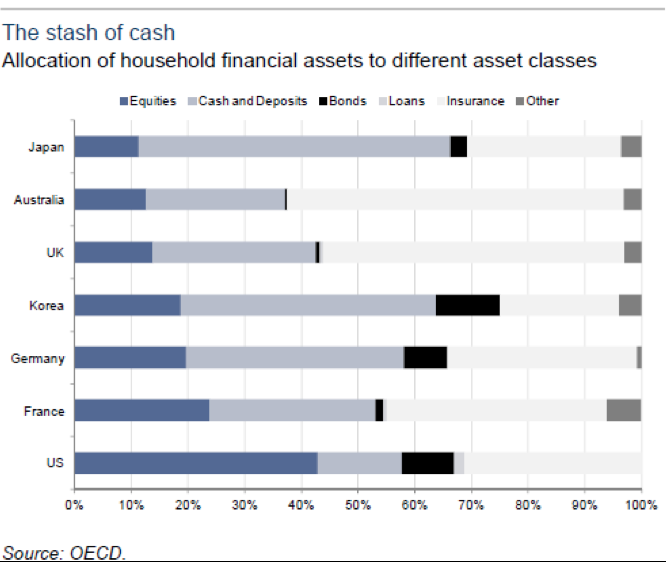

If anything, relative to the rest of the developed world American households over-own stocks and are perhaps equal to the rest of the world in terms of bond holdings. The below chart is Net Worth in Financial Assets by Country, the black portion of the bar is bond ownership and the dark blue is equities:

There’s no bubble in bonds. Gundlach is amused by those claiming that the bond market is on the verge of some kind of imminent collapse. “They’re dead wrong.”

Why do American households own so much stock compared to other countries? Gundlach believes that the massive wealth polarization in our country versus other countries plays a role – so much of our wealth is concentrated amongst the very rich, who tend to own stocks.

QE and ZIRP are a New Way of Life

Gundlach laughs whenever the Fed Minutes come out or a governor speaks and people search for clues about the end of monetary stimulus or accomodative low rates. Not happening this year or next.

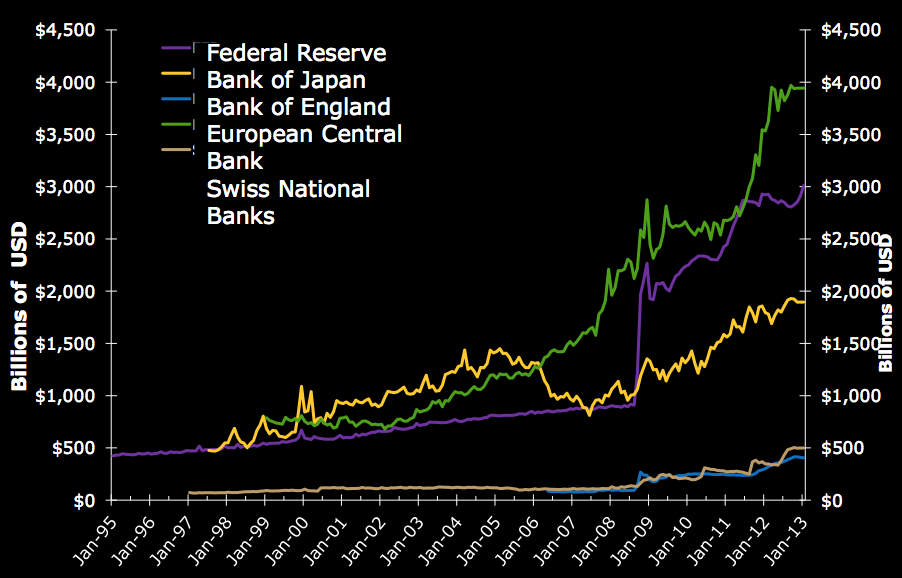

Publicly made comments and dissent is just talk. The entire world is embarking on what Gundlach refers to as “the circular financing scheme”. The below slide shows how just about every single country in the world is currently running a trade deficit at the same time – “How is this even possible?” The answer is the circular scheme being perpetuated around the world (Bank of Japan, Bank of England, the ECB and the Fed are all expanding their balance sheets at the rate of 3.5% of GDP per annum). “This is what Krugman says is the answer to five millennias-worth of human struggle. Maybe he’s right but it seems a little too easy.”

See below, that’s central bank balance sheets, January 1995 through January 2013:

He mentions that Ben Bernanke has publicly stated he sees “no observable negative consequences” from this activity and that Janet Yellen is even more dovish, has made comments about allowing this to run through 2025 if need be.

The trade deficit is what’s supporting the US economy and the Fed’s purchasing is the only thing keeping interest expense low enough to allow the government to continue running a trillion dollar deficit. We know that the only glue holding this altogether right now is that the interest we’re paying on government debt is manageable – no one is going to pull that chair out from under us on purpose.

Combine this with the state of the labor market and you know the Fed is going nowhere. When they say that they’re pondering the end of QE, Jeff says “Of course they’re pondering it, gee I would hope so!” but this does not mean they are considering an exit right now. He believes the exit will look like a run-off of the existing treasury and mortgage bond portfolio as the bonds the Fed holds mature – but not an outright sale of the portfolio. “There’s a better chance Bernanke buys every Treasury bond in existence before he ever sells a single one”

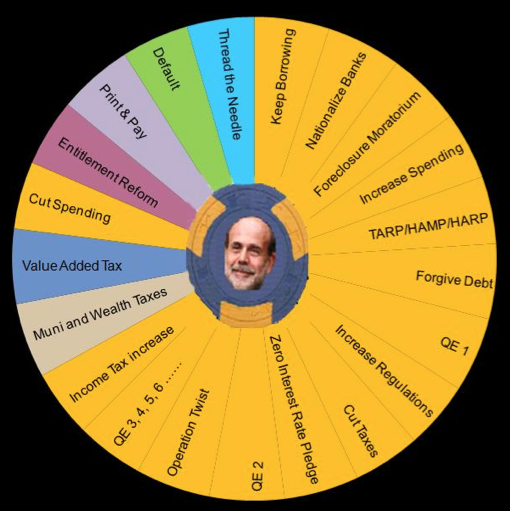

Gundlach breaks out the fan favorite slide – Bernanke’s Wheel of Fortune:

All of the options in yellow have already been attempted. Gundlach says that of the remaining, default is not going to happen and the long-rumored “print and pay” that the policy bears fret about is “not timely.” He says print and pay may happen someday but we’re simply not there yet, too early. He mentions that removing the tax benefit from muni bond interest for ultra-high net worth households is likely which keeps him cautious about the muni market in general. Entitlement reform would be nice – but when you poll Americans you realize that this has the support of only 10% of the population (about the same percentage as believes in Bigfoot) and so it won’t happen – you could never get elected.

How to play continuation of the Fed’s policies

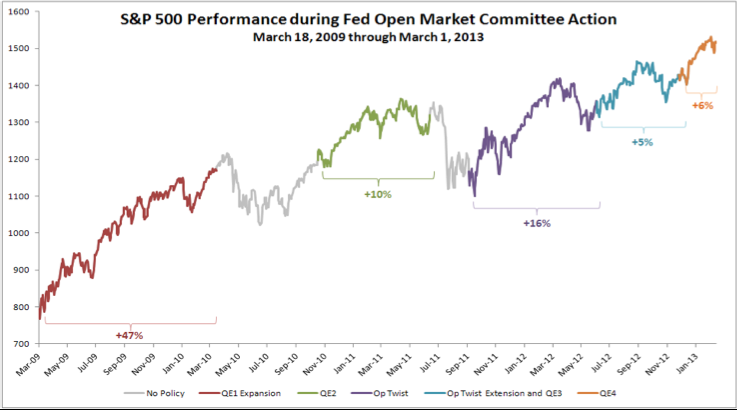

So if we know that QE and ZIRP are here to stay for the time being, is the answer stocks or bonds? Jeffrey says stocks maybe but bonds definitely. He notes that quantitative easing has had no effect on the commodities complex (CRB index) but the “transfer mechanism has weirdly benefited stocks.”

The below is the cumulative effect of QE on the stock market:

But it is the bond market that has the real “put” he says, and not the stock market. Quantitative easing “goes right through the heart of the bond market.” Which is one of the reasons why Gundlach is back to buying longer-dated Treasurys with some of his portfolio.

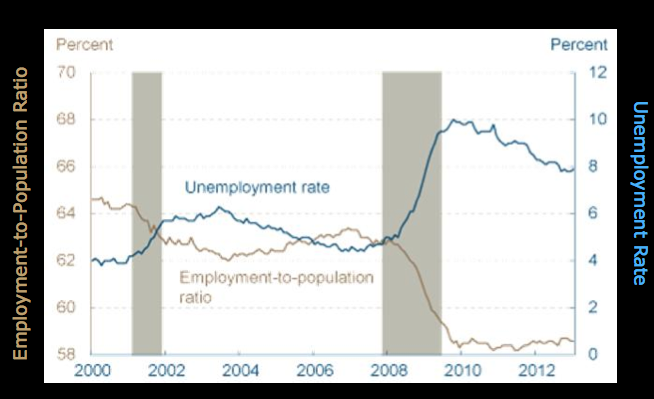

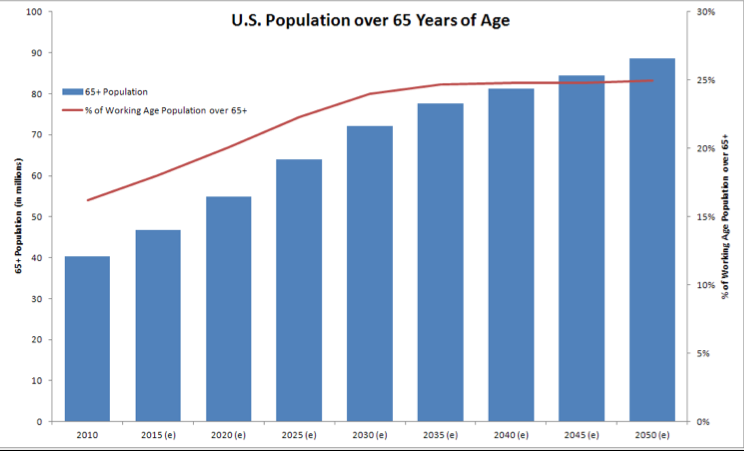

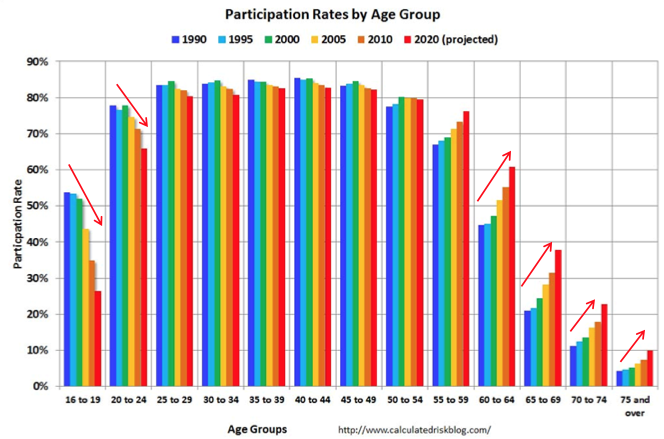

Speaking of the labor market…

…it still sucks no matter what the headlines say. The participation rate is alarming. The old people won’t retire (they can’t) and the one thing you can’t fake – employment-to-population – has not improved. On top of which, right now we’ve got 40 million Americans age 65 and older. In 15 years we’ll have 70 million age 65 and older! This large, aging population, he argues, is a bullish factor (or at least a supportive one) for the bond market.

Three key charts illustrating the age and participation problems in the US labor force (click to embiggen):

The bottom line is that this jobs picture is not conducive for any kind of ZIRP or QE exit anytime soon, hence continued support for the bond market.

What to do in the bond market

So if you agree that bonds are the bigger beneficiary of ZIRP-forever, what can you with a bond portfolio? Some key points Gundlach makes:

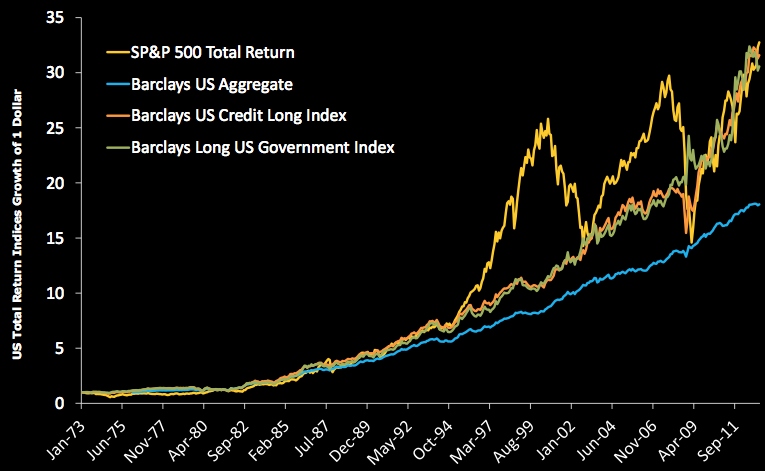

Investors have been spoiled by bond indexing – because it has worked. Here’s the total return of the long bond vs the S&P etc over the last 40 years:

But those days are over.

If you look at the major bond indexes (like the Barclays Aggregate) they are overloaded with Treasurys which have the lowest yields. Average durations for the Aggregate index have remained around 5 or so – interest rate risk hasn’t gone up, in other words – but yields-to-maturity have collapsed to around 2%. There’s not much in the traditional index left to scrape up, in essence. This is the anti-passive, anti-bond ETF argument.

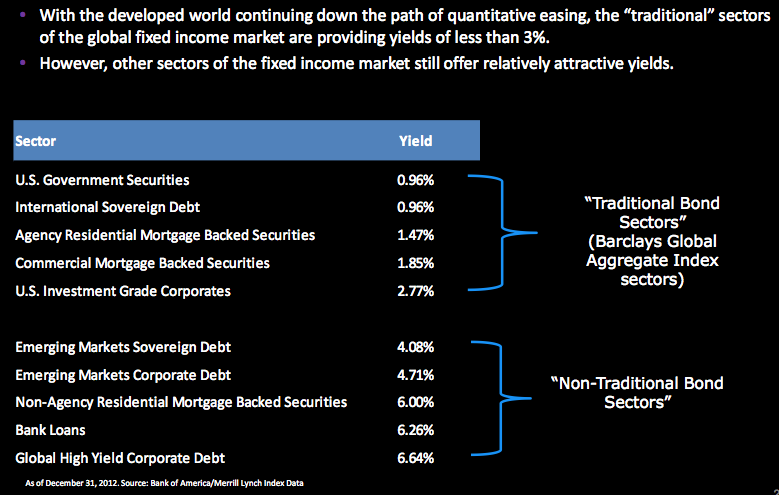

So being selective will work better than just going with the index going forward. In the below slide, perhaps the most important, Jeff shows how the “non-traditional” sectors of the market differ greatly from the more mainstream, developed ones in terms of yield. These outside-the-index areas are where there is still fruit left on the trees:

Jeff mentions that the single best area of investment grade fixed income right now is dollar-denominated emerging market corporate bonds. He still favors non-agency MBS but these credits will continue to be bid higher and then disappear, un-replaced.

He believes that when private financing (non-Fannie, non-Freddie) does return to the mortgage markets, it will create tremendous opportunities for bond investors.

He mentions bank loans being an interesting area for opportunity as well. The caveat is that the higher yield stuff should be paired with something like a Treasury for risk management purposes (barbell strategy?). I should note that DoubleLine is launching a floating rate bank loan fund shortly.

He also likes high yield corporate as he believes default rates should stay low given balance sheet strength – even if profit margins mean-revert lower. In this regard, Jeffrey agrees with John Hussman that 70%+ is probably the peak for the cycle and unsustainable. This shouldn’t hurt corporate bonds, however, the impact on stocks is debatable.

A word on Japan

Jeffrey mentions that Japan is important to watch for several reasons. He calls it the “Pace car for stock market peaks, weird policy responses and currency debasement.” He sees it as a template for how the rest of the world will deal with deflation and demographic issues. When queried about the Japanese stock rally, he mentions that he went bullish on Japanese equities last November and people told him him he was an idiot. A big time “Republican center of influence guy” emailed him “Don’t you know that Japan is where capital goes to die?”

Looking forward, Jeff says it’s hard to imagine that the 50% rally in the Japanese market just stops on a dime and reverses itself to the downside.

Besides, he thinks that over time – not tomorrow but one day – the only way the Japanese can ever deal with their debt level is more debasement so a Yen at 200 over the USD is conceivable.

Japan, most importantly, illustrates to investors that bond yields can stay low for as long as they want to.

Odds and Ends

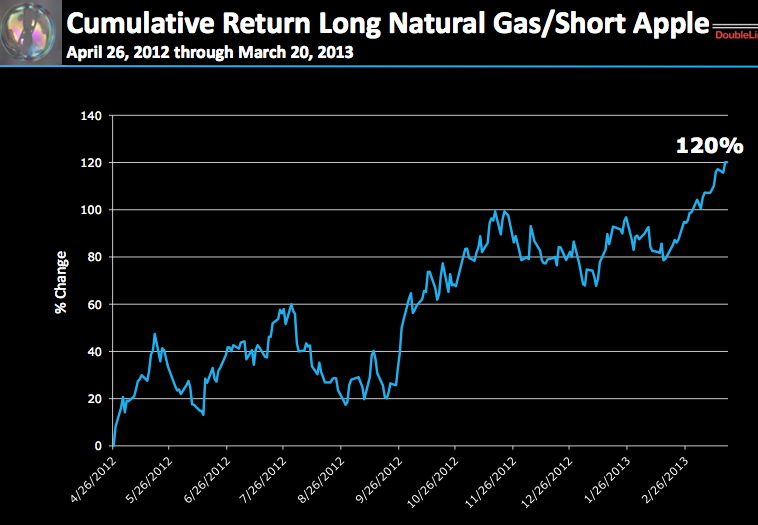

When we got to the Q&A the first thing people wanted to hear was a comment on Jeff’s now legendary pairs trade from last summer. I was in the room when he mentioned he liked “Short Apple versus 100X long Natural Gas futures” – he was demonstrating the ridiculousness of the consensus at the time, which was that Apple could never go down and natural gas was headed to zero. Obviously, he nailed it and the opposite happened. Nat gas almost doubled from there and Apple was just about cut in half from its high. World-renowned for his modesty, Jeff mentions that the trade was actually even better than we all think it was because “it was never down even or a single day.” My table – all wealth management guys with big egos (i’d presume) – got a kick out of that.

Here’s the chart of his pairs trade’s performance:

When asked for a new miracle trade, the manager demurred a bit but then mentioned that he would short Chipotle – which promptly knocked the stock down 8 points once the media reported my tweet from the event, what a world we live in! Jeff’s point – much the same as David Einhorn’s from last fall – is that the multiple is quite high for what is essentially an “oxymoron” product, the “gourmet burrito”. He’ll be at the Ira Sohn Value Investing Conference in May (as will I) and so maybe we’ll get more detail on this idea then.

He was asked about preferred stock as a way to cope with the low rate environment and admitted he had no opinion (first time I’ve ever heard him punt on a question). Like Socrates, he admits to knowing what he doesn’t know.

Nobody asked Jeffrey about gold for the first time – he was very surprised by this so he brought it up himself. He thinks that as fear of systemic collapse rolls away in the short term, gold should continue to slide. He mentioned $1200 an ounce as a possible target but didn’t seem emphatic one way or the other.

There was a question about assets under management and getting too big to be an effective total return investor. DoubleLine currently manages $56 billion – $40 billion of which is in Jeff’s Total Return flagship (full disclosure – we own this fund in client accounts at our shop and have since inception). Jeff thinks anything over $100 billion would hurt the strategy and $75 billion may even be too much. He takes a dig at “trillion dollar bond funds” in that they’re forced to use derivatives and swaps and as such they have counterparty risk, the single worst thing in Gundlach’s eyes (he refers to it as “rewardless risk”). DoubleLine is actively rolling out funds in new categories (there’s even a hedge fund in the works) and may soft-close Total Return at some point soon should the inflows continue at the current pace.

I asked the last question of the day. At the 2011 lunch he mentioned that high net worth investors ought to keep a portion of their wealth outside of banks and the traditional financial system so I brought up Bitcoin in that context. He said he really prefers to own things like fine art (he is an avid collector – I was awed by I saw in the lobby and hallways of DoubleLine’s L.A. office when I visited this past fall) as well as precious gemstones. “People scoff when I mention gems as an investment – then I tell them that I possess some of the most flawless, perfectly formed emeralds in the world and they beg to see them.” Jeffrey thinks Bitcoin is a “mega mania” and a gimmick, not a currency. “I’d rather own diamonds and Picassos.”

Spoken like a true boss.

***

Anyway, hope this was helpful for you. Taking these kinds of notes and then putting them together for you helps me learn and absorb a great deal as well – so thanks for reading!

Jeffrey Gundlach’s complete slides are PDF embedded in the link below if you’re left wanting more…

Why Own Bonds – DoubleLine April 2013

[…] from the DoubleLine Lunch with Jeffrey Gundlach, Spring 2013 by Josh Brown. The full slides […]

… [Trackback]

[…] Read More on on that Topic: thereformedbroker.com/2013/04/12/notes-from-the-doubleline-lunch-with-jeffrey-gundlach-spring-2013/ […]

… [Trackback]

[…] Find More to that Topic: thereformedbroker.com/2013/04/12/notes-from-the-doubleline-lunch-with-jeffrey-gundlach-spring-2013/ […]

… [Trackback]

[…] Read More Info here on that Topic: thereformedbroker.com/2013/04/12/notes-from-the-doubleline-lunch-with-jeffrey-gundlach-spring-2013/ […]

… [Trackback]

[…] Find More to that Topic: thereformedbroker.com/2013/04/12/notes-from-the-doubleline-lunch-with-jeffrey-gundlach-spring-2013/ […]

… [Trackback]

[…] Information on that Topic: thereformedbroker.com/2013/04/12/notes-from-the-doubleline-lunch-with-jeffrey-gundlach-spring-2013/ […]

… [Trackback]

[…] Read More to that Topic: thereformedbroker.com/2013/04/12/notes-from-the-doubleline-lunch-with-jeffrey-gundlach-spring-2013/ […]

… [Trackback]

[…] Find More to that Topic: thereformedbroker.com/2013/04/12/notes-from-the-doubleline-lunch-with-jeffrey-gundlach-spring-2013/ […]

… [Trackback]

[…] Read More Info here to that Topic: thereformedbroker.com/2013/04/12/notes-from-the-doubleline-lunch-with-jeffrey-gundlach-spring-2013/ […]

… [Trackback]

[…] Info on that Topic: thereformedbroker.com/2013/04/12/notes-from-the-doubleline-lunch-with-jeffrey-gundlach-spring-2013/ […]

… [Trackback]

[…] Read More Information here on that Topic: thereformedbroker.com/2013/04/12/notes-from-the-doubleline-lunch-with-jeffrey-gundlach-spring-2013/ […]

… [Trackback]

[…] Here you will find 69435 additional Information on that Topic: thereformedbroker.com/2013/04/12/notes-from-the-doubleline-lunch-with-jeffrey-gundlach-spring-2013/ […]

find cheap cialis online

USA delivery

buy cialis online generic

USA delivery