361 Capital portfolio manager, Blaine Rollins, CFA, previously manager of the Janus Fund, writes a weekly update looking back on major moves, macro-trends and economic data points. The 361 Capital Weekly Research Briefing summarizes the latest market news along with some interesting facts and a touch of humor. 361 Capital is a provider of alternative investment mutual funds, separate accounts, and limited partnerships to institutions, financial intermediaries, and high-net-worth investors.

361 Capital Weekly Research Briefing

August 26, 2013

Timely perspectives from the 361 Capital research & portfolio management team

Written by Blaine Rollins, CFA

Choose your door wisely. The final stretch for 2013 performance is almost upon us…

“A new day will dawn for those who stand long.” – Led Zeppelin

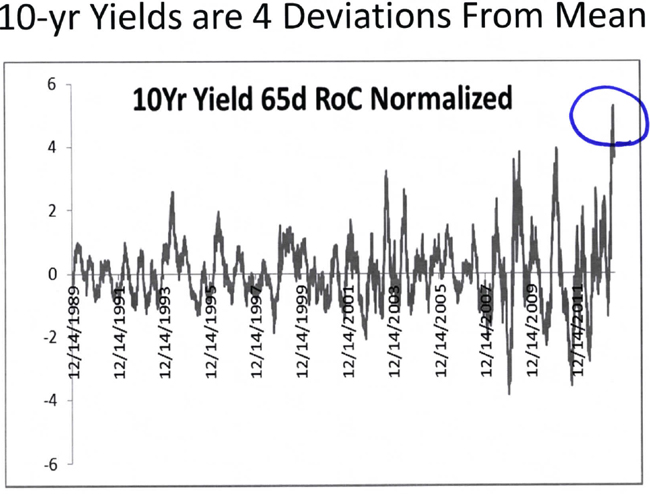

If I was being forced to choose a side for year end 2013 performance, I would have to agree with Mr. Plant. While September is historically a difficult month for the markets, we also know that the Q4 tends to reward the equity markets. But if you consider the big picture: 1) everyone expects the taper to begin in September, 2) more recent economic data in the U.S. shows less robustness (consumer retail spending, housing), 3) employment data continues to show slow, gradual improvement. So it would likely take a real jump higher in the European or Emerging Markets economic data for the Fed to consider tapering/tightening quicker than their current plan. And don’t forget to look at the U.S. Treasury Bond market which is 4 standard deviations oversold; any relief to bonds would be most welcome to equity investors. Meanwhile, the internals of the market remain weighed toward RISKON with SmallCap > LargeCap, Cyclicals > Consumer/Defensive, Europe > U.S., Junk Bonds > Treasuries, etc. So in your final week of summer, think about which door you will choose and be ready for the stairway that you will receive.

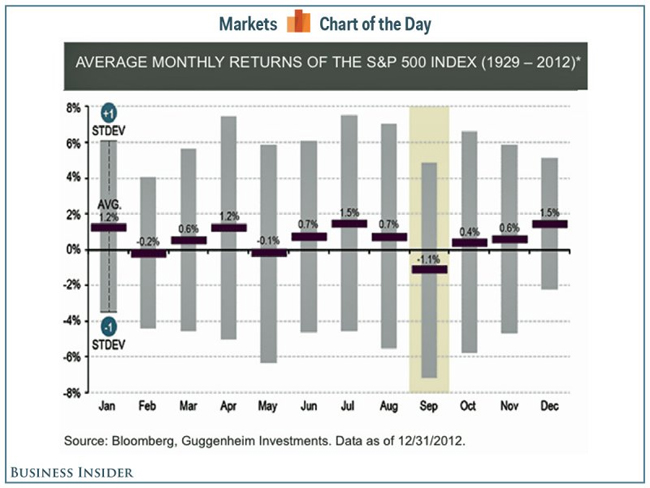

September typically means pain on the football field and on the floor of the exchanges…

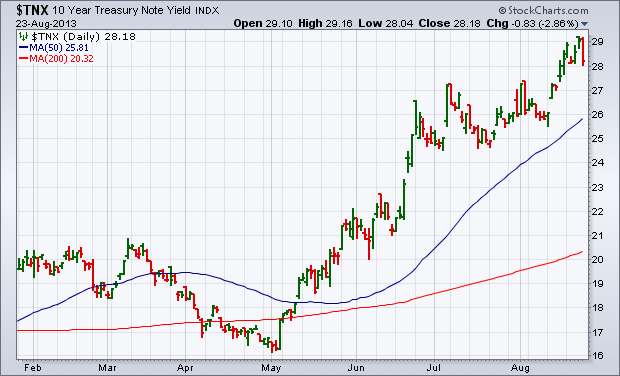

And while 10 year Treasury Bond Yields moved to new highs last week, they also moved to 4 standard deviations wide…

(RenMac)

As a result of the yield spike this summer, new corporate bond issuance has dried up. Will less supply = lower yields?

Global corporate bond issuance has this month fallen to the lowest level in five years as market turmoil, triggered by rising U.S. Treasury yields, persuades companies worldwide to shelve funding plans. Just $61bn in investment grade corporate debt has been raised so far in August, putting it on course to be the weakest month since 2008, according to data from Dealogic. In August last year, more than $121bn in new corporate debt was issued.

(FinancialTimes)

Also interesting last week was the return of Small Caps, which again overtook Large Caps in performance…

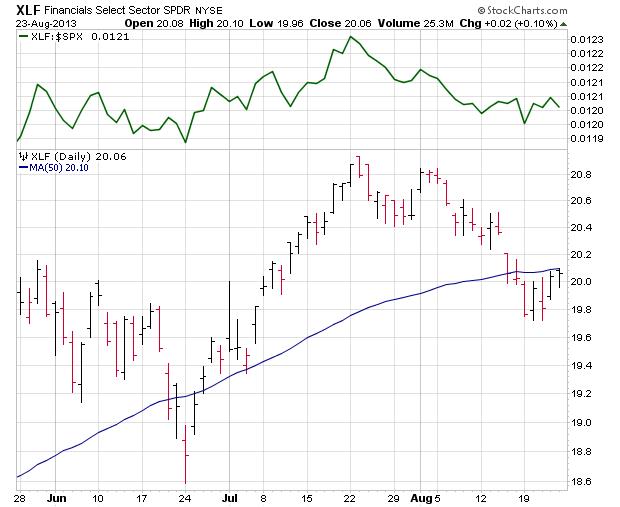

LONGS are still waiting for the Financials to retake the 50day and regain their market leadership…

Looks like the VIX spike to 16 was all that this mini correction had in it. So back to 12 again?

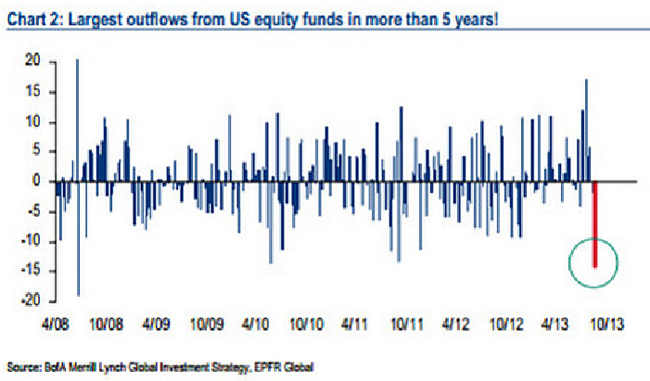

The cautiousness in bonds and equities caused $10b to fly out of the SPY ETF which rippled through the weekly fund flows…

Investors yanked $12.3 billion out of U.S. equity funds last week, the biggest outflow in more than five years, according to Michael Hartnett, chief investment strategist at Bank of America Corp.’s Merrill Lynch. The outflow marked the first time in eight weeks that investors yanked money out of U.S. stock funds. Mr. Hartnett points out the bulk of that amount — $10 billion — came from the ETF market’s largest fund, the SPDR S&P 500 (SPY). ETFs often attract a hefty dose of “hot” money that flows in and out from traders and hedge funds.

The Fed Minutes released last week had some meat for both the hawks and doves…

- “A number of participants indicated, however, that they were somewhat less confident about a near-term pickup in economic growth than they had been in June; factors cited in this regard included recent increases in mortgage rates, higher oil prices, slow growth in key U.S. export markets, and the possibility that fiscal restraint might not lessen…”

- According to the Fed minutes, “almost all participants” in the meeting were “broadly comfortable” with plans outlined by Ben Bernanke, Fed chairman, to scale back its $85bn a month in monthly bond purchases this year, and wind them down entirely by the middle of next year. But they do not appear to have settled on whether the economy was strong enough to withstand a first tapering step at the next meeting on September 17-18. “A few members emphasized the importance of being patient and evaluating additional information on the economy before deciding on any changes to the pace of asset purchases,” the minutes said. It noted that “a few others” had “suggested that it might soon be time to slow somewhat the pace of purchases”.

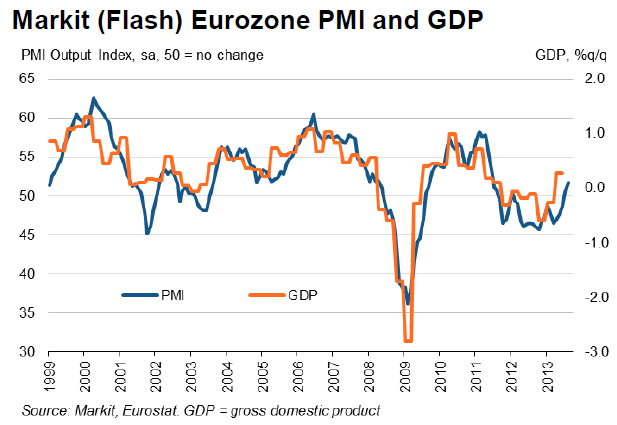

There were several interesting economic data points last week…Both China and Europe put up better than expected PMI data…

Better economic numbers out of China and Europe, whether believable or not, are starting to change perceptions in the near term. This could continue to disrupt the so-called goldilocks environment that existed in the U.S. the first part of the year. Some are becoming less bearish on commodities and materials, which could put pressure on many of the winning sectors from the first part of the year as prices and yields rise.

(FusionMarketSite)

The ABI index continued to show ramping internals…

The Architecture Billings Index (ABI) saw a jump of more than a full point last month, indicating acceleration in the growth of design activity nationally. As a leading economic indicator of construction activity, the ABI reflects the approximate nine to twelve month lead time between architecture billings and construction spending. The American Institute of Architects (AIA) reported the July ABI score was 52.7, up from a mark of 51.6 in June. This score reflects an increase in demand for design services (any score above 50 indicates an increase in billings). The new projects inquiry index was 66.7, up dramatically from the reading of 62.6 the previous month.

(CalculatedRiskBlog)

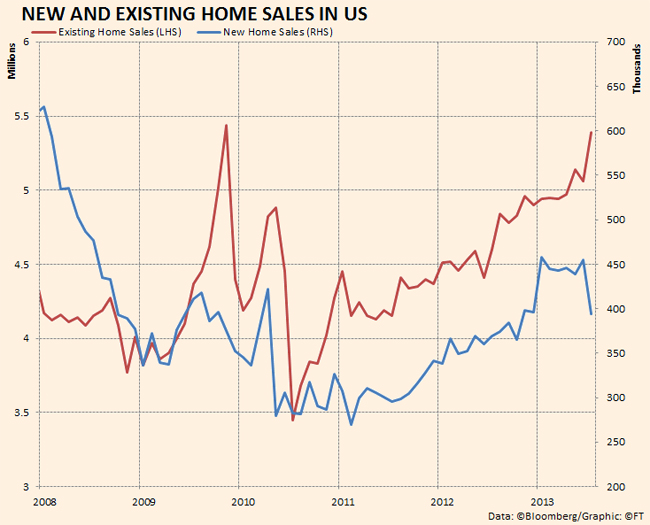

But one economic surprise that we did see was a pullback in New Home Sales…

Prices are up and Interest Rates are up so those new home lots are seeing more cautious buyers.

And some of the comments by retailers were a bit discouraging…

- Target: For the balance of this year, our U.S. outlook envisions continued cautious spending by consumers in the face of ongoing household budget pressures.

- Abercrombie & Fitch: “We believe youth spending has diverted into other categories.”

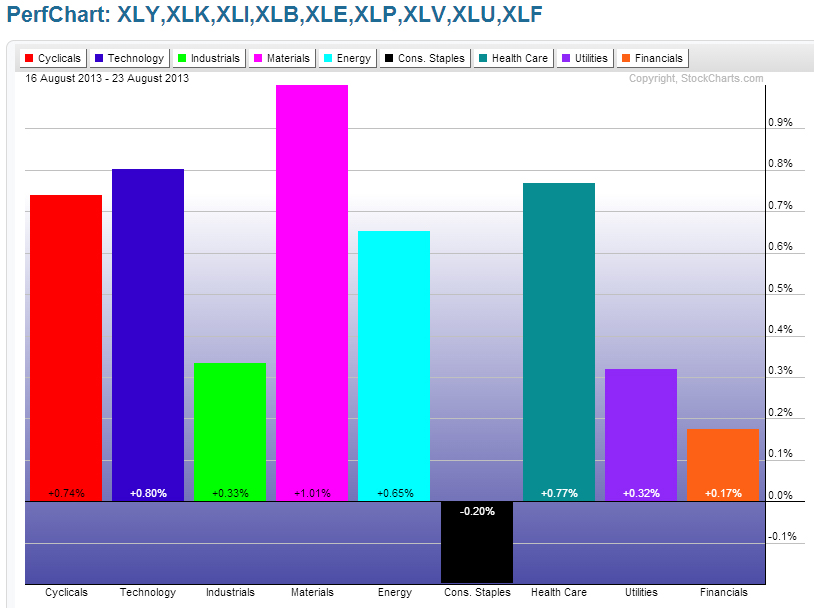

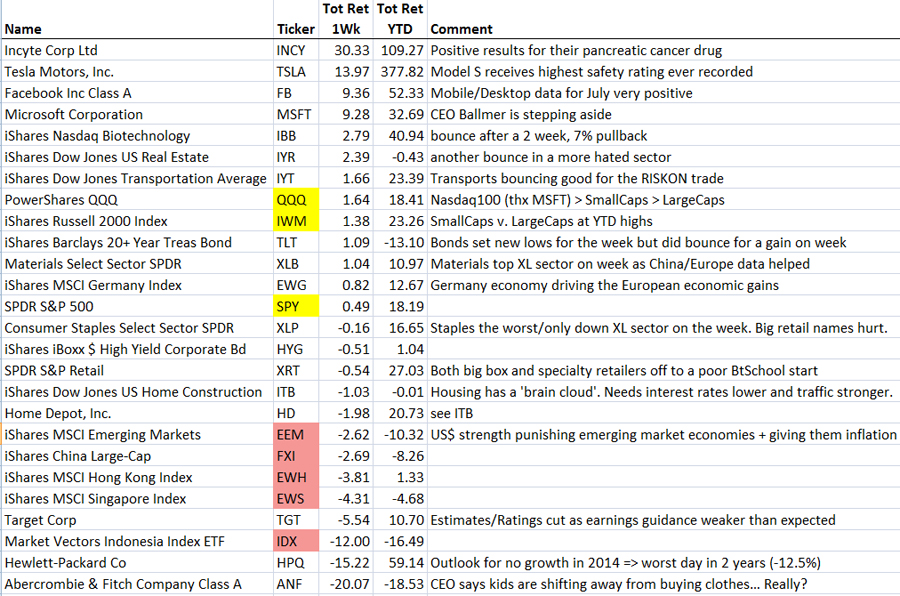

For the week in the market, all XL sectors finished except the Retail/Defensive heavy Staples sector…

A good week in the U.S. for the RISKON trade with Small Caps leading the market higher…

Stocks stopped trading on the Nasdaq for 3 hours on Thursday of last week, but the markets didn’t care and finished higher.

@666743x: A look inside the NASDAQ break room…

Evaluating your domestic growth equity managers in 2013 could not be simpler…

Question 1: Did you outperform your benchmark?

Question 2: How much has Tesla contributed to your performance?

If the answer to Q1 is ‘No’ and Tesla does not appear on your quarterly holdings report, then send them packing.

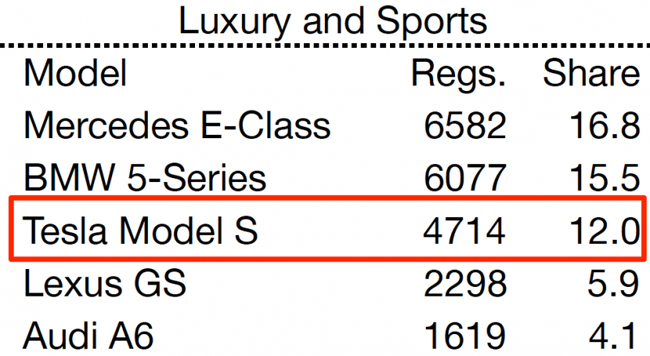

The new Tesla Model S now has 12% of monthly luxury car sales in California. This business model has become a growth stock manager’s dream stock. In my old days at Janus, one of our analysts would be rabidly calling and visiting mall stores to get a read on daily, weekly, and monthly sales. That same analyst would likely be holed up in a Motel 6 down the street from their main production facility counting the cars as they drove out for the first time. The investing world needs more Elon Musks to put more great growth enterprises into the marketplace. In the meantime, if you want to invest in growth stocks, make sure that your managers know how to invest in the best.

And looking to further spike future sales for the Tesla Model S…

The Tesla Model S may be the safest vehicle ever tested by the Feds. So safe, in fact, that according to the automaker, the all-electric sedan broke the testing equipment at an independent commercial facility. Most cars get five stars in the National Highway Traffic Safety Administration’s frontal crash protection test and four stars for side impact protection. But the Model S aced them all: front, side, pole, and rollover. And Tesla adds in its announcement that during a previous roof crush test used during validation, the machine failed while applying more than 4 G’s of pressure — the same as stacking four of the electric sedans on top of the car without the roof breaking. When NHTSA added up all the scores, it totaled a combined five stars across the board — one of the highest ever recorded for a production vehicle.

(Wired)

Is Uber one of the next great growth companies of the future?

As many of you have seen in the press today, Uber recently closed a financing round. We want to make sure the facts are clear and confirmed. Our vision is to build a technology company that changes transportation and logistics in urban centers around the world, and this financing gives us the fuel to make that a reality. This round is $258 million with proceeds to be used to expand into new markets, accelerate customer and driver acquisition, and fight off protectionist, anti-competitive efforts.

(UberBlog)

Speaking of the great growth companies of the future, you are not welcome in Minnesota…

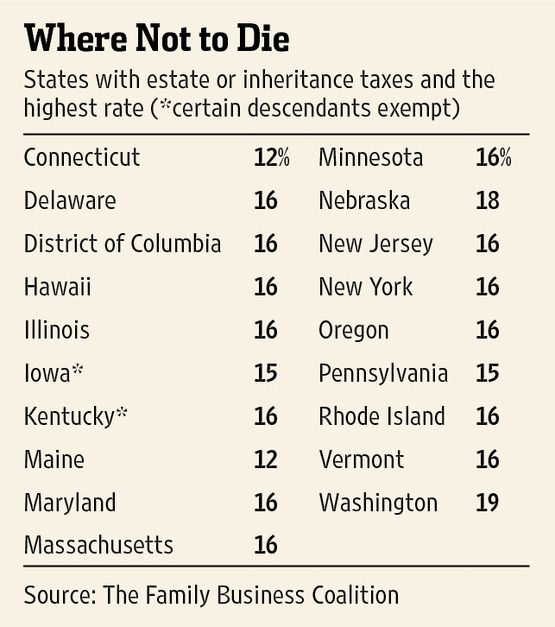

The grand prize for self-abuse goes to Minnesota, which this year enacted a new 10% gift tax with a $1 million exemption. A gift tax is a levy on money given away while still alive. This tax is in addition to Minnesota’s 16% estate tax. The new law is all the more punitive because it applies the 16% estate tax (6% on top of the earlier 10% gift tax) to any gift within three years of death. This is essentially a clawback tax, or more taxation without respiration. Democratic Governor Mark Dayton, who signed the law, is the heir to a department store fortune and knows a lot about inheriting wealth, but not much about creating it.

(WSJ)

Barron’s talking up Alternatives this week. If you need help finding a mutual fund to fill this bucket, I know a top performer…

Bonds have provided much-needed support for investors since the financial crisis. But now, with rates rising and stocks looking a little rich, it’s worth considering a change in the mix of your portfolio. Including alternative assets is one way to create other sources of momentum. “We encourage clients to have investments in alternative assets,” says Charles Zhang, managing partner of Zhang Financial, in Portage, Mich. “They can significantly lower risk while increasing returns.”… They are a timely investment because the upward trend in interest rates has made traditional fixed income “a very challenged asset class in real returns,” says Michael Christ, head of Guggenheim Investment Advisory.

(Barron’s)

@jfahmy: Detroit would be in much better shape if they didn’t spend all that money on Robocop

The drama in Detroit is better than anything at the box office this summer. But if the current and future pensioners of the Detroit pension plan do not fire their Board, they will suffer a significant financial hit to their recovery as the City goes through bankruptcy. There is ABSOLUTELY NO REASON for the Board to use a fictitious 8% return assumption when calculating their underfunding levels…

Further excitement in the saga of Detroit’s bankruptcy: Public-sector unions are challenging the city’s estimates of its pension underfunding. The actuaries hired by the city’s emergency manager say that the pensions are underfunded by 40 percent to 50 percent. The estimated shortfall, according to The Wall Street Journal, is more than five times higher than previous estimates.

(Bloomberg)

Funniest thing I saw all week, courtesy of my 9 year old…

In the event that you missed a past Research Briefing, here is the archive…

361 Capital Research Briefing Archive

The information presented here is for informational purposes only, and this document is not be construed as an offer to sell, or the solicitation of an offer to buy, securities. Some investments are not suitable for all investors, and there can be no assurance that any investment strategy will be successful.

Blaine Rollins, CFA, is managing director, senior portfolio manager and a member of the Investment Committee at 361 Capital. He is responsible for manager due-diligence, investment research, portfolio construction, hedging and trading strategies. Previously Mr. Rollins served as Executive Vice President at Janus Capital Corporation and portfolio manager of the Janus Fund, Janus Balanced Fund, Janus Equity Income Fund, Janus Aspen Growth Portfolio, Janus Advisor Large Cap Growth Fund, and the Janus Triton Fund. A frequent industry speaker, Mr. Rollins earned a Bachelor’s degree in Finance from the University of Colorado, and he is a Chartered Financial Analyst.

… [Trackback]

[…] Read More Info here on that Topic: thereformedbroker.com/2013/08/27/361-capital-weekly-research-briefing-54/ […]

… [Trackback]

[…] Find More to that Topic: thereformedbroker.com/2013/08/27/361-capital-weekly-research-briefing-54/ […]

… [Trackback]

[…] Info to that Topic: thereformedbroker.com/2013/08/27/361-capital-weekly-research-briefing-54/ […]