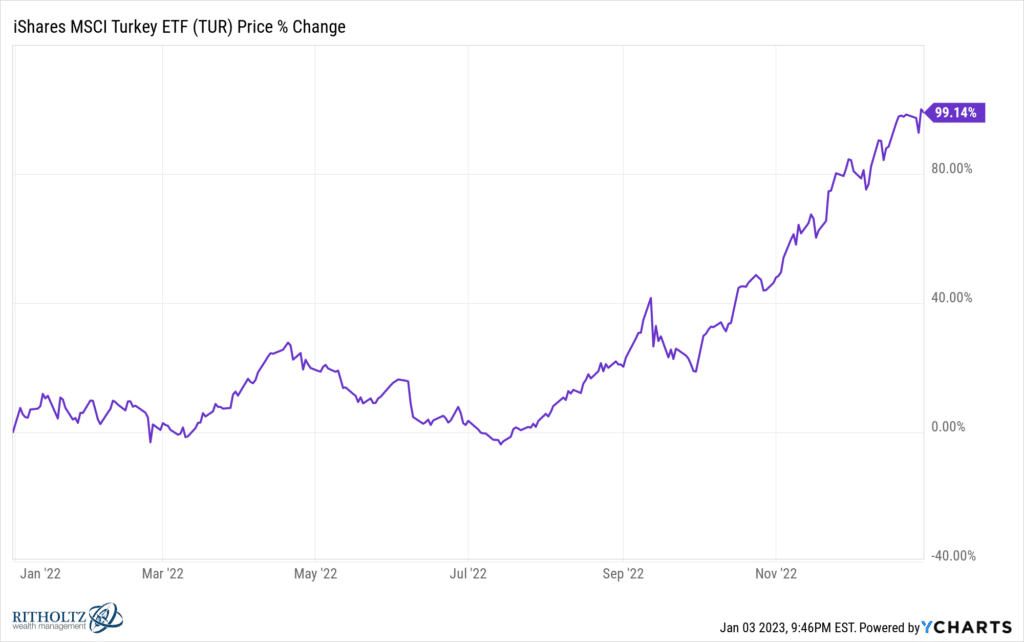

If you’re a financial advisor or a fund manager and you weren’t down 20% last year, you won, basically. The S&P fell into a 20% bear market while the Nasdaq crashed almost 40%. Bonds were down double digits as an asset class. International stocks, while outperforming the US and not down as much, were still down a lot. Except for Turkey, which inexplicably doubled last year – here’s the TUR ETF, up 99% in 2022.

I would Google it to find out why, but I don’t feel like it. Maybe there’s no reason at all.

The Dow Jones Industrial Average was down less than 10% thanks to larger weightings toward energy stocks, but no one owns the Dow Jones in the way people own the S&P 500. Proof? The SPY ETF has $356 billion in it and the index has hundreds of giant ETFs and mutual funds tracking it. The DIA – Dow Jones version of SPY – has less than a tenth of the AUM ($29 billion) despite having existed for just as long.

Anyway, the silver lining of this bear market for us is that we got to show off the capabilities of all the custom indexing and daily, algorithmic tax loss harvesting we’ve been doing. Plus the benefit of running a tactical strategy in tax-deferred accounts alongside our longer-term positions. Plus we raised a ton of money from new clients who had gone into this mess without a great advisor or a working financial plan or any clue about how to mitigate risk in a portfolio. We don’t root for bear markets, of course, but we make sure they pay off on the way out. And it’s nice to have positive, productive actions to take in a blood-red tape. This is the seventh bear market of my career already, we know how to get through these things and what to do while we’re in them.

So, all things considered, this hasn’t been fun but it will all work out in the end. It always does, provided nobody does anything stupid or irreversible on our watch.

I was thinking about the hierarchy of people who have been truly affected by the events (and price action) of 2022 and I guess I would put employees of tech startups at the top of my list.

The rank and file startup worker has probably received a lot of their compensation (and day to day motivation) in the form of shares and stock options over the last few years. In some cases they’ve even paid the taxes up front so as not to have to worry about the gains later. For this cohort, now staring down piles of worthless or near-worthless shares in thousands of companies, it’s been a horrible experience. The layoffs won’t stop until the funding markets for venture equity become more forgiving, and they won’t for the foreseeable future. Capital has gone from cheap (or even free) to very expensive. There is no appetite for this sort of risk right now. When the greatest company on earth is on the verge of losing half its market cap (as Apple seems to be headed for, at the moment), how on earth could there be demand for the shares of a pre-revenue white board idea masquerading as a business?

Remember the days of “Oh you have a slide deck and an ex-Google employee, here’s $80 million in seed capital”? Well, these days it’s the opposite. No seeds. Get away from my window.

The young people who’ve flocked to these sorts of companies are going to feel this uncertainty the most. The layoffs have only just begun. Next are the wind-downs. This is when a company is so hopelessly unprofitable and unlikely to be funded that the only responsible option is to just stop. Take what’s left out of the bank, return it to the investors and leave the keys. It takes years for this process to cleanse the ecosystem of excess and set up the next generation. The people with staying power to hang on until then come from family money or have already been the beneficiaries of an exit or two from a prior cycle. You know who they are. They have seven figures in the bank and a willingness to spend their time polluting Twitter with half-remembered Clay Christensen aphorisms and threads about the hard thing about hard things. They’ll do podcasts and pontificate about Ukraine until the Federal Reserve relents and the money spigot turns on again. Mortimer, we’re back!

But the workers are kind of f***ed for the moment. They probably didn’t cash anything out or take any risk off the table like the founders have. They had to put it all on black and keep it there while awaiting news on the next funding round. That news isn’t coming. And there’s nowhere to go right now, even in an economy with one of the tightest labor markets ever. The largest companies in tech, media and telecom are all freezing hiring or laying off staff, so swimming toward a bigger ship probably won’t help much in the short term.

After startup workers, I would probably most feel bad for the mortgage brokers and the realtors. They were riding one of the most exciting bubbles of activity and action the housing market has ever seen. A twenty year up-cycle all packed into a span of just twenty months. My favorite local realtor started filming himself trying on Gucci belts in the mirror. And posting it.

The years 2020 and 2021 might have been two of the greatest years of all time for the housing sector. Home prices rose 40%, eventually topping out in June of 2022. It’s been straight down ever since. Prices have to fall further to sync up with prevailing rents. Existing home sales have already begun fallen through the floor. Sellers have nowhere to go and no desire to re-borrow at 6.5%. Buyers can’t rationalize the massive increase in borrowing costs. Contractors can still sell newly built homes because inventories are so tight, but the profits from selling a new house relative to the cost of building it are nothing special. The market has been put into a deep freeze. Refinancings are done. Demand for mortgages is falling off a cliff. Transactions are vanishing. It’ll get worse this spring. The comps relative to last spring will be laughably bad.

Here’s Brian Wesbury and Robert Stein at FirstTrust writing about the housing market:

The real effect of the change in interest rates is evident in the existing home market. Sales hit a 6.65 million annual rate in January 2021, the fastest pace since 2006. But, by November 2022, sales were down to a 4.09 million annual rate, a drop of 38.5% so far. Meanwhile a decline in pending home sales in November (contracts on existing homes) signals another drop in existing home sales in December.

Existing home buyers have two major problems: first, much higher mortgage rates, which means substantially higher monthly payments. Assuming a 20% down payment, the rise in mortgage rates and home prices since December 2021 amounts to a 52% increase in monthly payments on a new 30-year mortgage for the median existing home.

You can get the rest of their housing commentary here.

So if you know a startup employee, be nice and offer to circulate their resume around. And if you know a residential realtor who wasn’t prepared for the 2021 environment to change so abruptly, give them a hug – they could use it right about now. And if you know a mortgage broker, well, maybe just cross to the other side of the street when you see them coming. No eye contact. Just let ’em pass and say, in low and reverent tones, “There but for the grace of God, go I.”

It’s a tough environment for most people right now. Try to remember that it could always be worse.

***

Happy New Year. If you’re unsure of your current financial plan or portfolio or you’re looking for a second opinion or a professional consultation, we’ve got a dozen Certified Financial Planners standing by to chat at your convenience. Don’t be shy, we do this all day for thousands of families across the country. Send us a note here: