361 Capital portfolio manager, Blaine Rollins, CFA, previously manager of the Janus Fund, writes a weekly update looking back on major moves, macro-trends and economic data points. The 361 Capital Weekly Research Briefing summarizes the latest market news along with some interesting facts and a touch of humor. 361 Capital is a provider of alternative investment mutual funds, separate accounts, and limited partnerships to institutions, financial intermediaries, and high-net-worth investors.

361 Capital Weekly Research Briefing

February 25, 2013

Timely perspectives from the 361 Capital research & portfolio management team

Written by Blaine Rollins, CFA

There was a stand-off in the Global Financial Markets last week…

With the lack of incremental positive news, investors took a deeper look into the current worries:

- The Italian elections?

- The Sequester impact?

- Outlook for the U.S. Consumer which is being impacted by rising gas prices and a rising payroll tax?

- When will the Fed scale back Asset Purchases and then Tighten Rates?

The worrying will continue until we receive more incremental positive data and this will be a big week for economic statistics so stay tuned. In the meantime, we will keep a close eye on the following data points…

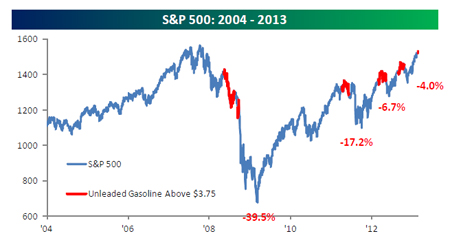

Paying $80 to fill up a tank is not enjoyable for my wallet and usually gives the market a pause also…

(Bespoke)

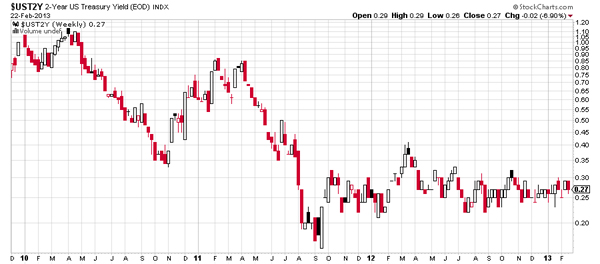

While many in the risk markets were getting nervous last week, a breakdown in the 2 year yield chart would be your green light to reach for the Pepto-Bismol. But so far, it is nearly a flat line…

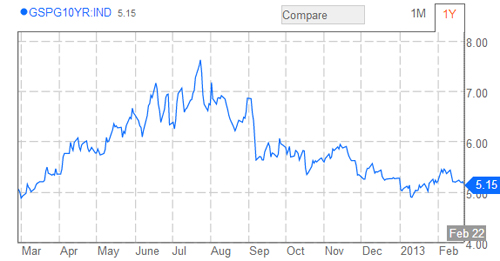

The other big risk thermometer in the world is the 10 year Spanish bond yield. The market should be happy with yields closer to a 4 handle than a 6 handle…

A breakdown in Gold is a positive for Risk assets…

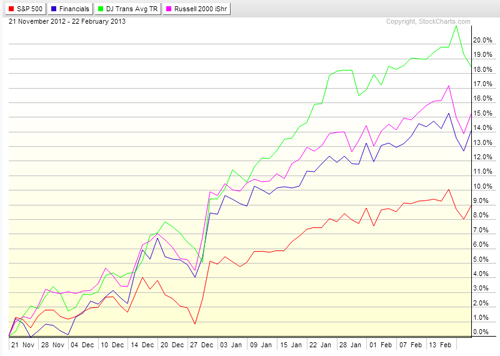

The market has been higher YTD by Financials, Transports and Small Caps. A dent in this leadership would be cause for concern…

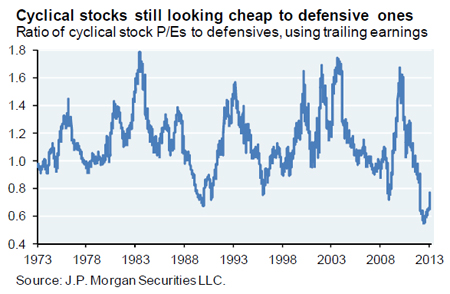

Cyclicals typically lead the equity markets higher and right now they are VERY cheap versus Defensive stocks…

(Michael Cembalest, J.P. Morgan Asset Management)

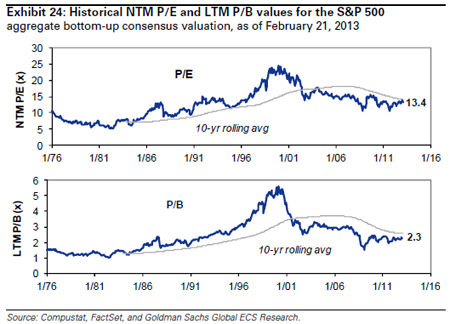

As for the overall market, valuations are nowhere near excessive…

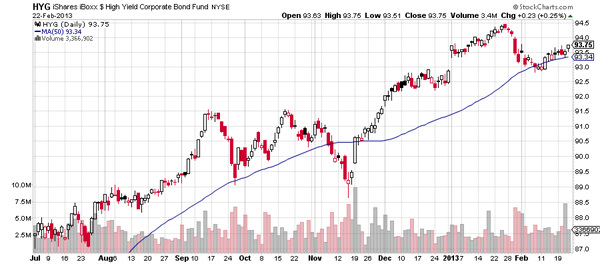

Keep an eye on Junk Bonds which had a pullback, but found some fresh buying last week…

A timely memo from Howard Marks stating why Oaktree thinks that high yield bonds are less vulnerable to rising interest rates…

(OaktreeCapital)

Alan Greenspan reminds us of the importance of equity prices to the economy…

“People don’t realize the significance of equity prices, and asset prices in general, for day-to-day economic activity, according to Greenspan. His research shows that equity markets are not only a leading economic indicator, but, much more important, they are fundamental creators of economic activity. Approximately 6% of the growth in GDP is funded by a rise in equity values, on average, though this varies considerably. As a result, increasing equity values can be even more important for economic growth than fiscal stimulus.”

(AdvisorPerspectives)

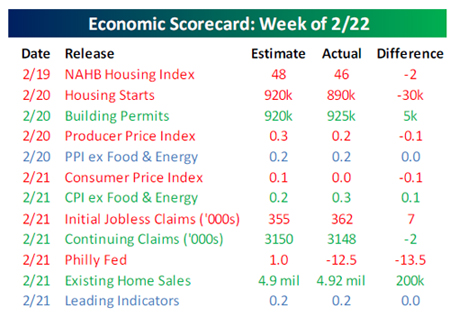

It was a slow week of Economic Data which tended toward the weak side. Housing was especially under pressure due to Toll Brothers weaker than expected quarterly earnings. And Caterpillar’s monthly statistics slowing in January did little to help the commodity or emerging market sentiment.

(Bespoke)

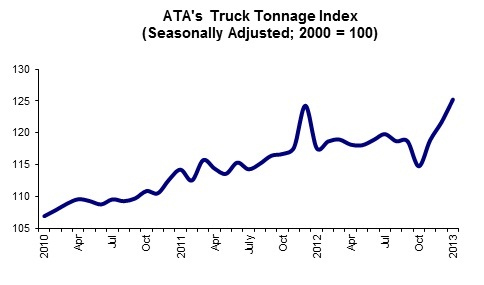

But not all the data was weak and the Trucking Industry showed…

January’s index was the highest on record. Compared with January 2012, the SA index was up a robust 6.5%, the best year-over-year result since December 2011. “The trucking industry started 2013 with a bang, reflected in the best January tonnage report in five years,” ATA Chief Economist Bob Costello said. “While I believe that the overall economy will be sluggish in the first quarter, trucking likely benefited in January from an inventory destocking that transpired late last year, thus boosting volumes more than normal early this year as businesses replenish those lean inventories.”

(TruckLine)

The Architecture Survey also showed a solid start to 2013…

The American Institute of Architects (AIA) reported the January ABI score was 54.2, up sharply from a mark of 51.2* in December. This score reflects a strong increase in demand for design services (any score above 50 indicates an increase in billings). The new projects inquiry index was 63.2, much higher than the reading of 57.9 the previous month. “We have been pointing in this direction for the last several months, but this is the strongest indication that there will be an upturn in construction activity in the coming months,” said AIA Chief Economist, Kermit Baker, PhD, Hon. AIA. “But as we continue to hear about overall improving economic conditions and that there are more inquiries for new design projects in the marketplace, a continued reservation by lending institutions to supply financing for construction projects is preventing a more widespread recovery in the industry.”

(CalculatedRisk)

And over in Europe, the biggest buyout since 2008 might be lining up…

A British-based private equity consortium is preparing a €3.5bn bid for French catering company Elior in what would be the biggest buyout in continental Europe since Lehman Brothers collapsed in 2008. CVC Capital Partners and BC Partners have teamed up to launch a buyout of Elior, underlining how confidence is returning to Europe’s private equity sector… The move partly highlights how recovering debt markets and the easing of the Eurozone debt crisis have triggered an improvement in sentiment among Europe’s leveraged buyout groups. Buyout groups are now able to finance larger deals and are showing stronger appetite to put their investors’ capital to work. (FinancialTimes)

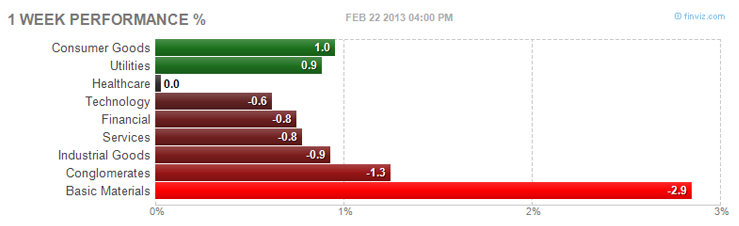

Inside the equity markets, Staples & Utilities won the week while Materials lost…

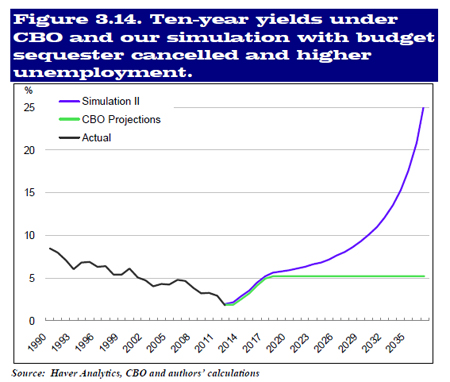

A timely paper by four economic thought leaders this weekend that should be kept away from all debt rating agencies…

“We can also examine a scenario in which policy actions and economic outcomes produce a less favorable path for the primary budget deficit (using our baseline current account deficit assumption of 2.5% of GDP). For example, suppose that the looming budget sequester scheduled to occur on March 1 is cancelled and that the steady-state unemployment rate is assumed to be 6% (as opposed to the 5.25% as assumed by CBO). In this case (which we refer to as Simulation II), the budget deficit would be quite a bit higher than in the initial scenario. The debt/GDP ratio would rise much more rapidly, hitting 304% of GDP by 2037 and bond yields would skyrocket, eventually getting above 25%.”

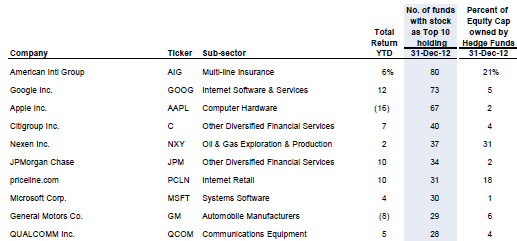

Goldman Sachs updated their Very Important Positions (VIP) for hedge funds basket as a result of all of the newest 13F filings. On Bloomberg you can pull the basket up using (GSTHHVIP). Probably to no one’s surprise, Apple has fallen from the top of the list…

(Goldman Sachs)

As Google leapfrogs Apple in Hedge Fund portfolios, is this Google device the next product that will change our lives?

“One day, I went to work — I live in SF and I have to commute to Mountain View and there are these shuttles — I went to the shuttle stop and I saw a line of not 10 people but 15 people standing in a row like this,” she puts her head down and mimics someone poking at a smartphone. “I don’t want to do that, you know? I don’t want to be that person. That’s when it dawned on me that, OK, we have to make this work. It’s bold. It’s crazy. But we think that we can do something cool with it.”

(TheVerge)

Something to keep an eye on which the M&A markets would not like…

Washington lawmakers, scrambling to close budget gaps and trim the deficit, will consider limiting or eliminating the ability of PE-owned companies to deduct from their taxes the interest on their loans, sources said. PE firms, which own companies employing 1 out of 10 Americans, have sidestepped about $127 billion in U.S. taxes since 2000 via this deduction. “I basically believe [the tax break] will be affected in tax reform,” a well-placed DC source who works for the PE industry said. Interest deductibility may end for junk bonds and mezzanine loans, although lobbyists might persuade legislators to keep the exemption for bank loans, the source added.

(NYPost)

Seeing Martin Zweig on Wall Street Week and reading his work had something to do with me changing my major to Finance and following a path to the markets. So if it wasn’t for Marty, Lou would have never had a reason to ask me onto his show one Friday a long time ago.

A regular guest on the PBS television show Wall Street Week with Louis Rukeyser, Zweig is credited with developing the technical analysis tool known as the put-call ratio, according to his firm. The indicator plots bearish versus bullish options as a way of determining investor sentiment. Zweig’s best-known call came during Rukeyser’s program on Oct. 16, 1987, when he predicted stocks were poised for a “vicious” decline reminiscent of the crash of 1929. The Dow Jones Industrial Average plunged 508 points, or a record 23 percent, in the next session, now known as Black Monday… Zweig bought bearish options and advised readers of the Zweig Forecast to do the same prior to the 1987 crash. The strategy generated an 8.7 percent profit for the month and helped push his picks up 50 percent in 2007.

(Bloomberg)

Tweet of the Week…

@OracleofWallSt: Alleged insider trader using Swiss account to purchase Heinz before takeover bid by Buffet identified.

Blaine Rollins, CFA, is managing director, senior portfolio manager and a member of the Investment Committee at 361 Capital. He is responsible for manager due-diligence, investment research, portfolio construction, hedging and trading strategies. Previously Mr. Rollins served as Executive Vice President at Janus Capital Corporation and portfolio manager of the Janus Fund, Janus Balanced Fund, Janus Equity Income Fund, Janus Aspen Growth Portfolio, Janus Advisor Large Cap Growth Fund, and the Janus Triton Fund. A frequent industry speaker, Mr. Rollins earned a Bachelor’s degree in Finance from the University of Colorado, and he is a Chartered Financial Analyst.

In the event that you missed a past Research Briefing, here is the archive…

361 Capital Research Briefing Archive

… [Trackback]

[…] Find More Info here to that Topic: thereformedbroker.com/2013/02/26/361-capital-weekly-research-briefing-34/ […]

… [Trackback]

[…] Find More to that Topic: thereformedbroker.com/2013/02/26/361-capital-weekly-research-briefing-34/ […]

… [Trackback]

[…] Info to that Topic: thereformedbroker.com/2013/02/26/361-capital-weekly-research-briefing-34/ […]

… [Trackback]

[…] Read More Information here on that Topic: thereformedbroker.com/2013/02/26/361-capital-weekly-research-briefing-34/ […]

… [Trackback]

[…] Read More Info here on that Topic: thereformedbroker.com/2013/02/26/361-capital-weekly-research-briefing-34/ […]

… [Trackback]

[…] Info to that Topic: thereformedbroker.com/2013/02/26/361-capital-weekly-research-briefing-34/ […]

… [Trackback]

[…] Find More here on that Topic: thereformedbroker.com/2013/02/26/361-capital-weekly-research-briefing-34/ […]

… [Trackback]

[…] There you can find 66146 more Information on that Topic: thereformedbroker.com/2013/02/26/361-capital-weekly-research-briefing-34/ […]

… [Trackback]

[…] Info to that Topic: thereformedbroker.com/2013/02/26/361-capital-weekly-research-briefing-34/ […]

… [Trackback]

[…] Here you will find 70256 more Information on that Topic: thereformedbroker.com/2013/02/26/361-capital-weekly-research-briefing-34/ […]