Josh here – we are extraordinarily fortunate to have tax planning expert and certified financial planner Bill Sweet working every day on behalf of our clients, finding solutions and saving people money like you wouldn’t believe. Bill’s expertise has enabled us to take on more complicated cases and streamline the asset “location” process across our entire practice. On top of that, he’s a great guy all-around and clients love working with him.

I asked Bill to take a stab at what the GOP’s Big Six tax reform plan, dropped yesterday, might mean for our clients. Below, his item-by-item bullets. This might be the most helpful thing on the topic for investors you’ll see all week. You can read more about Bill’s story here.

I hope this gives you a good understanding of what’s going on!

***

The new Big Six tax reform proposal dropped yesterday and is fresh on the streets. While the nine-page summary does answer some of the questions we raised in April, the Unified Framework for Fixing Our Broken Tax Code (an actual title for an actual government document!!) remains heavy on concepts but short on details – it is still more of a wish-list than a fully fleshed-out plan.

So we do the best we can do at this point is interpret how this latest proposal might impact taxpayers and more specifically Ritholtz Wealth investors. But the actual analysis for specific taxpayers will have to wait until Congress kicks into gear and actually gives us numbers – not broad concepts – to work with.

Let’s start with the good stuff – items we feel will generally benefit taxpayers.

AMT (Alternative Minimum Tax) Repeal

On the chopping block is the most confusing and least-understood parts of the tax code. It was originally intended to close a loophole wealthy taxpayers were exploiting to artificially lower their tax rates through excessive deductions. Because of numerous failed patches and failures to adjust for inflation, the AMT now primarily hits middle class taxpayers with lots of kids or residing in high cost-of-living states. Because it is complex, difficult to plan for, and likely doesn’t achieve its original intent, most taxpayers (and accountants) will be thrilled to see the AMT put to rest.

Fewer Tax Brackets

The outline suggests replacing the current tax brackets – 10% / 15% / 25% / 28% / 33% / 35% / 39.6% – with only three – 12% / 25% / 35%. We feel this is generally a good thing as it simplifies an unnecessarily complex system. It is important to note, however, that without knowing where each bracket starts and ends, it is impossible to estimate what the impact of this change will be on specific taxpayers or the tax system as a whole.

Doubles the Standard Deduction (but removes personal exemptions)

Taxpayers who don’t itemize their deductions (typically, those who rent instead of own their primary residence) seemingly get a large gift. The standard deduction seems to double, but at the cost of personal exemptions at $4,000 a person being removed. You have to combine the two to understand the actual impact as what looks like a 50% increase for many taxpayers is closer to 15%.For a married couple the total increases to $24,000 from $20,000 (made up of $12,000 standard + $8,000 in exemption in the current structure).

Meanwhile, households with one child just break even – currently $12,000 standard deduction + $12,000 exemptions = $24,000, exactly the standard deduction being proposed. Households with two or more children would likely receive a lower total deduction + exemptions than under the current structure, potentially harming larger families.

The proposal offers “significant increases [to] the Child Tax Credit” to make up for this.

The ultimate impact will depend on the details to be determined, but I’d guess that this change would result in fewer households paying income tax. Already, about 45% of households don’t pay any income taxes at all. This is likely because they don’t make enough income to file a return, or they file but a combination of their standard deduction or tax credits like the Earned Income Tax Credit or Child Tax Credit offsets taxes calculated on their Form 1040. Doubling the standard deduction is likely to increase that total in theory, depending on the fate of the EITC and CTC.

Lowers Rate on Pass-through Businesses

Typically small (and sometimes large) businesses take the form of sole proprietorships, partnerships, LLC/LLPs, and S-corporations. They do so to avoid double-taxation using a mechanism called pass-through income – the corporate or partnership entity pays no tax at the corporate level, but instead distributes all income through to owners pro-rata to be paid at individual rates.

The differential between the proposed pass-through rate of 25% and the highest marginal individual rate of 35% is significant and tantalizing. Yet the proposal warns that “committees will adopt measures to prevent recharacterization of personal income into business income.”

We have no clue what this means – after all, business income is personal income for your local barber or hedge fund manager, at the end of the day.

Secretary of the Treasury Steven Mnunchin has stated publicly that there will be a difference between certain service-based businesses – he used the example “accountant firm” which would not be eligible for the pass-through rate – in opposition to “a business that’s creating manufacturing jobs,” which supposedly would be eligible for the lower rate “to help create jobs and better wages.” So how the government chooses to draw the line is anyone’s guess outside of the unfortunate and incorrect conclusion that accountants don’t create jobs.

I’m just hoping that it doesn’t boil down to the government identifying winners and losers arbitrarily (or worse, based on ideology). About 85% of the US economy today is service-based, and high-wage jobs for Amazon and UPS are just as valuable as high-wage jobs for Boeing and General Motors, in our opinion.

Also, assuming that many mom-and-pop businesses will fall into the 25% individual tax bracket anyway, do small businesses actually benefit from this?

Estate & Generation-Skipping & Gift Tax Repeal

The proposal calls this the “death tax” since it this sounds like a big scary thing, but only applies to couples whose assets exceed $10.9 million who haven’t bothered to a hire competent estate planner. Estate tax today only affects about 0.14% of estates, meaning that 99.8% of the population is currently exempt. That said, a repeal of the estate and GST tax will benefit wealthy taxpayers who don’t believe in advance planning, allowing their heirs to inherit most of their wealth.

Let’s now take a look at how the proposal would (likely) harm certain taxpayers, and how.

Single Parents

Today, single parents are eligible for a head-of-household filing status, which gives the taxpayer favorable tax brackets somewhere in between single and married-filing-joint rates. They also receive a 50% boost to their standard deduction.

This filing status appears to be gone in the new proposal, likely increasing the tax paid by single parents should they be forced to file as single taxpayers. Theoretically, increases to the Child Tax Credit may offset some of this increase, but additional CTC benefits would have to be significant to keep pace with the additional deduction offered to single taxpayers as part of the proposal.

Households With Two or More Children

Since a household with two parents + two children are eligible for 4 x $4,000 personal exemptions at a total of $16,000, removing this and offsetting it with an additional $12,000 standard deduction leaves a family of four reporting $4,000 more in taxable income in the new plan vs. old. That’s a pretty raw deal.

The proposal promises an increase in the Child Tax Credit to offset this, but there is likely a reason that they didn’t quantify the figure.

I should also point out that this only affects households who receive a standard deduction – households who itemize, typically middle-class families who own a home as their primary residence, lose their exemptions at $4,000 per person but receive nothing back in the form of increased deductions. In fact. it’s probably worse for anyone who owns a home.

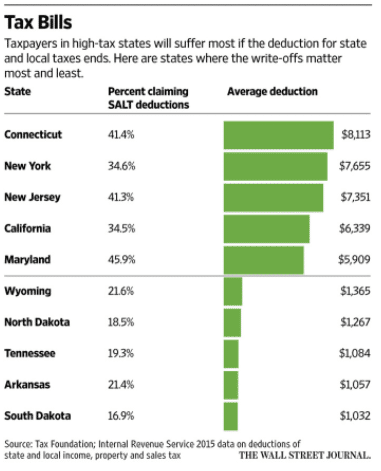

Anyone Paying Real Estate Taxes

If you live in a high property tax state, your property taxes are no longer deductible under the Unified Framework for Fixing Our Broken Tax Code. The UFFOBTC does retain mortgage interest deductions, which is significant. The real estate lobby will likely have something to say about this to their local representative, and so should you if you fork over taxes on your personal residence.

Anyone Paying State Income Taxes

If you live in a high income tax state, your income taxes are no longer deductible under the Unified Framework for Fixing Our Broken Tax Code.

If I end up marching on Washington to protest the further breaking of the Broken Tax Code, this is the thing that is going to trigger me personally – a large percentage of my clients (and me) pay significant income taxes to the great State of New York. This is atrocious and I do take this up with my local representative frequently, but a silver lining to help offset the blow is that I can at least deduct these against my federal income taxes.

So someone who pays state income tax AND real estate taxes is going to rightly be upset about UFFOBTC. I’ll be leading the charge.

It is also focused pain on high-income, high-tax states like New York, New Jersey, California, Oregon, and Illinois, thus theoretically benefitting no income tax and low property tax states like Texas, Florida, Tennessee, and Nevada.

Finally, here are some key questions / observations:

Did Congressional Leaders Learn Anything from Health Care “Reform” ?

From my view, the three ACA repeal efforts were heavy on campaign promises to do something, but really, really light on details. The public was made aware of this lack of planning, and the historically unpopular ACA suddenly became something that even GOP representatives rallied around.

Nearly everyone agrees that our tax code is unnecessarily complex and potentially “broken” – we get it. What are you going to replace it with exactly? How much thought went into this thing? Is your proposal going to unbreak or further break the tax code?

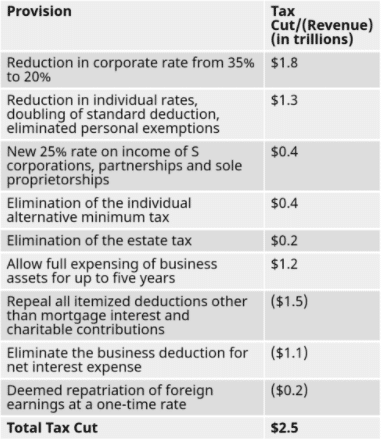

Do the Cuts Total More or Less than $1.5 Trillion of Lost Federal Revenue?

The $1.5 trillion number is very important. If projections show that the total revenue differential over the next 10 years is $1.5 trillion or less, a simple Senate majority of 51 votes can pass under a Congressional procedure called reconciliation that is somehow more complicated than our tax code.

More than $1.5 trillion, and a 60 vote majority is required, meaning that at least eight Democratic Senators need to sign on.

Our friend Tony Nitti did the math and shows that back-of-the-envelope they’ll need to add back in $1 trillion in cuts to make it work:

Furthermore, do we not care about the Federal Debt anymore? Subtracting even $1.5 trillion in federal revenue over 10 years probably decreases annual receipts by about 5%. Given that we’re running a deficit right now, what measures will be taken in government spending to make up for this additional shortfall?

What Happens to Existing Tax Credits?

We discuss the Earned Income Tax Credit briefly above, but will it exist in the new framework? A lot of economists find that the EITC is a powerful incentive to get people to work (since by definition the family must have earned income) and plays an important role in getting lower-income families some tax relief by boosting their refund by small amounts.

What About Capital Gains / Qualified Dividends?

There is no mention of changing favorable capital gains rates on long-term investment holdings, nor favorable tax treatment for dividends of US companies. Can we assume that these rates – capped at 15% for most taxpayers – continue in the new framework?

What about the Net Investment Income Tax (3.8%) on taxpayers earning more than $250,000 per year? Or the additional Medicare tax tied to the ACA?

We don’t know the answers to these and many other questions, making it speculation at best at this stage.

Still.

***

If you want to talk to Bill about your tax situation, financial plan or portfolio, hit us up here.

[…] What We’re Telling Our Wealth Management Clients About Tax Reform (thereformedbroker.com) – This is a great detailed look at how the new Trump tax plan might impact you. […]

[…] By Bill Sweet […]

[…] If you would like to read more about the other details of this proposal, my colleague and tax Guru, Bill Sweet, wrote this excellent piece. […]

… [Trackback]

[…] Find More on that Topic: thereformedbroker.com/2017/09/28/what-were-telling-wealth-management-clients-about-tax-reform/ […]

… [Trackback]

[…] There you can find 38689 more Info to that Topic: thereformedbroker.com/2017/09/28/what-were-telling-wealth-management-clients-about-tax-reform/ […]

… [Trackback]

[…] Find More Info here on that Topic: thereformedbroker.com/2017/09/28/what-were-telling-wealth-management-clients-about-tax-reform/ […]

… [Trackback]

[…] Read More on that Topic: thereformedbroker.com/2017/09/28/what-were-telling-wealth-management-clients-about-tax-reform/ […]

… [Trackback]

[…] Find More on to that Topic: thereformedbroker.com/2017/09/28/what-were-telling-wealth-management-clients-about-tax-reform/ […]

… [Trackback]

[…] Information to that Topic: thereformedbroker.com/2017/09/28/what-were-telling-wealth-management-clients-about-tax-reform/ […]

… [Trackback]

[…] Read More to that Topic: thereformedbroker.com/2017/09/28/what-were-telling-wealth-management-clients-about-tax-reform/ […]

… [Trackback]

[…] Find More on that Topic: thereformedbroker.com/2017/09/28/what-were-telling-wealth-management-clients-about-tax-reform/ […]

… [Trackback]

[…] Find More on that Topic: thereformedbroker.com/2017/09/28/what-were-telling-wealth-management-clients-about-tax-reform/ […]

… [Trackback]

[…] Find More on to that Topic: thereformedbroker.com/2017/09/28/what-were-telling-wealth-management-clients-about-tax-reform/ […]