Earlier this year, everyone in investment universe seemed to be plowing money into funds and products marketing the low volatility anomaly. There were a host of new “low-vol” strategies launched and a handful of ETFs, all of them showing the decades-long superiority of low beta strategy. Those with a quantitative background immediately recognized what was really going on – it was just dividends and the value premium in drag – you see, low volatility sectors and stocks tend to have a lot of overlap with high-yielders and “cheaper” names.

Unfortunately, by adding low-vol index products to their portfolios, well-meaning advisors and investors were essentially chasing the most expensive, overbought stocks in the marketplace just as they were peaking out in valuation for the cycle.

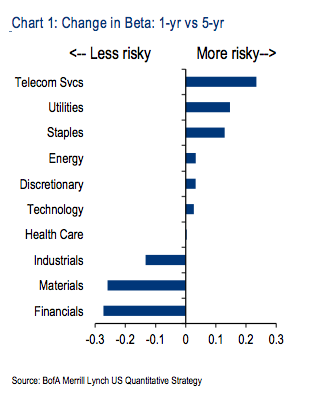

Merrill’s chief of quant strategy, Savita Subramanian, looked at this phenomenon on Friday and notes that all of our notions of “risky” and “defensive” may need to be flipped upside down as the year draws to a close…

The changing risk profile for sectors

With this year’s equity returns being largely driven by sectors generally thought to

be lower beta areas of the market (Utilities, Staples and Telecom), our work

suggests that the definition of risk versus safety could dramatically change following

this year. Sectors that have grown higher beta, as measured by the biggest positive

discrepancy between 1-year and 5-year betas, are Telecom, Utilities and Consumer

Staples. On the flipside, some decidedly cyclical sectors like Financials, Materials

and Industrials have seen a collapse in betas using a 1-yr versus 5-year measure

Josh here – So where is the true low beta investment to be had? It’s very interesting to see the materials stocks and banks and industrials declining in volatility relative to the supposedly stable sectors like telecom and utilities.

[…] There you can find 37060 additional Information on that Topic: thereformedbroker.com/2013/11/03/rearranging-your-thoughts-on-which-sectors-are-risky/ […]

[…] There you will find 6132 more Information on that Topic: thereformedbroker.com/2013/11/03/rearranging-your-thoughts-on-which-sectors-are-risky/ […]

I’m a New York City-based financial advisor at Ritholtz Wealth Management LLC. I help people invest and manage portfolios for them. For disclosure information please see here.

Get a Full Investor Curriculum: Join The Book List

Every month you'll receive 3-4 book suggestions--chosen by hand from more than 1,000 books. You'll also receive an extensive curriculum (books, articles, papers, videos) in PDF form right away.

… [Trackback]

[…] Info to that Topic: thereformedbroker.com/2013/11/03/rearranging-your-thoughts-on-which-sectors-are-risky/ […]

… [Trackback]

[…] Read More on on that Topic: thereformedbroker.com/2013/11/03/rearranging-your-thoughts-on-which-sectors-are-risky/ […]

… [Trackback]

[…] Read More on on that Topic: thereformedbroker.com/2013/11/03/rearranging-your-thoughts-on-which-sectors-are-risky/ […]

… [Trackback]

[…] There you can find 37060 additional Information on that Topic: thereformedbroker.com/2013/11/03/rearranging-your-thoughts-on-which-sectors-are-risky/ […]

… [Trackback]

[…] Find More on that Topic: thereformedbroker.com/2013/11/03/rearranging-your-thoughts-on-which-sectors-are-risky/ […]

… [Trackback]

[…] Find More on that Topic: thereformedbroker.com/2013/11/03/rearranging-your-thoughts-on-which-sectors-are-risky/ […]

… [Trackback]

[…] Find More here to that Topic: thereformedbroker.com/2013/11/03/rearranging-your-thoughts-on-which-sectors-are-risky/ […]

… [Trackback]

[…] Info on that Topic: thereformedbroker.com/2013/11/03/rearranging-your-thoughts-on-which-sectors-are-risky/ […]

… [Trackback]

[…] Find More here to that Topic: thereformedbroker.com/2013/11/03/rearranging-your-thoughts-on-which-sectors-are-risky/ […]

… [Trackback]

[…] Find More on to that Topic: thereformedbroker.com/2013/11/03/rearranging-your-thoughts-on-which-sectors-are-risky/ […]

… [Trackback]

[…] Info to that Topic: thereformedbroker.com/2013/11/03/rearranging-your-thoughts-on-which-sectors-are-risky/ […]

… [Trackback]

[…] There you will find 6132 more Information on that Topic: thereformedbroker.com/2013/11/03/rearranging-your-thoughts-on-which-sectors-are-risky/ […]

… [Trackback]

[…] Find More to that Topic: thereformedbroker.com/2013/11/03/rearranging-your-thoughts-on-which-sectors-are-risky/ […]