One of the things that’s kept people out of stocks (or more lightly allocated) has been the concern over “negative earnings growth” or the idea that the EPS and sales growth of 2018 was petering out.

When you hear stuff like this, it’s important to remember that we had a one-time tax cut benefit in all of the numbers that allowed S&P 500 constituents to report lower effective tax rates and an “instant” profitability spurt – and that this sort of thing was never going to be repeated in 2019. The corporate tax cut was made official in December 2017, and the S&P 500 had already spent the entire year anticipating it with a huge run-up in share prices. Then, in 2018, it took effect, and we had two double-digit selloffs into the news (one in February and then another that stretched from September through Christmas Eve – this one falling all the way down 20% to produce the requisite “bear market” headlines).

It’s not ironic that earnings and sales growth were incredible throughout 2018 while the index closed the year down 5%. Stocks are anticipatory; prices reflect people’s opinions about the future, not the present.

Let’s turn our attention to this year and beyond…

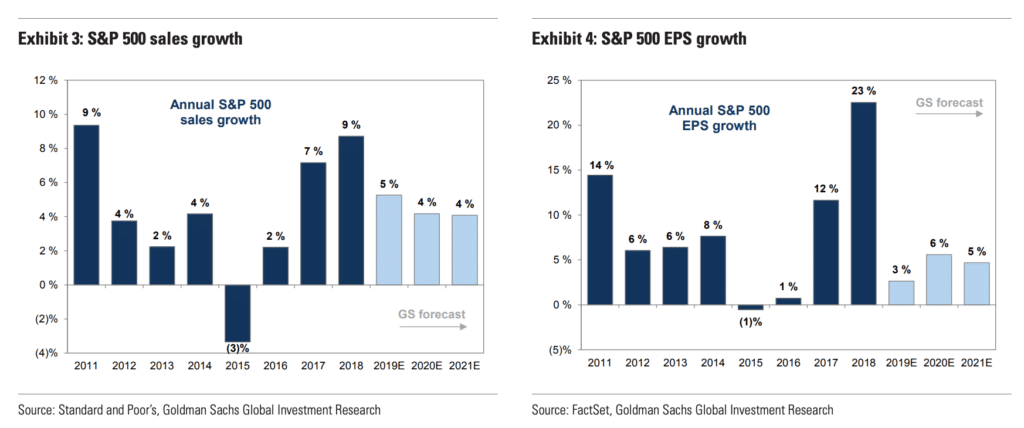

Goldman Sachs strategist David Kostin is out with a note looking at the outlook, and what he sees are continued gains in earnings and revenues and economic activity, but it’s plain to see that 2018 represented a statistical growth rate peak. See the charts below, which show actual plus expectations going forward:

Josh here – so you’re not going to get a return to 9% revenue growth or 23% earnings per share growth this year or next, because you’re not getting another massive, one-time tax cut (I know one was being promised a week before the midterms, but that’s just because liars will lie, nobody actually priced that happening into their estimates). Anyway, the important thing was to understand that, yes, of course the comps were going to generate a deceleration. Harder to imagine, however, was whether or not investors would “see through the valley” and react well to these declines in growth rates. They did react well. Who knew?

The message here is that stocks and the economy can continue to grow on past the peak, even if it is more reasonable to expect them to do so slowly. Here’s Kostin’s outlook, which is reasonable and should be supportive of at least current valuations, absent any sort of exogenous event:

We expect S&P 500 EPS will grow by 3% in 2019 and by 6% in 2020. Our top-down EPS estimates are generally in line with bottom-up consensus estimates in 2019 ($167 vs. $166), but well below consensus estimates in 2020 ($177 vs. $184). We forecast sales growth of +5% and +4% in 2019 and 2020, roughly in line with nominal US GDP growth and slightly below consensus estimates. We forecast margins will fall by 39 bp in 2019 but rebound by 14 bp in 2020 as economic growth improves.

We lower our 2019 EPS estimate by $6 and growth by 3 pp, given weakness in economic activity and the margin outlook. Since January, we have noted that 2019 EPS growth would likely equal between 3% and 6%, depending on the trajectory of key macro variables. Halfway through the year, economic growth has been below-trend, oil prices have been range-bound, and tariff uncertainty has not abated. We therefore expect that 2019 EPS growth will equal 3%, the low end of the range. Most of the change in our earnings estimate is driven by weaker-than-expected economic activity, oil prices, and margins, particularly within semiconductors.

So, technically, yes, we are seeing a “deceleration.” If that’s kept people out of a 20% S&P 500 rally this year, however, it’s not a good look. It was easy to have foreseen that the one-time benefit of tax reform was not going to repeat – but that this did not spell doom for the stock market or the economy.

The next test will be whether or not share prices handle things well as consensus forecasts for full-year 2019 come down at firms up and down The Street. The good news is that this happens almost every year – the most bullish outlooks are always published in December and, as Kostin remarks, it is after Q2 reports are out that analysts begin to chop down the full-year estimates. Hang tough.

Source:

S&P 500: Lowering earnings, raising price targets

Goldman Sachs – July 29th, 2019

… [Trackback]

[…] Info to that Topic: thereformedbroker.com/2019/07/30/deceleration/ […]

… [Trackback]

[…] Info to that Topic: thereformedbroker.com/2019/07/30/deceleration/ […]

… [Trackback]

[…] There you can find 48910 additional Information on that Topic: thereformedbroker.com/2019/07/30/deceleration/ […]

… [Trackback]

[…] Read More Info here on that Topic: thereformedbroker.com/2019/07/30/deceleration/ […]

… [Trackback]

[…] Find More to that Topic: thereformedbroker.com/2019/07/30/deceleration/ […]