361 Capital portfolio manager, Blaine Rollins, CFA, previously manager of the Janus Fund, writes a weekly update looking back on major moves, macro-trends and economic data points. The 361 Capital Weekly Research Briefing summarizes the latest market news along with some interesting facts and a touch of humor.

361 Capital is a provider of alternative investment mutual funds, separate accounts, and limited partnerships to institutions, financial intermediaries, and high-net-worth investors.

***

361 Capital Weekly Research Briefing

June 4, 2012

Timely perspectives from the 361 Capital research & portfolio management team

Written by Blaine Rollins, CFA

“We need to decide whether we want to be part of the past or part of the future.”

David Dencik ‘Tinker Tailor Soldier Spy’ 2011

School is out for the kids, but for all world leaders summer school is about to begin…

Three months ago, the world’s financial markets looked to be in a safe, steady place with the U.S. showing signs of economic recovery and China doing everything that it could to engineer a soft landing. But in the last two months, positive economic surprises in the U.S. turned negative, Europe showed no bounce and China, India & Brazil all slowed down much faster than expected. With Spain now on fire, the U.S. equity market looking at a 10% correction and financial stocks, crude oil and high yield bonds showing signs of stress, it is clear for all to see that it is time for global leadership to get the markets back to a happier place. Otherwise, consumer and business confidence will follow the equity markets south and a double dip recession will be inevitable. So to all incumbent politicians in Washington D.C. and Europe, cancel the summer vacation plans to Martha’s Vineyard and the Mediterranean beaches because there is no time like now for a fix to be put in place. Think big, bold and audacious because the markets will laugh at anything less. Have a great summer!

World leaders might start their next meeting by reading this suicide note…

“The police does not know me. I have never touched a drink in my life. Of women and drugs I have never even dreamed of. I have never been to a kafenio (coffee house), I just worked all day! But I committed one horrendous crime: I became a professional at age 40 and I plunged myself in debt. Now, I’m an idiot of 61 years and I have to pay. I hope my grandchildren are not born in Greece, seeing as there will be no Greeks here from now on. Let them at least know another language, because Greek will be wiped off the map! Unless of course there was a politician with Thatcher’s balls so as to put us and our state in line. Signed, Alexandros 29/5/2012” (AthensNews)

And in case you forgot how the Iron Lady dealt with the Socialists…

(Highlights of Margaret Thatcher’s last House of Commons Speech, Nov 1990)

The fire in Spain is not being contained by the E.U. or E.C.B….

- Data published by Spain’s central bank showed € 97bn had been pulled out in the first quarter — around a 10th of the country’s GDP — as concerns mounted over Madrid’s ability to contain its twin economic and financial crises, which have forced government borrowing costs to euro-era highs. The data appeared to corroborate earlier assessments from economists that foreign investors were selling Spanish assets, while Spanish banks were increasing their holdings of domestic bonds, helped by cash accessed through the ECB’s three-year liquidity operations. “My concern is that we haven’t yet seen the most recent numbers, which could be far worse,” said Raj Badiani, an economist at IHS Global Insight. “We are seeing a perfect storm.” (CNN)

- “We’re in a situation of total emergency, the worst crisis we have ever lived through” said ex-premier Felipe Gonzalez, the country’s elder statesman. (Telegraph)

- @beckyquickcnbc: “(European bank) depositors have not yet begun to run, but they are starting to jog.” — Robert Zoellick, World Bank Pres.

2 year German Bonds traded to negative yields this week. Not a good sign for any risk investor…

And it isn’t just Germany, but all safe havens are seeing record low 10 year yields…

(TheBigPicture)

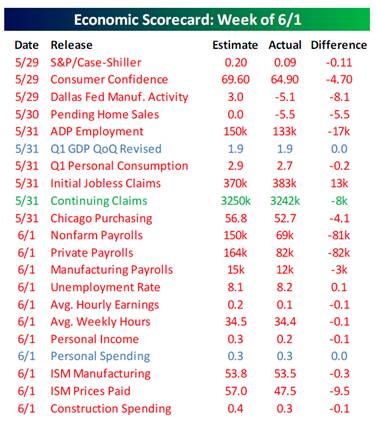

Friday’s payroll/unemployment data was surprisingly weak to most everyone…

As soon as the disappointing data for May and April revisions were released, the economists and strategists immediately pulled out the knives to carve down their GDP estimates:

- Over the first five months of the year the labor market has steadily lost momentum and we are now confronted with a global growth slowdown which will provide a further headwind to the economy. As such, we are taking Q3 growth from 3.0% to 2.0%, with much of the downward revision accounted for by an expectation that the pace of export growth will slow. We are leaving our Q4 forecast unchanged at 2.0%, though there are downside risks to that quarter as the fiscal uncertainties could weigh on the economy. (JPMorgan)

- Spare capacity has translated to soft wage growth. Average hourly earnings were only up 0.1% m/m or 1.7% y/y, which means continued weakness in income growth. Moreover, with the three-month trend in aggregate hours worked running just 1.0%, today’s employment report suggests downside risk to Q2 GDP. This is the beginning of the slowdown, which we expect to translate to only 1.0% GDP growth by Q4. (BofA)

- The May jobs report confirmed our view that U.S. growth remains stuck in a low gear. Nonfarm payroll employment increased by less than expected and job growth in earlier months was revised down…We are cutting our forecasts for Q4 2012 and Q1 2013 GDP growth by ½ point each, to 2% and 1½% respectively. (Goldman Sachs)

- Judging by the 2010/2011 Growth Problems in the U.S., stall-speed concerns are likely to push stock prices lower. Payroll employment increases are likely to run just +110k, and unemployment is likely to remain at 8.2%. We’re lowering our 2Q and 2H real GDP forecasts from +2.5% to +2.0%. (ISI Group)

- Morgan Stanley ups chances of QE3 at June Fed meeting from 50% to 80% after poor U.S. payrolls. (Dow Jones)

- “Friday’s weak U.S. employment report confirms a disappointing historical pattern: after an encouraging start to the year, job creation has again hit a soft patch. To make things worse, there is a distinct possibility that, absent major policy initiatives on both sides of the Atlantic, the U.S. economy may not accelerate as quickly as many hope – thus increasing America’s vulnerability to the deepening crisis in Europe.” Mohamed El-Erian (FT)

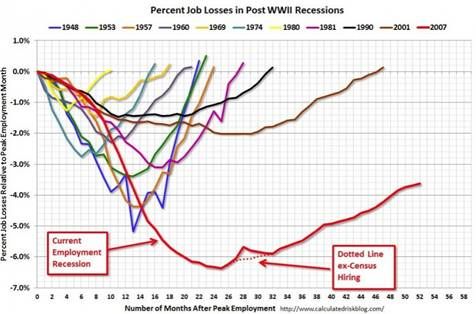

How much longer until the red line crosses zero?

Also on Friday, U.S. May auto sales of 13.8m came in well below forecasts of 14.4m…

“Since our last monthly sales call over the last 30 days or so, the economic indicators came in just a little softer than in the first quarter,” Ford senior economist Jenny Lin said on a conference call. (Reuters)

Bottom line, it was a very difficult week for U.S. economic data…

(Bespoke)

And an even worse WEEK for risk taking in as shown through the ETF performances:

- U.S. 20+ Yr Treasury/TLT +5.4% (that is a BIG move)

- Gold/GLD +2.3% (Fear + Panic > Inflation worries)

- South Korea/EWY +1.4%

- China/FXI +0.9%

- Utilities/XLU -0.1% (best performing XL sector)

- Apple/AAPL -0.2% (great showing by the new CEO at WSJ/ATD conference)

- Emerging Markets/EEM -0.9%

- High Yield Bonds/HYG -1.2% (keep a close eye on credit spreads)

- Dow Jones Industrial/DIA -2.6% (basically flat on the year at +0.3%)

- Nasdaq100/QQQ -2.7% > Large Cap/SPY -3.0% > Small Cap/IWM -3.8%

- U.S. Regional Banks/KRE -5.3% (another rising concern for the market)

- Germany/EWG -5.6% (what might Germany pay to save weaker Europe?)

- Spain/EWP -7.8% (-29.8% YTD)

- Home Construction/ITB -8.0% (due to weaker U.S. employment data & auto sales)

- Oil/USO -8.4% (world growth evaporating)

- Natural Gas/UNG -11.5% (so much for that LONG trade)

GM follows Ford’s lead to exit its ownership of long term pension liabilities…(expect the rest of corporate America to follow because why would any fiduciary want to PROMISE 7-8% returns in a world of 1% yield U.S./German bonds?)

General Motors Co., Detroit, on Friday announced it would offer a lump-sum payment to 42,000 retirees in its salaried pension plan and also will purchase a group annuity contract with Prudential Insurance under which Prudential will pay and administer future benefit payments to another 76,000 U.S. salaried retirees. Any of the 42,000 retirees who reject the lump-sum payment would be included in the annuity. The move will reduce GM’s expected pension obligations to its U.S. salaried defined benefit plans by $26 billion. All of GM’s DB plans had a total of $94.3 billion in assets as of Dec. 31. (Pensions&Investments)

Buy Virginia, Short Maryland…

Maryland accounted for the largest taxpayer exodus of any state in the region between 2007 and 2010, with a net migration resulting in 31,000 residents having left the state. Where did most of them go? Virginia. Virginia is now home to nearly 11,500 former Marylanders—a shift of $390 million from the tax rolls of one state to another, according to the non-partisan Tax Foundation.

Maryland’s sales tax is 6 percent; Virginia’s is 5 percent. The top personal income tax rate is 9 percent in Maryland compared to 5.75 percent in Virginia. The corporate income tax is 8.25 percent compared to 6 percent. (Reason)

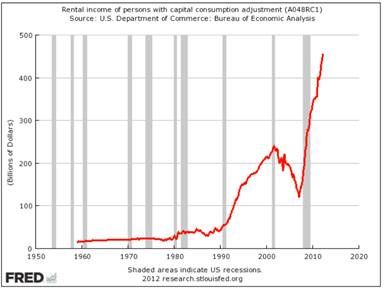

If you own residential rental property in the U.S., congratulations…

(BusinessInsider)

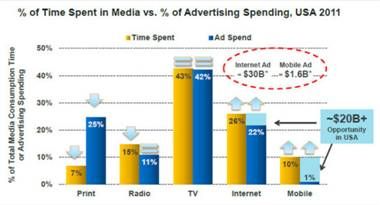

If you own print media companies, be concerned…

(KPCB-Internet-Trends-2012)

Best Quotes of the week…

- “People who thought they were buying this stock so they could get an enormous pop were both naive and ordered under the wrong pretenses. Why you’re taking companies public is to establish a long-term investor base. To that investor, I would hope that they haven’t panicked during the flurry of the last few days.” (Morgan Stanley Chief Executive Officer James Gorman talking about Facebook)

- “I think President Clinton is correct. Private equity is a very important aspect of growing our economy. Obviously there’s good practices in private equity; there are bad practices. You criticize bad practices but not the whole enterprise itself.” (Rep. Steny Hoyer – Maryland)

- “I don’t think I have ever thrown a no-hitter, even in video games. ” (Johan Santana, N.Y. Mets pitcher who threw the organizations first no-hitter)

- “The fact of the matter is that tobacco-related diseases in the state cost California about $9B a year” (Lance Armstrong talking on his support of Proposition 29 on CNN)

- “I told Steve that bricks and mortar was dead. Steve said, “But we’re using glass and steel.” (Larry Ellison recalling a conversation with Steve Jobs)

- @ReformedBroker: “By the way, historically when people start eating each other’s faces, we’re closer to a market bottom than a top.”

Boy Scout motto = Be Prepared. And so Bloomberg went to a live test of the new Greek Drachma this week…

Tips for summer interns (centric for those going to D.C., but applicable to any locale):

- Remember that you are here to learn.

- Don’t be annoying.

- Do the work you are assigned. Then show initiative.

- Keep up with current events.

- Don’t gossip or rant.

- Admit when you make a mistake.

- Try not to go into debt.

- Don’t limit your sight-seeing to Madhatters, Sign of the Whale, Capitol Lounge and/or Union Pub.

- If your employer is abusive, report it.

- Act professional.

- Be prepared: D.C. summers are miserable.

- Have a good attitude.

Queen Elizabeth’s approval rating is 80%. That is incredible.

(Buckingham Palace on the evening of the Diamond Jubilee)

In the event that you missed a past Research Briefing, here is the archive…

(http://361capital.com/

Blaine Rollins, CFA, is managing director, senior portfolio manager and a member of the Investment Committee at 361 Capital. He is responsible for manager due-diligence, investment research, portfolio construction, hedging and trading strategies. Previously Mr. Rollins served as Executive Vice President at Janus Capital Corporation and portfolio manager of the Janus Fund, Janus Balanced Fund, Janus Equity Income Fund, Janus Aspen Growth Portfolio, Janus Advisor Large Cap Growth Fund, and the Janus Triton Fund. A frequent industry speaker, Mr. Rollins earned a Bachelor’s degree in Finance from the University of Colorado, and he is a Chartered Financial Analyst.

In the event that you missed a past Research Briefing, here is the archive…

(http://361capital.com/

… [Trackback]

[…] Read More on that Topic: thereformedbroker.com/2012/06/06/361-capital-weekly-research-briefing-2/ […]

… [Trackback]

[…] Find More on that Topic: thereformedbroker.com/2012/06/06/361-capital-weekly-research-briefing-2/ […]

… [Trackback]

[…] Find More on that Topic: thereformedbroker.com/2012/06/06/361-capital-weekly-research-briefing-2/ […]

… [Trackback]

[…] Here you can find 61132 more Info on that Topic: thereformedbroker.com/2012/06/06/361-capital-weekly-research-briefing-2/ […]

… [Trackback]

[…] Find More here on that Topic: thereformedbroker.com/2012/06/06/361-capital-weekly-research-briefing-2/ […]

… [Trackback]

[…] Find More here to that Topic: thereformedbroker.com/2012/06/06/361-capital-weekly-research-briefing-2/ […]

… [Trackback]

[…] Find More on to that Topic: thereformedbroker.com/2012/06/06/361-capital-weekly-research-briefing-2/ […]