The S&P 500’s valuation on current earnings is more expensive than it was last year and more expensive than it was the year before. Relative to 2012 and 2011, it is not cheap. In addition, it is also expensive relative to the earnings growth rate and to the rate of growth in the US economy overall.

But the S&P 500 is not at a bubble valuation at the current moment.

I know sometimes you wish things would be black or white, Summer Roberts or Marissa Cooper, but that sort of exactitude just isn’t how the world works.

And so the answer as to whether or not the market is cheap comes laden with asterisks and caveats and on-the-other-hands.

Here’s FactSet Research with some nuance on the current valuation puzzle:

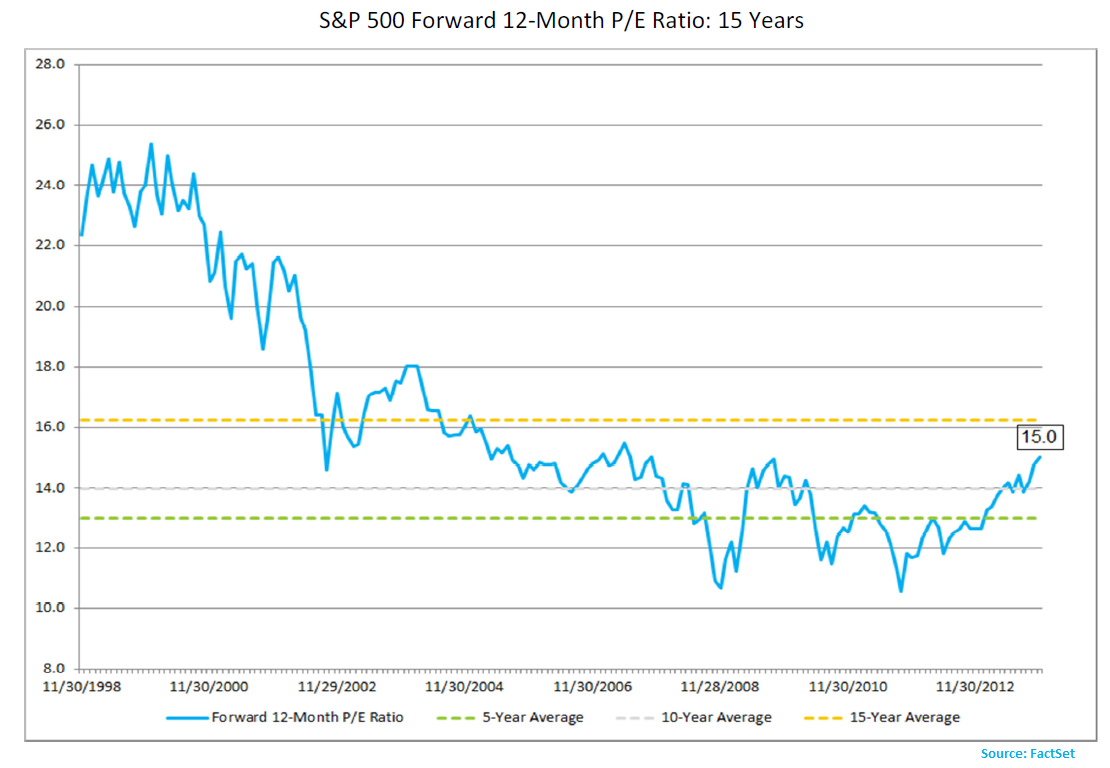

The forward 12-month P/E ratio for the S&P 500 now stands at 15.0, based on yesterday’s closing price (1790.62) and forward 12-month EPS estimate ($119.26). This is the highest forward 12-month P/E ratio logged by the S&P 500 in more than four years (September 2009). Given the high values driving the “P” in the P/E ratio, how does this 15.0 P/E ratio compare to historical averages? Is the index now overvalued? On the one hand, the index is now trading above both the 5-year (13.0) and 10-year (14.0) average P/E ratios. On the other hand, it is still trading below the 15-year average P/E ratio (16.2), and is not close to the peak P/E ratio of 25 recorded in the late 1990’s and early 2000’s.

Josh here – Everything is a relative game in the stock market. Relative not to any numbers or historic time period, but relative to expectations.

Expectations are just now coming around to the bright side. For years there were no expectations whatsoever and this is how we’ve gotten a 40% expansion in the current price-to-earnings multiple.

It ain’t magic.

If people largely expect the worst for an extended period of time and the worst doesn’t happen, longs make money. Lots of it.

Now of course, when expectations start to grow sunny and widespread pessimism begins to subside, things get a bit trickier. Or, at a minimum, the gains become less automatic. That’s how the valuation-relative-to-expectations game ends. Watch carefully as investors’ return presumptions grow beyond what can reasonably be delivered.

I’m a New York City-based financial advisor at Ritholtz Wealth Management LLC. I help people invest and manage portfolios for them. For disclosure information please see here.

Subscribe & Reform

Get a Full Investor Curriculum: Join The Book List

Every month you'll receive 3-4 book suggestions--chosen by hand from more than 1,000 books. You'll also receive an extensive curriculum (books, articles, papers, videos) in PDF form right away.

… [Trackback]

[…] Find More here to that Topic: thereformedbroker.com/2013/11/17/stock-market-valuation-is-a-relative-game/ […]

… [Trackback]

[…] Find More Information here on that Topic: thereformedbroker.com/2013/11/17/stock-market-valuation-is-a-relative-game/ […]

… [Trackback]

[…] Find More here on that Topic: thereformedbroker.com/2013/11/17/stock-market-valuation-is-a-relative-game/ […]

… [Trackback]

[…] Read More on that Topic: thereformedbroker.com/2013/11/17/stock-market-valuation-is-a-relative-game/ […]

… [Trackback]

[…] Find More Information here on that Topic: thereformedbroker.com/2013/11/17/stock-market-valuation-is-a-relative-game/ […]

… [Trackback]

[…] Find More Info here on that Topic: thereformedbroker.com/2013/11/17/stock-market-valuation-is-a-relative-game/ […]

… [Trackback]

[…] Here you can find 77213 additional Info to that Topic: thereformedbroker.com/2013/11/17/stock-market-valuation-is-a-relative-game/ […]

… [Trackback]

[…] Info on that Topic: thereformedbroker.com/2013/11/17/stock-market-valuation-is-a-relative-game/ […]

… [Trackback]

[…] Find More here to that Topic: thereformedbroker.com/2013/11/17/stock-market-valuation-is-a-relative-game/ […]

… [Trackback]

[…] Read More here on that Topic: thereformedbroker.com/2013/11/17/stock-market-valuation-is-a-relative-game/ […]

… [Trackback]

[…] Find More here on that Topic: thereformedbroker.com/2013/11/17/stock-market-valuation-is-a-relative-game/ […]