My fave thing about the FinTech space is the fact that amazing tools can literally sprout up from anywhere. I get sent stuff all the time to take a look at. Every once in awhile, something comes across my path that’s so awesome I just have to share it with you guys.

Today, I’m showing you a new resource, posted completely for free on the web, called PortfolioCharts.com. Created by Tyler, an engineer who’s taken some time away from his industry, PortfolioCharts offers a simple and intuitive way to backtest asset allocation strategies and truly gauge what the investor’s experience might have been like over various holding periods.

I spoke to Tyler this week by phone to get a little bit of background on why he built the tool and see what he intends to do with it. The answer to the first question is that he was sick of the 2-dimensional “average returns” calculators that proliferate across the web. Portfolio management is a hobby of his, but he was very unsatisfied with the available tools and thought he could build a more explanatory illustration for himself as he backtested different strategies.

The problem with the tools that currently exist is that they don’t offer the most important aspect of a historical returns test – what it may have felt like to be invested in various ways.

In other words, if I tell you that a roller coaster has an average speed of 40mph, am I really telling you anything about what the experience of the ride might be like? Not quite. I’m giving you an average but not showing you how the parts of the ride where you’re plunging at 90mph are only periodically offset by the sections of track where you’re coasting through at only 10mph in order to reach that mean speed.

The same is true when describing the experience of holding an asset class over time. If I tell you that the total US stock market returns 7% in real (inflation-adjusted) terms over 40 years, then I’m leaving out some really critical information (see How Averages Lie). I’m not demonstrating the fact that an average of 7% annualized returns only gets that way because there are up-30% years and down-30% years and everything in between all along the way. And I’m certainly not showing you what it would look like year-by-year by merely repeating that average return.

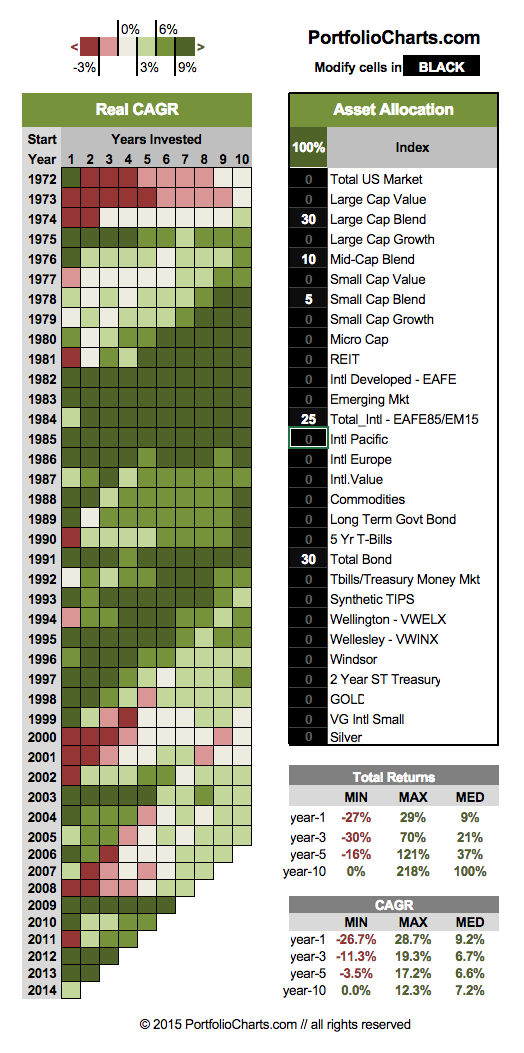

Enter Tyler’s interactive, visualized portfolio calculator. Here’s his “Pixel” view, with an asset allocation I’ve created:

As you can see, this is a portfolio that would have hypothetically produced a median cumulative annual growth rate of 7.2% over ten year periods going back to the data set’s starting point of 1972. As a reference point, if you can compound at 7.2% real, your portfolio doubles in size roughly every ten years. Not bad, huh?

But here’s the thing – that 7.2% didn’t come for free. You had to live with it through some tough times, which is exactly what Tyler is aiming to illustrate here.

Think about how holding this portfolio might have felt had you implemented it in the early 1970’s. An investor whose starting point was 1972 would be looking at average annual losses (losses!) for the first 8 years and a breakeven after 10 years. Futility doesn’t even begin to describe the emotional mindset of our fictitious holder after all that time. In other words, just because the median return for this portfolio over all one-year periods turned out to have been over 9% real, that doesn’t mean 9% real would have been a realistic bogey to hope for over all one-year periods.

Bear markets are hard, especially when a portfolio seemingly makes no progress for almost a decade. But raging bull markets can be just as difficult on the investor’s psyche – especially when there seem to fortunes being made by everyone else. I’ve seen firsthand how this could drive otherwise sane, conservative people completely crazy.

Consider what this asset allocation would have felt like had you implemented it at the beginning of 1999. We all know that ’99 was an amazing year for the Nasdaq Composite, which more than doubled as growth investors were becoming multi-millionaires seemingly overnight. Our test portfolio above would have only produced a return of 13.2% over the course of that year. A great return by any measure, but many investors watching the acrobatics of Sun Microsystems, Dell, Lucent and Cisco might have been suicidal as other people’s fortunes tripled and quadrupled while they themselves earned less than 15%.

Talking about the feel of a portfolio is important because the end investor is a human being – an emotional person who’s got to live with an asset allocation, not just cooly glance at the results, dispassionately from afar. No one is immune to the fear and greed that makes living with an asset allocation – even a good one – so difficult to do.

At Ritholtz Wealth Management, we have many portfolio construction and visualization tools at our disposal. Even by our professional standards, however, this is still a great one. Tyler’s also posted a “Hurricane” view that allows you to see the effect of annual contributions or withdrawals (great for retirement scenarios) as well as a “Funnel” view that shows you how long it takes to arrive at the point where long-term mean returns can be arrived at.

A few words on where PortfolioCharts.com gets its data from and how it makes its return assumptions:

Unless otherwise noted, all calculations assume a few things:

1) All returns are taken as a snapshot on December 31st

2) Returns include reinvested dividends

3) Portfolios are rebalanced annually

4) Returns quoted are REAL. This means that every year I subtract the inflation for that year (measured by CPI-U) to get the inflation-adjusted returns.

5) For calculators like the Hurricane that account for annual contributions or withdrawals, those cash flows are also adjusted for inflation each year. So if the initial contribution is $10k and inflation is 3%, the contribution in year two is $10.3k. This is adjusted every year based on variable changes in inflation.

6) Returns ignore taxes. Individual tax situations are far too complex for a tool like this to model. Your mileage may vary.

With those caveats in mind, I highly recommend you go play with the site and bookmark it for future use. Tyler isn’t sure about what he wants to do with it, but watching how real people make use of it is probably a good first step.

Check it out here:

RT @ReformedBroker: The Coolest Portfolio Tool on the Web http://t.co/EyH1pF6DVN

RT @ReformedBroker: The Coolest Portfolio Tool on the Web http://t.co/EyH1pF6DVN

RT @ReformedBroker: THE COOLEST PORTFOLIO TOOL ON THE WEB

http://t.co/X9AbfdrO5p http://t.co/55PUVR8CfH

RT @ReformedBroker: THE COOLEST PORTFOLIO TOOL ON THE WEB

http://t.co/X9AbfdrO5p http://t.co/55PUVR8CfH

RT @ReformedBroker: THE COOLEST PORTFOLIO TOOL ON THE WEB

http://t.co/X9AbfdrO5p http://t.co/55PUVR8CfH

RT @RockTheBoatMKTG: Individual innovation is possible! @reformedbroker raves about a portfolio tool created by an engineer http://t.co/1Ji…

RT @ReformedBroker: THE COOLEST PORTFOLIO TOOL ON THE WEB

http://t.co/X9AbfdrO5p http://t.co/55PUVR8CfH

The Coolest Portfolio Tool on the Web http://t.co/LmQx8ho5LL

The Coolest Portfolio Tool on the Web http://t.co/FlCgjJnUDN

Nice portfolio visualisation by #PortfolioCharts see, http://t.co/tToBpJhRND http://t.co/nYjYE238cs HT @ReformedBroker @RhinoTroy #fintech

RT @DrewWalkCo: Nice portfolio visualisation by #PortfolioCharts see, http://t.co/tToBpJhRND http://t.co/nYjYE238cs HT @ReformedBroker @Rhi…

RT DrewWalkCo: Nice portfolio visualisation by #PortfolioCharts see, http://t.co/m2iq4qHm0t … http://t.co/u5n8aZW85j HT ReformedBroker …

RT @ReformedBroker: The Coolest Portfolio Tool on the Web http://t.co/EyH1pF6DVN

RT @ReformedBroker: The Coolest Portfolio Tool on the Web http://t.co/EyH1pF6DVN

The Coolest #Portfolio Tool on the Web http://t.co/Qu5TTrveSE