361 Capital portfolio manager, Blaine Rollins, CFA, previously manager of the Janus Fund, writes a weekly update looking back on major moves, macro-trends and economic data points. The 361 Capital Weekly Research Briefing summarizes the latest market news along with some interesting facts and a touch of humor. 361 Capital is a provider of alternative investment mutual funds, separate accounts, and limited partnerships to institutions, financial intermediaries, and high-net-worth investors.

361 Capital Weekly Research Briefing

June 10, 2013

Timely perspectives from the 361 Capital research & portfolio management team

Written by Blaine Rollins, CFA

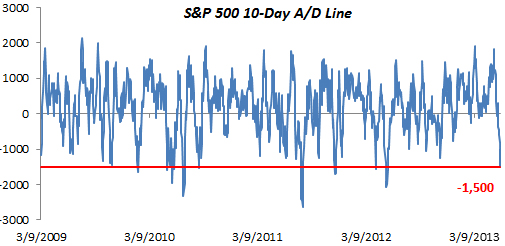

And like clockwork, stocks bounced both from their very short term oversold point and off the 50day moving average on Wednesday…

@bespokeinvest: The 10-day A/D line is now at its most oversold level in more than a year. What does this mean for the market?

(BespokeInvest)

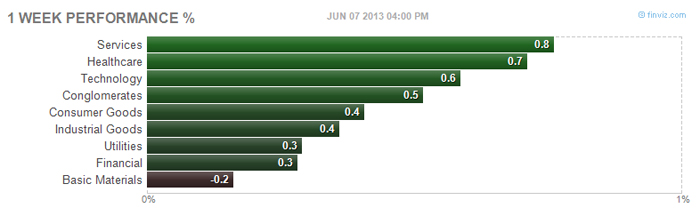

It was a broad-based bounce attempt with only the Materials sector finishing lower (most tied to emerging markets)…

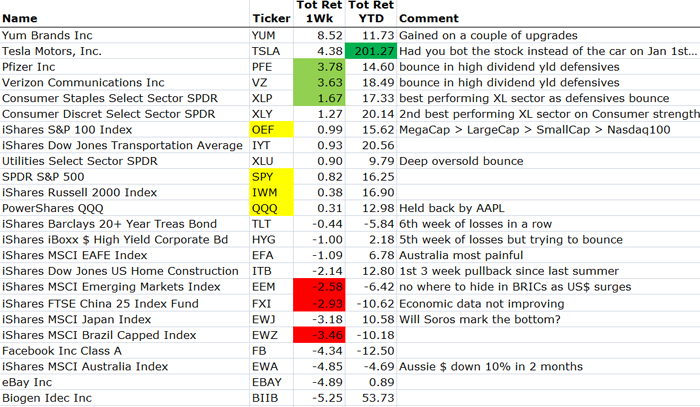

A tough week for the emerging markets again as they suffer from U.S. dollar strength against their local currencies + few improving economic data points…

One reason for the continued outperformance in Consumer Discretionary sector…

(ISI Group)

Speaking of economic data points, last week was a busy one, but banana slugs in Santa Cruz might have had more momentum than what we saw…

Weekly Indicators: moving forward in first gear edition… May monthly data reported this past week was dominated by yet another tepid jobs report of +175,000 with a slight increase in the unemployment rate due to more people entering the labor force. Average hourly earnings barely increased, so real earnings probably fell slightly for the month. The ISM reported that manufacturing contracted slightly, which services expanded at slightly better rate. Auto sales increased slightly for the month, but have been flat over a 6 month period. April factory orders also increased, but have also been flat for a 6 month period. Consumer credit increased. In the rear view mirror, in the first quarter productivity increased and unit labor costs fell sharply, but only partially reversing a huge spike in the fourth quarter due to income being shifted forward into that quarter.

(BonddadBlog)

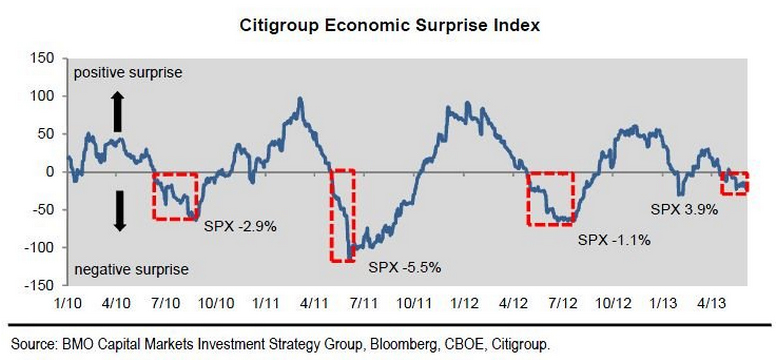

As this economic surprise index chart highlights, the equity market disapproves of missed expectations…

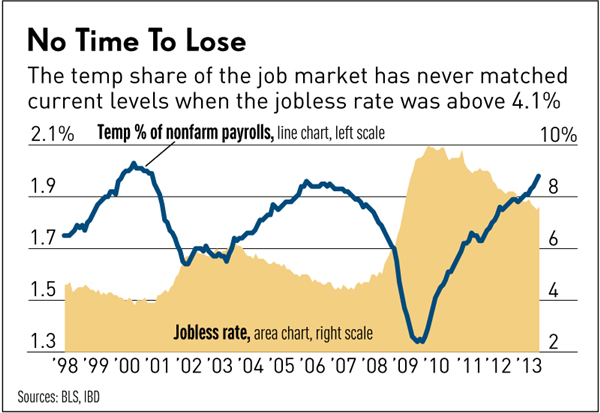

One of the strongest areas of the May jobs report was temporary employment. Put the group on your watchlist. The wind is at the industries back now and if/when the economy gets stronger, the temp companies will gain from the permanent employment fees they earn from the employers.

Temp employment grew by 25,600, eclipsing the previous high seen in April 2000. In the past four months, the temp industry has added 99,000 jobs, a spurt that has outpaced the gains in every other sector, except the restaurant industry. Temp jobs now account for 1.98% of nonfarm payrolls, just below the prior record of 2.03% — but higher than at any time the jobless rate was above 4.1%. That is a noteworthy development, given that temp employment tends to peak with the economic cycle as tight labor markets make temp agencies more indispensable for filling short-term hiring needs.

The boom in temp employment is no surprise because the industry offers ways to minimize ObamaCare’s fines for firms with at least 50 full-time-equivalent workers. One way temp firms can help is by helping employers to stay below that 50-worker threshold and free from ObamaCare’s regulations. Firms above that level who don’t provide health coverage will face a $2,000 per-worker fine (minus 30 workers), so the 50th employee could mean a $40,000 fine under ObamaCare. As Keith Waddell, Robert Half International chief financial officer, said on an earnings call earlier this year, “we can legally help them remain under 50, since we are the employer of record for the temporaries we provide to them.”

(IBD)

Not surprising to see that Greece is seeing a pickup in tourism… A great place to visit with now much lower prices…

@economistmeg: #Greece international tourist arrivals +6.05% yoy to 2.44m in 5M’12 and +18.4% yoy to 1.43m in May (SETE) #eu #euro #eurozone

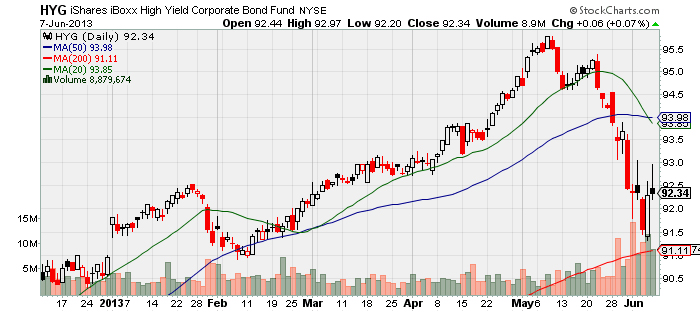

The pain in the bond market makes it to the mainline press. Now wait for investors to get their May and June brokerage statements…

As if it wasn’t bad enough for the millions of Americans scraping by on paltry interest payments, now they face another threat: the loss of principal on their bonds and other fixed-income assets. The month of May, and this first week of June, was terrible for many fixed-income investors who have spent the last few years reaching for higher yields. If there was an index for fixed income with the status of the Dow Jones Industrial Average or Standard & Poor’s 500 Index for stocks, the carnage in fixed-income markets would have been a big story and we’d all be talking about a bear market in bonds.

Consider the damage: mutual funds that invest in long-term United States Treasury bonds lost an average 6.8 percent in May, according to Morningstar, with the loss in principal wiping out years of interest payments. But that’s not the worst-hit sector. Higher-yielding bonds and fixed-income securities, to which investors have turned in droves in recent years, have suffered even more, especially mortgage-backed securities and emerging market debt, as well as just about anything that uses borrowing to increase returns. Many individual securities and funds were hit much harder than the averages. Vanguard’s Extended Duration Treasury Index fund was down more than 6 percent in the last month. In the mortgage area, Annaly Capital Management, a popular real estate investment trust that invests in mortgages, fell 8.7 percent, and an iShares mortgage exchange-traded fund lost 10.4 percent. Pimco’s Corporate Opportunity Fund, which is managed by the star analyst Bill Gross and which invests in a mix of corporate bonds and mortgage-backed securities and uses some borrowing, lost nearly 13.4 percent. Annualized, such declines are off the charts.

(NewYorkTimes)

As the New York Times notes, junk bonds have been crushed. Time for this KEY risk thermometer to find a low and help equities, or not…

Not helping prices will be the now outflowing assets of fixed income mutual funds and ETFs…

Investors have pulled a record $12.53bn out of global bond funds in the past week, beating a speedy retreat from fixed income holdings that can fall in value as interest rates rise. EPFR Global, the research firm, said the selling wave swept across all major classes of bond funds, including $6bn of outflows from junk bonds funds and $1bn from emerging markets funds. Two-thirds of the total outflows came from U.S. funds, where nervousness over the Federal Reserve’s next moves in monetary policy is at its height. EPFR’s data stretch back to 2001. Market interest rates have already jumped in response to speculation that the central bank will begin to taper its purchases of bonds. Bond valuations move inversely to interest rates. The market’s benchmark, the Barclays US Aggregate Index, which consists of Treasury, mortgage and corporate debt, has registered a decline of 1 percent for 2013, its worst year-to-date performance since the great bond market rout of 1994.

(FT)

If there is one CFO who gets a prize for nailing the bottom in borrowing rates…

@ParHedge: Apple couldve hardly picked a better time to borrow $17b: it’s pocketing $724m in interest savings over the life of bonds v rates now.

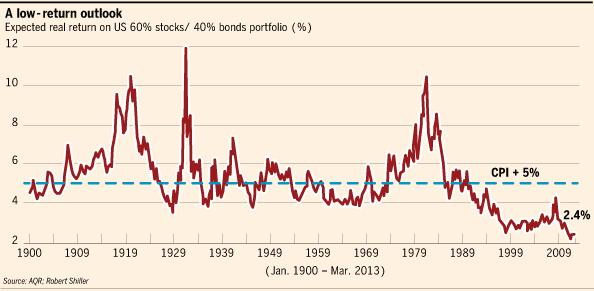

Cliff Asness outlines how difficult it will be to generate inflation beating returns…

The chart was produced by Cliff Asness, the founder of AQR Capital Management in New York. It shows what the forecast 10-year return, after inflation, would have been on a portfolio with 60 percent in equities and 40 percent in bonds at every point since the beginning of the last century. On this basis, the 10-year outlook has never been so gloomy…So long-term investors have few places to hide. Stocks look expensive relative to their own history, but less expensive than bonds – so there is no point in switching from stocks to bonds. Meanwhile, managers have little reason to move out of bonds, particularly when regulators are prodding funds to hold them. What can we do about this? Mr. Asness suggests that those wanting a return of 5 percent must overcome squeamishness and resort to leverage and derivatives (to magnify returns from safe but boring trades) and selling short (to profit when security prices go down). Academics have identified enough long-term anomalies in stock markets that investors might have a fighting chance of getting to 5 percent. For example, cheap stocks tend to outperform, while stocks with strong momentum tend to keep moving in the same direction.

(FT)

Byron Wien thinks it is time for a near-term pause in equity returns…

“The market has already given you a full-year’s performance and we’re only at the beginning of June. It’s unrealistic to think the market could continue to go up at the rate it’s gone up so far this year. There’s bound to be a correction. You have earnings problems, you have the economy slowing, you have all the economies around the world slowing, demand for U.S. products are slowing, so my view is it’s time to be cautious.”

(Byron Wien via Fox Business News)

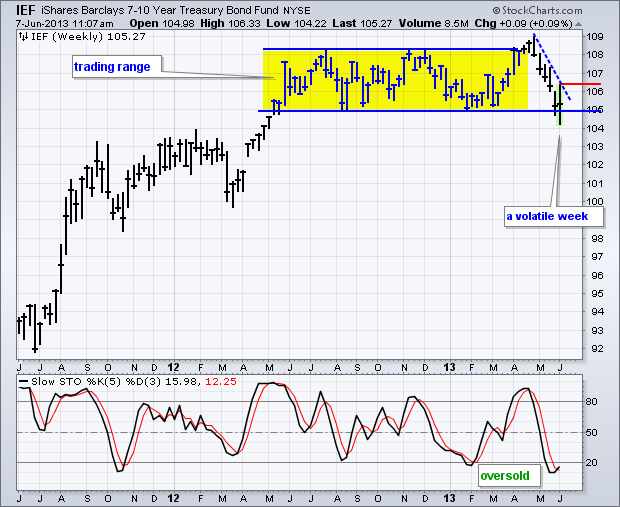

So will they bounce Bonds this week or is the bottom about to fall out?

If you think bonds are oversold here, Barron’s is highlighting the Utility sector this weekend, which could catch a move higher given the oversold position of the group. Go back and look at the November XLU chart when the sector was equally oversold.

The sector looks attractive after a 10% selloff since its late April highs that has been driven largely by a nearly half-percentage-point rise in Treasury yields and fear of even higher bond yields. Utilities now are up about 8% in 2013. “We like the basic investment thesis for regulated utilities: 4%-5% [earnings per share] growth, 4% dividend yields, and 0.5-0.7 beta create a high-single-digit annual return in a low-risk package,” wrote Credit Suisse analyst Dan Eggers in a recent note. A beta of about 0.6 means utilities have 60% of the volatility of the S&P 500 Index.

(Barron’s)

The same case could be made for the REIT sector…

The REITs in the IYR continue to punish bottom-fishers, with a straight-line down move since May 22nd on very heavy sell volume. The good news with each new real estate mogul being shaken out of bottom-picking attempts is that we get one step closer to an actual tradable bottom.

(iBankCoin)

The largest banker in the world reminds you that volatility will be around for a while…

Global markets will face increased volatility as central banks bring interest rates back to normal levels, JPMorgan Chase & Co. (JPM) Chief Executive Officer Jamie Dimon said. “We should all hope for a normalization of interest rates — that’s a good thing,” Dimon said today during a panel discussion at the Fortune Global Forum in Chengdu, China. “As we go back to normal, it’s going to be scary, and it’s going to be kind of volatile.”

(Bloomberg)

Speaking of volatility, look at this 3 week reversal in the Yen…

This Yen move combined with the equally violent moves in the Nikkei and Japanese Bonds is creating booming sales of Pepto-Bismol and Hard Liquor in NYC, London, and Zurich…

Some of the world’s biggest quant hedge funds have suffered steep losses in the past two weeks following the sell-off in global bond markets. So-called “CTAs”, which use computer models to automatically spot and ride market trends, were caught out as investors anticipated an end to the Federal Reserve’s measures to stimulate the U.S. economy, triggering a global rout in fixed income investments. Bond yields have risen sharply from some of their lowest levels in decades in the past fortnight, leaving funds with large holdings badly hit. Many quant funds have been major buyers of bonds over the past few years as their algorithms have followed yields lower. “Since mid-May it has been a perfect storm of some of the biggest trends in markets reversing all at once,” said a senior manager at one large quant fund. “It has been particularly brutal.”

(FT)

Meanwhile the majority of active mutual fund managers continue to only dream of outperformance…

2013 is a challenging year for active managers: 72% of large cap funds have underperformed, and by an average of 228bp. Equity indices are up about 15% YTD, and the typical fund is up 13% (see Figure 3), or missing its benchmark by 228bp. In fact, about 68% of fund managers are missing their benchmarks in 2013. The spread between those beating by 250bp and those missing by 250bp is 2,000bp in 2013. This is worse than usual, particularly through the end of May. In terms of funds trailing, the most notable large-cap laggards are those benchmarked against the Russell 1000 Value Index, with 76% trailing in 2013 through May. On small cap, it is those managers tracking the Russell 2000 Growth index, with 81% missing that benchmark.

(JPMorgan)

If only the underperforming managers owned more Google…

Everywhere one looks, Google is doing remarkable things. It could soon overtake Apple in downloads of applications; it is developing self-driving cars; people wear its kooky augmented reality Glass spectacles; it is signing renewable power deals in South Africa and Sweden. From being a one-product company that tapped a stream of wealth with paid internet search, Google is emerging as the dominant consumer technology company of the early 21st century, along with Amazon. Fred Wilson, a leading New York venture capitalist, accuses it of trying to control the internet, “like Microsoft tried with personal computing … Who will stop Google?”

My answer is: nobody, or not easily. Indeed, the best comparison for Google seems to me not Microsoft in the 1980s, but General Electric in the late 19th century – the age of electrification. Like GE, Google is a multifaceted industrial enterprise riding a wave of technology with an uncanny ability not only to invent far-reaching products but also to produce them commercially. It coincides with Larry Page’s ascent to being undisputed leader of the company he founded at Stanford University with Sergey Brin 15 years ago. Instead of the “Google guys” – Mr. Page, Mr. Brin and Eric Schmidt, its former chief executive and now chairman – running it as an amiable mixture of a company and a chaotic research lab, Mr. Page has made it formidably focused.

(FT)

Or maybe they should follow Soros back into Japan?

Investors of all types are selling Japanese stocks, worried that a recovery might not be easy for the government to engineer. But George Soros’s firm, Soros Fund Management LLC, is buying, once again. Mr. Soros’s firm, which manages $24 billion of the investor’s cash, had sold much of its Japanese stock position in May, before the recent, steep selloff, according to a person close to the matter. But Mr. Soros’s firm is now betting on the Japanese market again, the person said. Mr. Soros, who had scored gains of more $1 billion on bets against the Japanese yen and on Japanese stocks, returned to the market this week after seeing some signs of stability in the Japanese bond market, the person said.

(WSJ)

The one time it is GREAT to be blue…

Sports Tweet of the Week…

And finally…

@SJosephBurns: “There is a time to go long, time to go short, and time to go fishing.” ~ Jesse Livermore

Blaine Rollins, CFA, is managing director, senior portfolio manager and a member of the Investment Committee at 361 Capital. He is responsible for manager due-diligence, investment research, portfolio construction, hedging and trading strategies. Previously Mr. Rollins served as Executive Vice President at Janus Capital Corporation and portfolio manager of the Janus Fund, Janus Balanced Fund, Janus Equity Income Fund, Janus Aspen Growth Portfolio, Janus Advisor Large Cap Growth Fund, and the Janus Triton Fund. A frequent industry speaker, Mr. Rollins earned a Bachelor’s degree in Finance from the University of Colorado, and he is a Chartered Financial Analyst.

In the event that you missed a past Research Briefing, here is the archive…

361 Capital Research Briefing Archive

… [Trackback]

[…] Here you will find 98938 additional Information to that Topic: thereformedbroker.com/2013/06/11/361-capital-weekly-research-3/ […]

… [Trackback]

[…] Information to that Topic: thereformedbroker.com/2013/06/11/361-capital-weekly-research-3/ […]

… [Trackback]

[…] Find More Information here to that Topic: thereformedbroker.com/2013/06/11/361-capital-weekly-research-3/ […]

… [Trackback]

[…] Info to that Topic: thereformedbroker.com/2013/06/11/361-capital-weekly-research-3/ […]

… [Trackback]

[…] Read More Information here on that Topic: thereformedbroker.com/2013/06/11/361-capital-weekly-research-3/ […]

… [Trackback]

[…] Read More Info here on that Topic: thereformedbroker.com/2013/06/11/361-capital-weekly-research-3/ […]

… [Trackback]

[…] Information on that Topic: thereformedbroker.com/2013/06/11/361-capital-weekly-research-3/ […]

… [Trackback]

[…] Find More Info here on that Topic: thereformedbroker.com/2013/06/11/361-capital-weekly-research-3/ […]

… [Trackback]

[…] Info on that Topic: thereformedbroker.com/2013/06/11/361-capital-weekly-research-3/ […]

… [Trackback]

[…] Find More on to that Topic: thereformedbroker.com/2013/06/11/361-capital-weekly-research-3/ […]

… [Trackback]

[…] Info to that Topic: thereformedbroker.com/2013/06/11/361-capital-weekly-research-3/ […]