I was on TV the other day next to a guy who goes, totally matter-of-factly: “We should get 8 percent earnings growth for the S&P 500 in 2014 and earnings drive stock market returns so I expect to see an 8ish percent return for the market this year.” My jaw dropped. I don’t even want to tell you how much actual money he manages for people in real life. It’s disturbing.

But only disturbing to me. Everyone else seemed okay with both the forecast and the basis upon which it had been formulated, no questions asked. Maybe I’m the freak. I need to learn to nod my head, I guess. By the way, 8% isn’t very far off of the average annual return for equities, so he may end up being right by accident 😉

So anyway, does earnings growth determine the returns of the stock market?

How about interest rates? Do they drive returns for stocks?

What about inflation? Or GDP growth? Or the rate of the ten-year treasury bond? Or any of the other factors used on a daily basis to predict the markets?

Well? Which one is it? Which one works?

All of them. None of them. Some of them sometimes – but then others of them other times. And usually in all different combinations. Also, they start and stop mattering randomly and with no warning. And then sometimes no combination of any of them is indicative of anything because a president is shot or a war starts or a plane hits a building or a nuclear reactor melts down during an earthquake-caused tsunami on the other side of the world.

In other words, forecasts using any combination of any of these can only ever be nonsense – even if it’s well-meaning nonsense. None of these factors can continually keep an investor on the right side of the stock market, although ignoring them altogether also won’t be able to either.

Ben Carlson is an institutional investor who writes a great new blog called A Wealth of Common Sense. He tries to distill complex topics down into key points of understanding for regular folks and pros who are interested in the truth. I love his stuff. Here he makes the same point with data that I’ve made above with my anecdote:

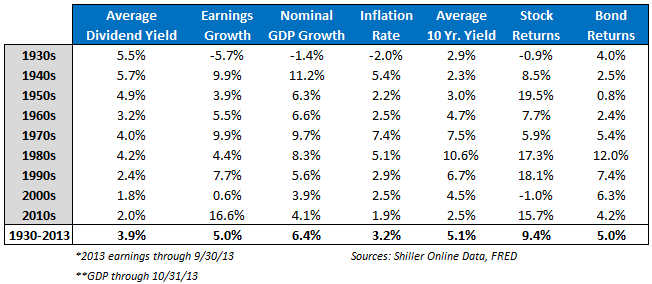

The following table shows the average dividend yield, company earnings growth and performance of the S&P 500 by decade along with economic growth, inflation, average interest rates and the 10 year treasury returns:

Some observations on this data:

- Add up the average dividend yield and the average earnings growth (8.9%) and you get pretty close to the long-term average annual stock return (9.4%) since 1930.

- Yet stock returns can be feast or famine depending on the decade.

- Dividend yields have come down in recent decades, but much of this stems from a combination of rising markets and share repurchases.

- Rising interest rates don’t necessarily have to be bad for stock returns (50s & 60s)

- There were times when bonds outperformed stocks (30s, 00s).

- There were long periods of negative real bond returns (40s to 70s).

- Bonds didn’t have a single decade of negative nominal returns proving their worth as a stabilizer for the low risk part of your portfolio.

- There were times of subdued inflation (50s-60s & 90s-present) and high inflation (40s, 70s & 80s).

- Stocks lost out to inflation over two different decades (70s & 00s)

- There were times when economic growth outpaced growth in company earnings (30s to 60s, 80s & 00s).

- There were times when company earnings growth outpaced economic growth (70s, 90s, 10s).

- Economic growth was fairly stable from the 1950s to the present time but stock returns were not.

- Stocks lost investors money during two decade long stretches (30s & 00s).

- Companies still paid decent dividends during those periods.

- The 1930s were a pretty terrible decade.

Ben goes on to show that stocks have, in fact, murdered bonds in inflation-adjusted terms going back to the 1920’s at a rate of more than 3-to-1. But it is important to note that this long-term record for the market has been accumulated through a vast array of economic environments – no two are ever exactly the same.

Moreover, even when there are similarities between environments – think of the rapid earnings growth during both the 1970’s and the 1990’s – the end results can be starkly different; the 70’s couldn’t have been worse for stocks while the 90’s couldn’t have been better.

The bottom line is that it’s great to be aware of the current trends and the ability to contextualize them in terms of historic periods is probably not harmful either. So long as you’re not betting big on the predictive power of these metrics. Because it’s not different this time, it’s different every time.

Source:

The Way Way Back of Market Cycles (A Wealth of Common Sense)

… [Trackback]

[…] Find More here to that Topic: thereformedbroker.com/2014/03/03/nonsense-forecasts/ […]

… [Trackback]

[…] Find More Information here on that Topic: thereformedbroker.com/2014/03/03/nonsense-forecasts/ […]

… [Trackback]

[…] Here you can find 39477 additional Info to that Topic: thereformedbroker.com/2014/03/03/nonsense-forecasts/ […]

… [Trackback]

[…] Read More Info here on that Topic: thereformedbroker.com/2014/03/03/nonsense-forecasts/ […]

… [Trackback]

[…] Read More on that Topic: thereformedbroker.com/2014/03/03/nonsense-forecasts/ […]

… [Trackback]

[…] Read More Information here to that Topic: thereformedbroker.com/2014/03/03/nonsense-forecasts/ […]

… [Trackback]

[…] Information to that Topic: thereformedbroker.com/2014/03/03/nonsense-forecasts/ […]

… [Trackback]

[…] Find More Info here to that Topic: thereformedbroker.com/2014/03/03/nonsense-forecasts/ […]