Among the nightmare scenarios that could knock this market off its bull course and do some real damage would be the forced deleveraging of the “risk parity” funds that have grown to comprise hundreds of billions of dollars of institutional money.

As an overgeneralization, risk parity funds seek to target specific levels of volatility and create a sort of “all-weather” strategy where bonds are leveraged up to offset the wild swings of stocks. This strategy works well when bonds are the steadier asset component of the portfolio and are somewhat or very non-correlated to stock returns.

Unfortunately, this is not assured to always be the case. In the summer of 2013, after some hawkish comments on rates / QE from the Bernanke Fed, we found out just how scary things could be when stock and bond correlation shoots up and the enormous, rules-based risk parity hedge funds are not ready for it. The rules that govern their exposures trigger the sort of forced deleveraging that could really play havoc with the stock and Treasury markets. They also can be self-reinforcing if the unwind is powerful enough – selling begets more selling which, well, you get the drift.

With bonds and stocks both at elevated levels, and the leverage on bonds at risk parity funds very overweight, this is a legitimate thing to be thinking about right now.

Bank of America Merrill Lynch’s Global Equity Derivatives Research team looks at the risks to the market posed by forced deleveraging of risk parity strategies – should we get a repeat episode of bonds and stocks selling off together…

Last week’s sharp sell-off in JGBs following the BoJ’s decision not to cut rates renewed investor fears of forced selling by risk parity funds. However, the spill-over into US Treasuries was relatively muted…For this very reason, the latent risk in this corner of the quant fund space remains worth monitoring.

To the extent that the leverage is via vol control overlays, there are reasonable concerns on the potential market impact should these model-driven investments be forced to simultaneously deleverage.

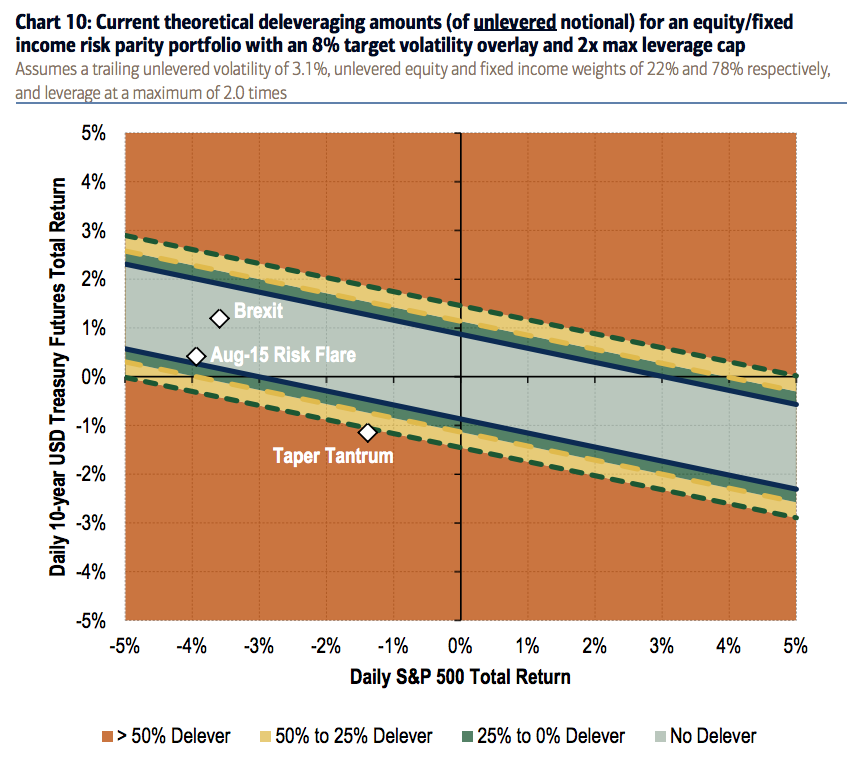

In the chart below, BAML breaks down the scenarios in which bonds and stocks either rise together, fall together or rise and fall separately. You can see that the aforementioned 2013 “Taper Tantrum” was a consequence of the sort of simultaneous volatility spike we should be concerned about:

Josh here – Anything in the lower lefthand quadrant, in terms of asset class vol, could trigger massive amounts of selling. The question is whether something like that could ultimately be contained, or how much damage would need to happen before it burns itself out.

The main takeaway here is the most risk of model driven deleveraging from vol controlled risk parity funds comes when both volatility and correlation of the underlying components rise together.

Source:

Understanding when risk parity risk increases

Bank of America Merrill Lynch – August 9th 2016

[…] Should we be concerned about a risk-parity de-leveraging? (thereformedbroker) […]

[…] This Would be Not Good – The Reformed Broker Changing Classifications – The Research Puzzle Distractions Cause Investors 115% – The Irrelevant Investor Oil and Stocks Part Ways – Crossing Wall Street The Best Stock Market Indicator is Financial Media Competition for Clicks – Price Action Lab Blog Should You Hedge Your Portfolio Against Zika? – The Reformed Broker This Jarring Chart May Explain why Investors are Flooding into the Stock Market – Yahoo! […]

[…] Commitment of Traders (COT): VIX net speculative positioning (2016.08.23) | Commodity Futures Tradin… Along with this summer’s incredibly low vol, VIX speculators have reached an alltime record net short positioning, and BAML is alarmed by the proliferation of return-enhancing strategies (like selling puts)… “The recent chase for yield has potentially reached an important inflection point. Selling vol to enhance yield is now at an extreme level, with net speculative VIX exposure at all time shorts. Furthermore, this reach for yield is apparent across FX, equity, and fixed-income markets… complacency combined with short vol exposure could set up the market for a highly volatile and correlated sell off on the next shock.” [See also: S&P 500 net speculative positioning is overwhelmingly long & at ytd highs] #Bearish $VXX #options […]

… [Trackback]

[…] Info to that Topic: thereformedbroker.com/2016/08/10/this-would-be-not-good/ […]

… [Trackback]

[…] Info to that Topic: thereformedbroker.com/2016/08/10/this-would-be-not-good/ […]

… [Trackback]

[…] There you will find 98603 more Info to that Topic: thereformedbroker.com/2016/08/10/this-would-be-not-good/ […]

… [Trackback]

[…] Info on that Topic: thereformedbroker.com/2016/08/10/this-would-be-not-good/ […]

… [Trackback]

[…] Read More to that Topic: thereformedbroker.com/2016/08/10/this-would-be-not-good/ […]

… [Trackback]

[…] Read More here to that Topic: thereformedbroker.com/2016/08/10/this-would-be-not-good/ […]

… [Trackback]

[…] Here you can find 25172 additional Info to that Topic: thereformedbroker.com/2016/08/10/this-would-be-not-good/ […]

… [Trackback]

[…] Find More Info here on that Topic: thereformedbroker.com/2016/08/10/this-would-be-not-good/ […]

… [Trackback]

[…] Read More on to that Topic: thereformedbroker.com/2016/08/10/this-would-be-not-good/ […]

… [Trackback]

[…] Here you can find 38740 more Information to that Topic: thereformedbroker.com/2016/08/10/this-would-be-not-good/ […]