Did you liquidate your 401(k) 53 days ago when the market breakdown of January shook investor confidence and temporarily drove the punditocracy to madness?

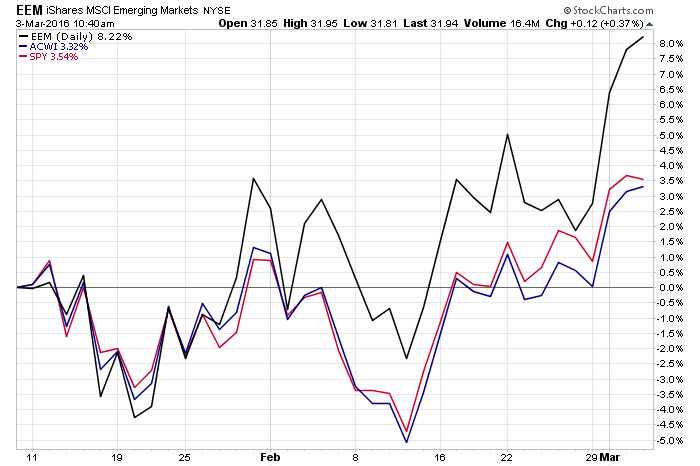

If so, here is what’s gone on since across stock markets around the world – Emerging Markets (EEM), MSCI All Country World (ACWI) and the S&P 500 (SPY):

Had you sold off your 401(k) account in response to volatility, which was a suggestion being seriously made in the financial media at the time, you’d be faced with new questions today:

Now what?

Do you buy back in and get fully invested substantially higher in so short a period of time?

Do you dismiss the recent market recovery as a “headfake” and hold out for lower prices?

Do you make a solemn vow to stop listening to your emotions or the noisemakers who have no business giving you advice about your retirement assets?

What do you do now? I don’t have the answer because I don’t know where the market is headed next. Nor does anyone else, which makes an “unforced error” like this so tragic – it puts you in a position to have to make guesses that you couldn’t possibly be equipped to get right on a regular basis.

Investing is simple, but it’s not easy, which is why smart investors do much less with their 401(k) portfolios than most investors.

Not only did liquidating a retirement account on January 10th put you into a position of having to make a decision like this, it also robbed you of the twin buying opportunities you can see in the chart above, both of which happened in the middle of the months of Jan and Feb – right about the time your payroll deduction would have gone into the account. It is the compounding effect of regular dollar cost averaging that generates massive retirement account balances over years and decades – not timing the market right.

I talked about the sacred nature of 401(k) accounts on January 10th and why investors should not be f***ing with their allocations in response to market volatility. I don’t give personalized investment advice here, but if you’re a regular reader of my site, I feel some responsibility to you. I don’t want you to fall prey to unforced errors and the attention-seeking manipulation of the market commentator class.

If you missed this the first time or haven’t internalized it yet, please let it sink in and pass it on to the young people in your life who are just getting started:

The Farce Awakens

One of the worst starts to a calendar year in stock market history. The S&P 500 plunges straight out of the gate and is now 11% off its record high set last year.

Volatility brings out the most counterproductive behavior in investors and, almost without fail, brings out the worst sort of advice. Farcical advice, the kind that would be laughed out of the room in the company of wealthy people or successful investors who’ve been around for a few cycles.

Some of the more disturbing nonsense I’ve seen over the last few days has concerned what people should be doing with their 401(k) accounts, of all things. Why day traders and aspiring hedge fund startups feel compelled to weigh in on how ordinary people ought to handle their defined contribution retirement plan accounts is beyond my understanding.

The gist of what I’m hearing, mostly from people who are utterly unequipped and unqualified, is that:

a) the market’s been falling and it seems like it will continue to fall because of ______

b) therefore, the responsible thing to do is to liquidate your 401(k) and sit in cash until it’s over

To which I would remark the following:

The average investor has no ability to put any kind of technical or quantitative data to work regularly – even if it was shown to be completely effective (which it hasn’t) – in order to time the market.

401(k) accounts are not about P&L, they’re an accumulation vehicle designed to allow the capital markets to do their job over time, which is translating the risks of the present into the returns of the future. Interfering with this process by flipping into and out of cash literally defeats the purpose.

If an investor manages to get one shift into cash right because they had a hunch or they happened to read the right blog post that day, this doesn’t mean they’ll be able make the shift back at an opportune time.

Even if they get out and back in once, can they do it twice? Thrice? Can they do this always?

More than likely, they cannot do this always. What is more likely (some would say guaranteed) is that an investor will get some shifts right and others wrong and the misses will negate much of the benefit of the hits. Or worse. Selling when volatility spikes and then buying when “the coast is clear” essentially guarantees the kind of “sell low, buy high” strategy that’s sure to result in massive underperformance of one’s own investments.

Many independent traders do not have access to employer-owned 401(k) plan accounts so it may not occur to them that there can be fees for moving funds around. There are freezes that prevent one’s ability to buy and sell and buy back again. It’s not that you can’t trade in a 401(k), it’s that you weren’t meant to and it is against the spirit of the thing.

Volatility is not risk, it is the source of future returns. Drawdowns should be embraced, not fled from. If anything, a better timing tool would be to up one’s allocation in times like these, or to skew one’s elections further toward equities to take advantage of a temporary decline. This is a passive way to exploit events that are beyond our control, and there is the added benefit that it actually works.

A working-age person between the ages of 20 and 65 could conceivably be looking at anywhere from three to seven decades during which they’ll need to live on their savings. They’re going to need stock market exposure to do this unless their financial plan involves hitting the Powerball or inventing The Facebook. The idea that side-stepping a bear market is of equal importance to the steady accumulation of risk assets is, in this context, a giant joke.

Being fully in cash warps your mind and does not allow you to think straight. It’s sure to result in emotional problems as well. Plus, it’s a money loser. I explained this during the last bout of nasty volatility when everyone was panicking to cash back in October 2011. There are people who “flipped to cash” then that have still not gotten back in. Believe me, we see their portfolios sent in to us every week.

The person telling you to liquidate your retirement investments is most likely uninformed about retirement investing in general, even if they are a good trader or have a great understanding of the macro situation or whatever. A well-meaning person can give bad advice just as easily as an attention-seeking charlatan can. Don’t judge the speaker, judge the actions they’re advocating.

If you’re a do-it-yourself investor, you probably don’t have the sophistication or the time to be running your money tactically. You might think you do, but it’s not a matter of being smart or “understanding the market.” It’s a matter of having the separation between your money, which represents your freedom and future happiness, and your emotions about these things. It is very hard to untie your own feelings from your money. This is why wealthy people pay a financial advisor to create this separation. Investment advice is about having good counsel, only a fool thinks it’s about picking a lineup of ETFs.

Historically, less than 15% of all ten-year periods offer losses to investors in the stock market. That’s not the best part. Over rolling twenty-year periods – starting in any month of any year over the last century – you’ve never lost money in stocks. Didn’t happen in the 20’s, 30’s, 40’s, 50’s, 60’s, 70’s, 80’s, 90’s or the 2000’s. Some twenty-year rolling periods have been better than others, but none have been outright losers. You’re welcome to go to cash, wagering that your savings years will break that streak, but it’s a pretty low-percentage bet.

If you cannot parse the difference between volatility and risk (which I define as the chance of a permanent capital loss), then at least accept the fact that risk is a given no matter what. But you have a choice: You can decide when to take the risk, today or in the future. Rational investors would prefer to take investment risk today, accumulating assets while coping with drawdowns and fluctuations in value. Only an insane person would choose to take their risk at the back end of their life – being short of money in old age when it is nearly impossible to earn more money.

You can risk the volatility today or the chance of being broke later, your choice, but you must choose. Sitting in cash may temporarily feel better because there is a sense of security that comes over us when the value of our account ceases to fluctuate. But you’re not safe, you’re merely gaining the stability of a unit of currency in exchange for the risk of losing future purchasing power.

Here’s Helen Keller: “Security is mostly superstition. It does not exist in nature, nor do the children of men as a whole experience it. Avoiding danger is no safer in the long run than outright exposure. The fearful are caught as often as the bold.”

Let me wrap this up: 401(k) accounts are sacred, but they are not magic. They require a thoughtful person making decisions and behaving logically in order to work. The 401(k) users who have persevered through the large drawdowns of 15 and 7 years ago, while continuing to plug away with fresh contributions, are doing better than ever. Vanguard and Fidelity have reported record balances and have noted specifically that it’s the people who have made the least allocation changes that now have the most to show for it. Act accordingly and ignore people who don’t know any better, even if they think they’re helping.

[…] A favorite post: Guarding Against Unforced Errors […]

[…] a favorite post: guarding against unforced errors […]

[…] A favorite post: Guarding Against Unforced Errors […]

[…] A favorite post: Guarding Against Unforced Errors […]

… [Trackback]

[…] Info to that Topic: thereformedbroker.com/2016/03/03/guarding-against-unforced-errors/ […]

… [Trackback]

[…] Read More Information here on that Topic: thereformedbroker.com/2016/03/03/guarding-against-unforced-errors/ […]

… [Trackback]

[…] Read More Information here to that Topic: thereformedbroker.com/2016/03/03/guarding-against-unforced-errors/ […]

… [Trackback]

[…] Information to that Topic: thereformedbroker.com/2016/03/03/guarding-against-unforced-errors/ […]

… [Trackback]

[…] Read More on that Topic: thereformedbroker.com/2016/03/03/guarding-against-unforced-errors/ […]

… [Trackback]

[…] Read More Information here to that Topic: thereformedbroker.com/2016/03/03/guarding-against-unforced-errors/ […]

… [Trackback]

[…] There you will find 25547 additional Information to that Topic: thereformedbroker.com/2016/03/03/guarding-against-unforced-errors/ […]

… [Trackback]

[…] There you will find 102 additional Information on that Topic: thereformedbroker.com/2016/03/03/guarding-against-unforced-errors/ […]

… [Trackback]

[…] Read More Info here on that Topic: thereformedbroker.com/2016/03/03/guarding-against-unforced-errors/ […]

… [Trackback]

[…] Find More here to that Topic: thereformedbroker.com/2016/03/03/guarding-against-unforced-errors/ […]

… [Trackback]

[…] Info on that Topic: thereformedbroker.com/2016/03/03/guarding-against-unforced-errors/ […]